By 2030, cross-border payments hit $290T. Will XRP, HBAR, XLM, or SWIFT lead the race for faster, cheaper, and more transparent money movement? | Credit: Veronica Cestari/CCN.com

Share

Key Takeaways

Cross-border flows are expected to rise by over 50% from 2023 to 2030, reaching nearly $290 trillion.

SWIFT, blockchain networks, CBDCs, and stablecoins will coexist, each optimized for different use cases and corridors.

Real-time settlement, ISO 20022 messaging, and API-based integration will set new industry standards.

Regulation, corridor liquidity, and interoperability remain the biggest hurdles to achieving a fully efficient global system.

The cross-border payments market, worth over $150 trillion annually, powers global trade, remittances, and commerce, yet it remains slow, costly, and inefficient. Transfers often take days, involve multiple intermediaries, and carry steep fees. This approach is increasingly challenged by the shift toward a digital, real-time economy.

By 2030, innovation and regulation will collide: central banks will test digital currencies, fintechs will build faster rails, and institutions will demand instant settlement. The race to modernize cross-border payments is intensifying, with four major contenders now under comparison, including:

XRP (Ripple): The blockchain veteran targeting instant, low-cost global settlement.

SWIFT: The entrenched incumbent linking over 11,000 banks, now reinventing itself for the digital era.

Each offers a distinct vision for the future of the global money movement. As 2030 approaches, the real question isn’t if disruption will happen, but which system will lead the next generation of cross-border payments.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

The global economy depends on the movement of money as much as goods and data. Yet, while communication is instant, cross-border payments remain outdated, slow, expensive, and opaque.

Most transfers still rely on correspondent banking networks, where funds pass through multiple intermediaries, each adding delay, cost, and compliance friction. Most cross-border transfers also rely on the correspondent banking system, a chain of intermediaries that adds delays, compliance checks, and hidden FX costs.

These frictions hit hardest in low- and middle-income corridors. Sending $200 costs an average of 6.2%, but over 8–9% in sub-Saharan Africa, the world’s most expensive region.

In the UK-Tanzania corridor, nearly $20 can be lost in fees and delays of up to five days. Similar bottlenecks persist in U.S.-Philippines, UAE-India, and EU-Nigeria routes, as many local banks must route through hubs like London or New York, duplicating AML and KYC checks.

The Pain Points

Speed: Transfers can take days to settle, hurting cash flow for individuals and businesses.

Cost: Average global fees remain around 6%, far above the UN target of 3%.

Transparency: Senders often have no visibility into where their money is or when it will arrive.

This inefficiency persists even as demand grows.

According to Karbon Business, the cross-border payments market already processes $150 trillion annually and could exceed $250 trillion by 2030.

Growth is driven by:

The expansion of global e-commerce and digital marketplaces.

The rise of remote work and cross-border gig payments.

Market size and growth by segment in cross-border payments. | Credit: FXC Intelligence EY analysis

The Transformation

Blockchain networks like XRPL and Stellar enable direct, near-instant settlement between parties, eliminating intermediaries.

Stablecoins like USDC and USDT move value across borders 24/7 with minimal fees.

CBDCs (Central Bank Digital Currencies) are being tested by over 130 central banks to enable programmable, interoperable digital money. However, critics warn that CBDCs could enable government overreach by allowing control over how money is spent, raising serious concerns about privacy and financial freedom. They also highlight risks of systemic failures, displacement of commercial banks, and question whether CBDCs truly solve issues existing digital payment systems already address.

Legacy systems like SWIFT, Visa, and Mastercard are integrating blockchain to modernize existing infrastructure.

Together, these forces are reshaping the global money movement. By 2030, international payments could be instant, affordable, and fully transparent, turning money into something that moves as freely as information.

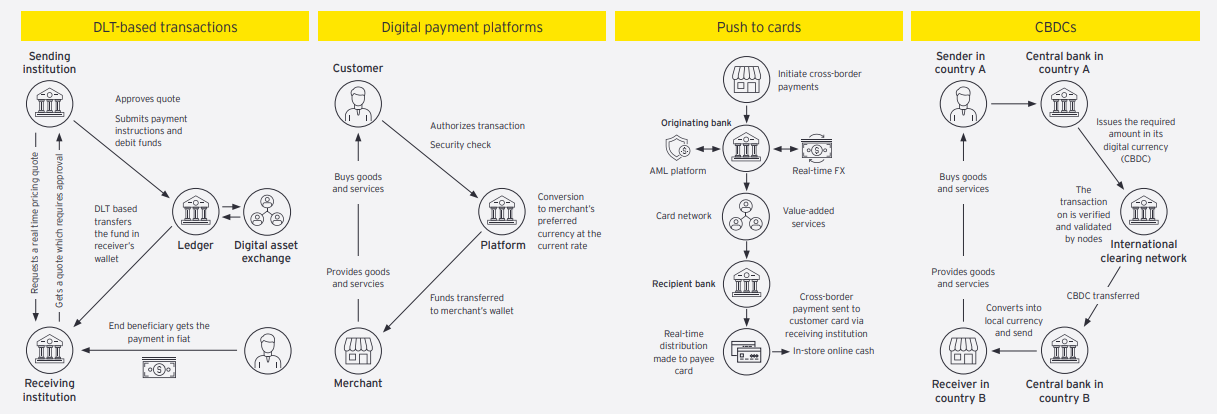

How CBDCs and Stablecoins Fit Into the Cross-Border Payments Race

The global push to modernize cross-border payments has created two leading contenders: CBDCs and stablecoins. Both aim to solve the same problem, making international money movement faster, cheaper, and more transparent, but they approach it from opposite directions.

Emerging alternative models poised to revolutionize cross-border payments. | Credit: EY

Traditional cross-border payments still rely on correspondent banking networks, where money passes through multiple intermediaries. This results in:

Delays: Transactions can take 2-5 business days.

High fees: Transfers often cost 5-10% of the amount sent.

Poor transparency: Senders can’t easily track payment progress or costs.

Innovation is urgent, as the global payments market is expected to top $150 trillion annually and grow toward $250 trillion by 2030.

CBDCs are digital versions of fiat currencies issued by central banks. They could revolutionize cross-border payments by enabling:

Instant interbank settlement between countries.

Programmable transactions with built-in compliance and FX conversion.

Transparency that reduces fraud and money laundering risks.

Projects like the BIS mBridge initiative and pilots in China and Europe are testing how multi-CBDC networks could replace slow legacy rails.

On the other hand, issued stablecoins such as USDC by Circle – which went public last yeat – and USDT by Tether and already handle trillions in on-chain payments yearly. They offer:

24/7 global settlement without banks or intermediaries.

Low-cost remittances are accessible via mobile wallets.

Seamless integration with fintech and DeFi platforms.

However, regulatory clarity remains challenging, with frameworks like the EU’s MiCA now emerging.

CBDCs bring regulatory trust; stablecoins bring agility and adoption. Together, they point to a future where money moves instantly, securely, and globally, a system where digital currencies interoperate to make payments as seamless as sending an email.

XRP Ledger (Ripple) – The Longstanding Contender

Among the many blockchain projects aiming to transform global payments, Ripple’s XRPL is one of the earliest and most tested blockchain networks for cross-border payments. Since its launch in 2012, Ripple has pursued a clear vision: to make cross-border money movement as fast and seamless as the internet.

Ripple set out to replace the outdated correspondent banking model with instant, low-cost settlement between financial institutions. Instead of moving money through a chain of intermediaries, Ripple uses the XRP Ledger (XRPL) as a neutral bridge asset, settling transactions in seconds, not days.

Speed: Average settlement time of 3-5 seconds, compared to days on traditional networks.

Cost efficiency: Transaction fees are often below $0.01, enabling micro and large-value transfers.

Liquidity solutions: Ripple’s On-Demand Liquidity (ODL) product uses XRP to provide real-time FX conversion, eliminating the need for pre-funded Nostro/Vostro accounts.

Real-World Adoption

Hundreds of institutions have integrated Ripple’s technology across over 55 countries, including major payment firms and remittance providers. ODL corridors operate between regions like Asia-Pacific, Latin America, and the Middle East, handling billions in volume annually.

Regulatory Challenges

Ripple’s long-running legal battle with the U.S. Securities and Exchange Commission (SEC) over whether XRP is a security has shaped its trajectory. With the court ruling that XRP itself is not a security when sold on exchanges, and with the case ended with a mutual deal between Ripple and the SEC, much of the regulatory cloud over Ripple has lifted.

Strategic Partnerships

Ripple maintains key relationships with Santander, SBI Remit, Tranglo, and Pyypl and connects banks, fintechs, and payment providers through its network. These partnerships underscore Ripple’s unique position: bridging the worlds of traditional finance and blockchain innovation.

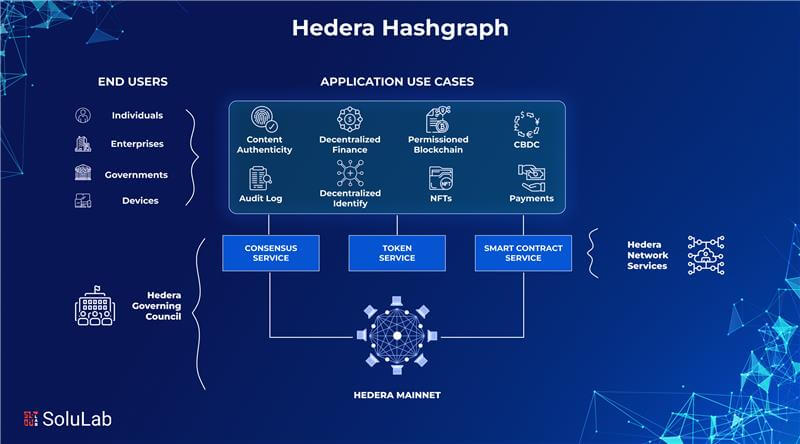

HBAR (Hedera Hashgraph) – The Enterprise Challenger

While most crypto payment networks are built on traditional blockchain architectures, Hedera Hashgraph takes a different route, designed for enterprise-grade speed, security, and stability.

Positioned as an institutional challenger in the race to modernize global finance, Hedera aims to provide the reliability of traditional systems with the efficiency of decentralized technology.

Hedera Hashgraph application use cases. | Credit: SoluLab

Unique Technology: Hashgraph vs. Blockchain

Unlike blockchains that bundle transactions into sequential blocks, Hedera’s hashgraph consensus uses a Directed Acyclic Graph (DAG) structure, allowing multiple transactions to be processed in parallel.

Consensus by gossip: Nodes share transaction data and reach agreement through “gossip about gossip,” enabling extremely high throughput.

Speed and fairness: Transactions achieve finality in seconds with predictable ordering, which is ideal for payment and enterprise use cases.

Security: Hashgraph offers asynchronous Byzantine Fault Tolerance (aBFT), one of the highest security standards in distributed systems.

Core Strengths

Scalability: Handles over 10,000 transactions per second with finality under 5 seconds.

Governancemodel: Managed by the Hedera Governing Council, a consortium of global corporations ensuring stability and compliance.

Environmental efficiency: It uses minimal energy and is verified as carbon-negative, making it one of the most sustainable DLTs.

Enterprise Adoption and Real-World Applications

Hedera’s credibility stems from its council members and enterprise users, including Google, IBM, Avery Dennison, LG, Boeing, and Standard Bank. These institutions govern the network and build real-world solutions, from supply chain tracking to carbon credit verification.

Avery Dennison’s atma.io uses Hedera for product authentication and supply chain transparency.

ServiceNow and DLA Piper leverage Hedera for document notarization and digital asset tokenization.

Carbon offset platforms use their efficiency for transparent environmental reporting.

Cross-Border Payment Potential

With its low latency, near-zero fees, and corporate trust model, Hedera is well-positioned to disrupt institutional cross-border payments. It offers banks and enterprises a compliant, eco-friendly alternative to legacy rails and public blockchains, a system where value can move globally with enterprise-grade assurance.

Its native token, HBAR, stands out as the enterprise-ready layer of the digital payments future, bridging decentralized innovation with the governance, performance, and compliance that global finance demands.

XLM (Stellar Lumens) – The Financial Inclusion Pioneer

In the global race to modernize payments, Stellar (XLM) has carved out a unique mission: bringing financial access to the unbanked and underbanked. Rather than targeting large banks or enterprises, Stellar focuses on remittances, low-cost transfers, and microtransactions, the payments that matter most to everyday people and small businesses in emerging markets.

A Mission of Inclusion

Founded in 2014 by Jed McCaleb, one of Ripple’s co-founders, Stellar was built to ensure digital money could reach those excluded from traditional banking. Its blockchain enables fast, affordable cross-border transactions, making it especially valuable in regions where high fees and limited access to financial services remain significant barriers.

Key Partnerships Driving Adoption

MoneyGram: Through the MoneyGram Access platform, users can convert cash directly into digital assets, including USDC on Stellar, and withdraw them again in local currency.

Circle (USDC): Stellar hosts USDC, enabling stable, dollar-denominated transfers on a low-fee global network.

Fintech startups: Companies like Tempo, Coinqvest, and Airtm use Stellar rails to power remittances, payroll, and payments across Latin America, Africa, and Southeast Asia.

These partnerships have made Stellar one of the most actively used blockchains for real-world remittance flows, connecting local cash economies to the global digital asset ecosystem.

Advantages in Emerging Markets

Low fees: Typical transaction costs are fractions of a cent, making microtransactions viable.

Speed: Payments settle in 3-5 seconds faster than bank wires or traditional money transfer services.

Accessibility: Designed for lightweight, mobile-friendly applications with minimal internet connectivity.

Challenges in Scaling

Stellar faces stiff competition from newer layer-1 networks, stablecoin issuers, and central bank pilots in emerging economies. Additionally, expanding liquidity and regulatory clarity remain ongoing challenges for broader institutional integration.

Even so, Stellar Lumens (XLM) stands out as the financial inclusion pioneer, a blockchain built not for speculation, but for affordability, access, and empowerment in the global digital economy.

SWIFT – The Incumbent Powerhouse

No name carries more weight regarding cross-border payments than SWIFT, the Society for Worldwide Interbank Financial Telecommunication.

Founded in 1973, SWIFT underpins the global financial system, connecting more than 11,000 banks and financial institutions across over 200 countries. Every day, it facilitates the secure messaging behind trillions of dollars in international transfers, making it the backbone of traditional cross-border banking.

SWIFT usage. | Credit: Decentro

A Global Network Built on Trust

SWIFT doesn’t move money itself; it transmits the instructions that tell banks where and how to send funds. Its power lies in its unmatched network reach, regulatory credibility, and institutional trust. For decades, governments, central banks, and significant financial institutions have relied on SWIFT as the global standard for secure, compliant messaging and settlement coordination.

Innovation to Stay Relevant

As fintechs, blockchain networks, and stablecoin systems threaten to outpace it, SWIFT has launched a series of modernization efforts:

SWIFT GPI (Global Payments Innovation): Introduced to improve transparency and speed, GPI lets users track payments in real time, reducing settlement from several days to just hours in many corridors.

CBDC Integration: SWIFT is piloting connections between central bank digital currencies in different countries – Australia, Germany, Thailand, Hong Kong among others – to serve as the interoperability layer between national digital currencies.

Blockchain Interoperability: In September 2025, the network announced plans to test cross-chain messaging systems enabling banks to transact across multiple blockchains, including Ethereum Layer 2s like Linea. The initiative aims to ensure secure interoperability with digital asset and CBDC platforms while remaining compatible with existing compliance and settlement systems..

Strengths and Weaknesses

Strengths:

Massive network reach: Over 11,000 member institutions ensure unmatched global coverage.

Despite its inefficiencies, SWIFT remains the incumbent powerhouse, a deeply entrenched network adapting to survive in a rapidly changing payments environment. Despite its inefficiencies, SWIFT remains a dominant force, evolving to stay relevant in a shifting payments landscape. Its push toward CBDC and blockchain interoperability, including pilots with Ethereum Layer 2s like Linea, shows its intent to bridge traditional finance with scalable, low-cost digital networks.

XRP vs. HBAR vs. XLM vs. SWIFT: Key Cross-Border Payment Differences You Can’t Ignore

All four networks aim to facilitate faster, cheaper, and more efficient cross-border money transfers than their competitors. They differ in who they serve best and how they get the job done.

If you’re paying a supplier or sending wages, waiting days can stall shipments or leave workers hanging:

XRP/XLM: Confirm payments in 3–5 seconds, about the time it takes to refresh a webpage. XRP is optimized for payments and FX pathfinding; XLM is lightweight and efficient for mobile-first, low-bandwidth environments.

HBAR: Settles in seconds as well, but focuses on predictable timing and ordering. Think enterprise-grade punctuality. The network offers deterministic (immediate), low-jitter finality that’s ideal for enterprise use.

SWIFT’s GPI: Dramatically improved the old wiring experience. 60% of transactions are credited within 30 minutes, and nearly all settle within 24 hours. With GPI Instant, some corridors now enable 24/7 settlement, though coverage depends on the domestic instant-payments infrastructure.

Example: A fashion brand in Los Angeles needs to pay a cotton supplier in Dhaka before a shipment leaves port:

XRP/HBAR/XLM: Funds confirm while the freight forwarder is still on the phone.

SWIFT: Vastly better than traditional wires, but you still have to plan around business and bank hours.

Transaction Costs and Money Management (Fees vs. Total Cost)

A $200 remittance losing 6-8% in fees/FX is painful. For businesses, capital stuck in pre-funded accounts is essentially dead weight. Here’s how some of the networks handle the following:

On-chain fees: XRP, HBAR, and XLM transactions typically cost fractions of a cent ($0.001 or less). The bigger issue is FX and corridor liquidity.

Ripple ODL: Uses XRP as a bridge asset to eliminate the need for pre-funded Nostro/Vostro accounts, cutting FX costs in high-volume corridors.

SWIFT: Coordinates liquidity among banks. Intermediaries add time, compliance checks, and spreads, especially for smaller transfers.

Say that a cafe owner in London pays a roaster in São Paulo in BRL every week:

XRP (ODL): Buys XRP in GBP, then sells XRP for BRL in seconds—no pre-funded BRL account needed.

SWIFT: Strong option for recurring invoices but still subject to FX spreads and bank cutoffs.

XLM: Pay in USDC on Stellar and settle near-instantly with minimal fees. Conversion to BRL depends on available local on/off-ramps.

HBAR: Executes the invoice with low fees and predictable, seconds-fast finality.

Scalability

All four networks scale, just differently:

HBAR: Optimizes throughput and predictable timing, which is ideal for enterprises.

XRP/XLM: Efficient for high volumes of repetitive payments. Scaling constraints are less about ledger limits and more about corridor liquidity and on/off-ramp availability.

SWIFT: “Scales” through its 11,000+ institutions and evolving data standards. Reach is unmatched, but ultimate delivery speed still depends on batch queues and local banking hours.

Example: A payroll platform has to push 50,000 micropayments across 12 countries in a day:

HBAR: Handles bursts of high volume with deterministic finality.

XRP/XLM: Well-suited for rapid, repetitive transactions, liquidity being the key constraint.

SWIFT: Global reach, but delivery time depends on local rails and banking schedules.

Adoption and Partnerships

Each rail has a “home turf,” which shows in who integrates it first:

XRP: Skews toward payment firms/remitters and FX-heavy corridors.

HBAR: Learns toward the enterprise/public sector through its governing council and systems integrators.

XLM: Widely used for remittances, especially when paired with USDC and MoneyGram’s cash-in/out network.

SWIFT: The bank-to-bank default, increasingly experimenting with CBDC interoperability and tokenized assets.

Example: A non-profit entity needs to send $150 stipends across rural areas in one week. Here’s how that could work:

XLM: Paired with USDC, stipends can be cashed out locally (MoneyGram covers 170+ countries).

XRP: Effective if both sender and receiver use supported wallets/exchanges with corridor liquidity.

HBAR: Strong when run through a government or enterprise program.

SWIFT: Best when sending directly to bank accounts, especially for already-banked recipients.

Governance and Trust (Who’s Accountable)

Institutional adoption often comes down to “Who do we call if something breaks?”

HBAR: Governed by a term-limited council of global organizations (equal voting rights, capped at 39 members).

XRP: Open ledger + Ripple as the commercial vendor = hybrid trust model.

XLM: Overseen by the Stellar Development Foundation, with an open community-driven ecosystem.

SWIFT: Member-owned cooperative with long-standing regulatory integration.

Example: A regional bank’s risk committee evaluates a new payment rail:

HBAR: Enterprise-grade governance and deterministic finality ease approvals.

SWIFT: Familiar standards and risk-screening frameworks.

XRP/XLM: Approval depends on local regulatory clarity and custody rules.

Long-term Sustainability

Sustainability refers to energy use and operating durability:

HBAR: Low-energy footprint (0.000003 kWh/tx) and long-term, forward-thinking governance via its rotating council.

XRP/XLM: Low-energy payment ledgers, especially when compared to proof-of-work (PoW) chains.

SWIFT: SWIFT’s messaging infrastructure isn’t constrained by blockchain energy debates, as it operates within existing bank data systems.

Example: A city government sets up a decade-long subsidy program with strict audits:

HBAR: Deterministic finality plus verifiably low emissions makes it a strong fit.

XRP/XLM: Lightweight, energy-efficient rails for recurring payouts.

SWIFT: Guarantees continuity and compliance while upgrading standards over time.

What Will the Cross-Border Payment Market Look Like in 2030?

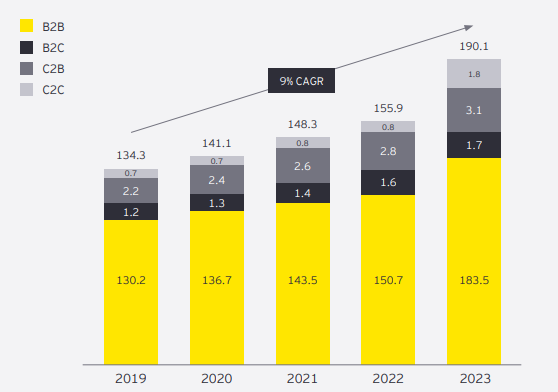

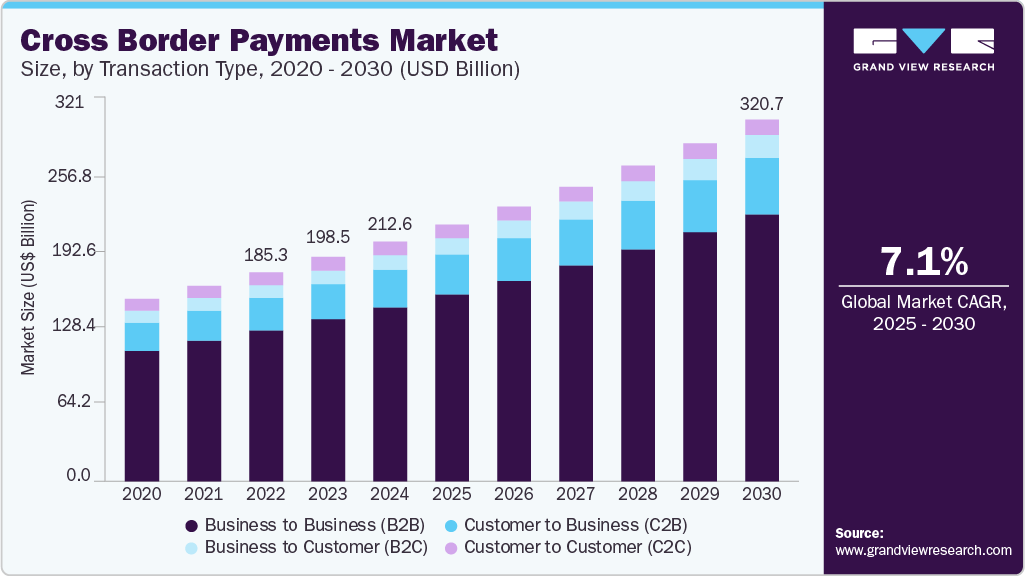

By 2030, cross-border payment flows are projected to grow significantly, from about $190 trillion in 2023 to nearly $290 trillion, with business-to-business transfers accounting for the largest share.

Retail segments such as e-commerce, digital remittances, and gig economy payments will also expand rapidly. Market revenues from payment services themselves are expected to surpass $300 billion by the end of the decade.

The industry will see broad adoption of real-time settlement, richer messaging standards such as ISO 20022, and greater use of application programming interfaces for transparency and automation.

Cross border payments market forecast. | Credit: Grand View Research

Central bank digital currencies are being piloted in more than 100 jurisdictions, with many initiatives focused on cross-border interoperability. Stablecoins already process trillions in value annually and will continue to play a role in faster, lower-cost transfers, though their use depends on regulatory clarity.

SWIFT’s network of over 11,000 banks is modernizing with GPI and instant connections, while blockchain-based rails like XRP Ledger, Stellar, and Hedera Hashgraph pursue efficiency in different market niches.

The future market is expected to be hybrid: legacy institutions, CBDCs, stablecoins, and decentralized networks will coexist, with corridor liquidity, compliance, and interoperability determining which rails dominate specific use cases.

Risks & Constraints (What May Hold Back Ideal Adoption)

Regulatory fragmentation: Different countries having divergent rules on stablecoins, digital assets, capital controls, AML/KYC will slow seamless integration.

Corridor liquidity & on/off-ramp constraints: Just having a fast rail isn’t enough; if one side lacks liquidity or exchange infrastructure, delays or costs persist.

Legacy inertia and bank resistance: Large financial institutions, accustomed to correspondent banking, may be slow to adopt or risk-averse about new rails.

Cost pressures on margins: As competition increases, profit margins on transaction services may shrink, making business models tighter.

Interoperability challenges: Ensuring different rails (SWIFT, CBDCs, token rails) talk seamlessly will be a major technical and governance hurdle.

Conclusion

The cross-border payments market is on the verge of its most significant transformation in decades. By 2030, global flows are projected to approach $290 trillion, with technology-driven rails enabling faster, cheaper, and more transparent transfers.

Blockchain networks like XRP, Stellar, and Hedera are advancing new settlement models, while SWIFT continues to modernize with instant connections and CBDC interoperability. Stablecoins and central bank digital currencies add further momentum, but regulatory clarity, interoperability, and corridor liquidity will determine how these systems coexist.

The future is not about a single winner but about multiple networks working in parallel, each serving specific niches in a hybrid, digital-first global economy.

Unlikely. SWIFT is deeply entrenched, connecting over 11,000 banks, and is modernizing through GPI and CBDC pilots. Blockchain networks will complement rather than fully replace it.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy