RippleNet and R3 Corda Code Confirm XRP’s ISO 20022 and SWIFT-Ready Infrastructure — Here’s the Proof

Share

Key Takeaways

Global payments giant SWIFT pilots an Ethereum Linea-based ledger to extend its role as a neutral infrastructure provider for tokenized deposits.

The XRP Ledger embeds settlement directly into the network using XRP as a bridge asset, promising instant, low-cost transfers.

SWIFT emphasizes compliance-friendly, token-agnostic plumbing trusted by banks.

Banks and regulators may prefer SWIFT’s permissioned, neutral design, while fintechs and disruptors could gravitate toward XRPL.

Cross-border payments are entering a new era. For decades, SWIFT has acted as the invisible backbone of global finance, a neutral messaging system that allowed banks to move trillions of dollars daily across borders. But as blockchain technology matures, new models of settlement are challenging that legacy.

On one side, SWIFT is experimenting with an Ethereum-based ledger, designed to extend its reputation as a provider of neutral financial infrastructure. Instead of pushing a single asset, its system aims to support tokenized deposits, central bank digital currencies (CBDCs), and stablecoins within a permissioned, compliance-friendly environment.

On the other hand, Ripple’s XRP Ledger (XRPL) represents the opposite philosophy: a native settlement network, powered by the XRP token as a built-in bridge for liquidity. By embedding the asset into the rail itself, XRPL promises speed, lower costs, and instant settlement, but it also inherits the risks of volatility and regulatory scrutiny.

The debate is no longer just about technology.

It’s about two competing visions for the future of cross-border finance: neutral pipes trusted by banks versus crypto-native rails where liquidity comes from the token itself. The outcome may shape how money moves across the world in the decades ahead.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

What SWIFT Means by “Financial Infrastructure Neutrality”

Neutrality has defined SWIFT since its creation. Unlike a bank or payment processor, it does not issue money, hold balances, or take currency risk. Its role has always been the plumbing, providing secure, standardized messaging so banks can transact without being forced into a particular asset.

The move toward a blockchain-powered ledger extends this same principle. The system is token-agnostic and permissioned, designed to let banks settle using regulated digital money without a SWIFT-issued token. That way, SWIFT provides shared rails that institutions can trust, avoiding conflicts of interest.

Tom Zschach, SWIFT’s Chief Innovation Officer, has stressed why this matters. As he put it, “institutions don’t want to live on a competitor’s rails,” underlining why neutrality appeals to banks balancing compliance and sovereignty. He has also noted that “surviving lawsuits isn’t resilience. Neutral, shared governance is,” pointing to the importance of transparent rules rather than dependence on a single token economy.

Tom Zschach’s Ripple critique. | Source: Tom Zschach on LinkedIn

Yet neutrality is not absolute.

Permissioned systems must still decide who can join, who sets standards, and how disputes are resolved. Critics argue this governance is shaped by large member banks, and that excluding native assets may limit the liquidity advantages that networks like XRPL can provide. Neutrality reassures institutions, but it comes at the cost of built-in liquidity.

Ripple’s XRPL: Native Token Settlement Through XRP

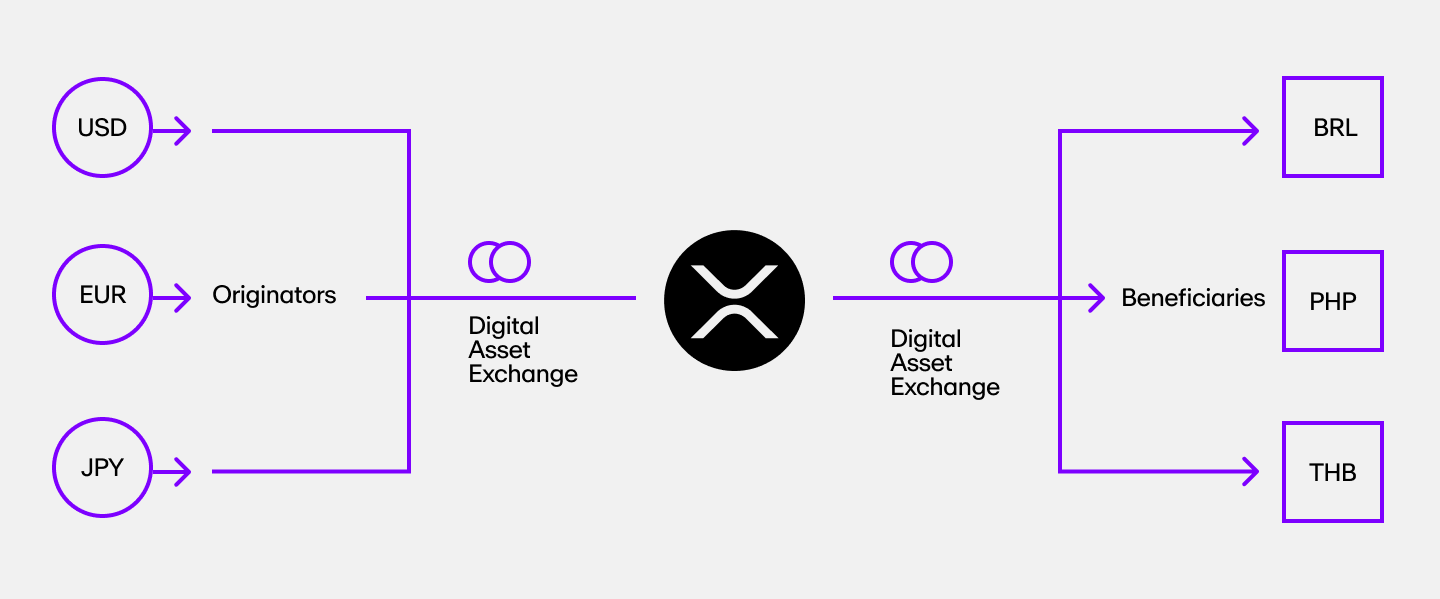

Ripple’s XRP Ledger (XRPL) is built around XRP as a native bridge asset for liquidity. Instead of relying on pre-funded nostro/vostro accounts, institutions can convert value into XRP, send it across the ledger instantly, and then settle back into local currencies.

This design speeds up settlement but ties the network’s success directly to the token itself and is not neutral. That reliance creates both advantages and risks.

How value transfer flows through the XRP Ledger. | Source: MoonPay

Benefits

Faster settlement: Near-instant cross-border transfers compared to the days it can take with correspondent banking.

Lower costs: Reduces the need for multiple intermediaries and pre-funded accounts.

Bridge liquidity:XRP can serve as a neutral connector between illiquid or exotic currency pairs, making settlement possible in underserved corridors.

Inclusive design: Useful for fintechs and payment providers outside the traditional banking system.

Regulatory scrutiny: Regulatory scrutiny of XRP can impose idiosyncratic risk on the rail.

Dependence on a single asset: The system’s efficiency is tied to XRP liquidity, which may be uneven across markets.

Governance questions: Concerns remain over validator distribution and the long-term decentralization of the network.

Ripple’s ILP Puts XRP at the Core of Global Payments

Ripple’s Interledger Protocol (ILP) was developed to enable value transfer across different networks. Unlike traditional blockchains, ILP does not create a new ledger. Instead, it synchronizes existing ones, allowing interoperability between financial systems without requiring them to operate on the same infrastructure.

The design has parallels with SWIFT’s role in global banking, where the processing of a payment message results in binding obligations between institutions. ILP extends this model by enabling native settlement capabilities through the XRPL, as highlighted by researcher SMQKE on X.

Ripple’ ILP vs. SWIFT debate | Source: @SMQKEDQG on X.

By aligning with SWIFT messaging practices and ISO 20022 standards, ILP is structured to integrate with existing financial networks while providing the option to use XRP as a bridge asset.

Ripple has emphasized that “the world will never agree on one ledger.” ILP reflects this principle by acting as a universal protocol that connects otherwise fragmented systems in a secure and scalable way.

How SWIFT Plans to Use Ethereum’s Linea for Blockchain-Powered Payments

Most people know SWIFT as the behind-the-scenes network that helps banks send money across borders. When you wire money abroad, it usually travels through SWIFT messages that tell banks how and when to move the funds. But SWIFT doesn’t actually move the money itself, it just passes the instructions.

Now, SWIFT is experimenting with something bigger: using blockchain technology to handle not only the messaging, but also the actual settlement of value. And its blockchain pivot isn’t built on XRP Ledger or Hedera Hashgraph, it’s anchored in Linea, the Ethereum layer-2 developed by Consensys.

The choice reflects SWIFT’s priorities: scalability, regulatory compliance, and neutrality. Linea’s zkEVM architecture bundles transactions together off-chain and then secures them on Ethereum. This design gives institutions the speed and privacy of zero-knowledge proofs while avoiding the volatility of relying on a native token. For SWIFT, that means it can extend its role as neutral financial infrastructure, providing the pipes for tokenized deposits, CBDCs, or stablecoins, without being tied to a single asset ecosystem.

What is Linea?

Think of Ethereum as a busy global highway: secure, proven, but often crowded and expensive at peak times.

Linea is like a fast side road (L2) that handles many cars at once, then feeds a single “receipt” back to the main highway to prove that the traffic moved correctly. This setup lets banks get the best of both worlds, high throughput and lower costs, with the security of Ethereum anchoring it all.

How SWIFT Would Use It

On this new ledger, banks could create digital versions of money, tokenized deposits, regulated stablecoins, or CBDCs. Instead of just sending messages, they could actually move those tokens across borders in real time, 24/7.

Compliance checks such as identity verification or transaction size limits could be automated through smart contracts, embedding regulation into the settlement layer itself.

SWIFT’s Ledger: Token-Agnostic, Not Token-Issuing

Unlike Ripple’s XRPL, which is built around the XRP token, in announcing its blockchain-based shared ledger, SWIFT explicitly states that it will “work with financial institutions to define the types of tokens that can be exchanged on the ledger” — implying that token issuance is a function delegated to banks or central banks, not SWIFT itself.

Historically, SWIFT has always functioned as a messaging network, not a settlement or account-holding entity. It has no role in keeping accounts or conducting the actual settlement of funds, that is handled by banks and central banks.

This “neutral plumbing” approach is designed to reassure banks and regulators that SWIFT is not promoting one particular asset, but simply providing the infrastructure to move whatever assets institutions choose.

That said, these statements are forward-looking and conceptual. SWIFT is still building a prototype, and its ultimate design and governance could evolve.

Who’s Testing It?

SWIFT is collaborating with more than 30 global financial institutions to develop a shared blockchain ledger focused initially on real-time, 24/7 cross-border payments.These pilot participants include large banks such as JPMorgan, HSBC, Deutsche Bank, Citi, BNP Paribas, Santander, and others.

Neutral vs. Native: Key Differences in SWIFT and Ripple’s Design Philosophy

SWIFT remains the undisputed backbone of institutional payments, processing over $5 trillion daily across its network of more than 11,000 financial institutions. For example, when a multinational like Siemens or Nestlé pays suppliers overseas, those flows are routed through SWIFT’s trusted rails, ensuring compliance, standardized messaging, and settlement between regulated banks.

By contrast, Ripple’s XRPL and XRP are gaining traction in niche but growing corridors. Tranglo in Southeast Asia and SBI Remit in Japan utilize XRP as a bridge asset to reduce costs and deliver near-instantaneous remittances.

Bitso in Latin America has also leveraged XRP for cross-border crypto-to-fiat transfers between the U.S. and Mexico, enabling migrant workers to send money home more cheaply than with banks or Western Union.

However, because SWIFT’s blockchain ledger is still in development, its vision of neutral infrastructure remains largely conceptual and that means inevitable tradeoffs.

SWIFT will need to decide who gets to issue tokenized assets, how compliance rules are enforced, how governance and upgrades are managed, and how interoperability with existing banking rails and other blockchains is ensured, all without the anchor of a built-in token providing liquidity.

By contrast, Ripple’s XRPL is already live, but it carries its own tradeoffs. Its reliance on XRP as a bridge asset exposes users to token volatility, ongoing regulatory scrutiny, and questions around validator trust and decentralization.

Each approach reflects a different philosophy: SWIFT leans toward institutional comfort and regulatory fit, while XRPL emphasizes embedded liquidity and crypto-native efficiency.

SWIFT vs. Ripple: Who Gains the Edge in Cross-Border Payments?

Cross-border payments have always been shaped by the infrastructure of trust. In the early 20th century, global trade and finance operated under the gold standard, where the value of money was anchored to physical gold reserves. This provided a common benchmark but was slow, rigid, and vulnerable to crises.

After World War II, the Bretton Woods system shifted that anchor to the U.S. dollar, with the Federal Reserve and U.S. Treasury at the center. Trust in dollar clearing, not gold, became the backbone of international finance.

When SWIFT was founded in the 1970s, it emerged as the digital messaging layer for this dollar-led financial order. SWIFT didn’t settle transactions itself, correspondent banks and central banks did, but it became the trusted “language” that allowed trillions of dollars, yen, pounds, and euros to move securely each day. Its neutrality, avoiding issuance of money, was part of its strength: it provided plumbing, not policy.

Ripple’s XRP Ledger (XRPL) challenges that legacy by embedding settlement into the infrastructure itself, using a native token, XRP, as a bridge asset for liquidity. This represents a philosophical break. Instead of correspondent banks holding nostro-vostro accounts and reconciling ledgers over days, XRPL promises near-instant atomic settlement, with the token itself acting as the liquidity lubricant. It recalls the gold standard era, where settlement was tied directly to a tangible reserve, but now it’s a digital reserve native to the chain.

Other blockchain payment networks take different approaches. Hedera Hashgraph emphasizes high throughput, predictable fees, and strong governance. It makes it attractive for institutions that want to issue and move tokenized assets without relying on a volatile bridge token. Meanwhile, Stellar focuses on simplicity and accessibility: its lightweight consensus protocol and low fees are designed for remittances, micro-payments, and emerging markets, where cost and inclusivity matter most.

Together, XRPL, Hedera, and Stellar show that crypto-native settlement isn’t one-size-fits-all. Each reflects a different philosophy, XRPL’s native liquidity, Hedera’s governed tokenization, and Stellar’s inclusive low-cost design, all of which stand in contrast to SWIFT’s neutral, token-agnostic rails.

Practical Adoption Scenarios

Banks and regulators are likely to prefer SWIFT’s new Ethereum Linea-based ledger. It preserves the traditions of neutral infrastructure, no native token, permissioned governance, and compatibility with tokenized fiat, stablecoins, and CBDCs. This makes it easier to fold into existing compliance frameworks.

Fintechs, crypto exchanges, and payment disruptors may lean toward Ripple’s XRPL. Its native asset, XRP, can provide open liquidity without waiting for tokenized fiat arrangements between banks. For corridors underserved by the banking system, XRPL offers speed, accessibility, and lower entry barriers.

Coexistence Rather Than Winner-Takes-All

Just as gold and dollars coexisted for decades before the dollar became dominant, it’s likely that SWIFT’s neutral ledger and Ripple’s XRPL will serve different niches. SWIFT may continue to anchor regulated, institution-to-institution transfers where compliance and legal enforceability are paramount.

At the same time, XRPL and other crypto-native networks could thrive in high-speed corridors, retail-facing applications, or geographies where banks are less dominant.

The future of cross-border payments may not hinge on one rail replacing another, but on layered coexistence, neutral pipes trusted by banks, alongside token-driven networks that offer speed and liquidity to a broader ecosystem.

In this mosaic, Hedera could provide governed rails for tokenized assets. Stellar instead remains focused on low-cost remittances and emerging markets.

History suggests that financial infrastructures evolve through overlapping phases rather than abrupt replacements. SWIFT, Ripple, Hedera, and Stellar may all gain the edge, but in different ways and in different corridors.

Conclusion

Cross-border payments are entering a phase of pluralism rather than monopoly. SWIFT’s Ethereum-based ledger seeks to preserve its role as the trusted, neutral backbone of institutional finance. Ripple’s XRPL embodies a crypto-native vision built around token-driven liquidity.

Hedera and Stellar add further diversity, each optimized for different needs, governed tokenization in one case, inclusivity and cost-efficiency in the other.

Instead of a single winner, the future may resemble a layered ecosystem where banks, fintechs, and decentralized networks all operate side by side. Neutral infrastructures will appeal to regulators and global institutions, while token-native rails may power faster, cheaper flows in corridors underserved by traditional banking. As history shows, financial systems evolve through coexistence and gradual integration.

The next era of cross-border payments will likely be defined not by one rail replacing another, but by how these different approaches interconnect to move value across the world.

For decades, SWIFT has provided the messaging layer for banks to transfer money, but settlement remained slow and costly. With blockchain technology maturing, new models are emerging that can move money instantly and at lower cost.

What is SWIFT’s new approach?

SWIFT is experimenting with a blockchain ledger built on Ethereum’s Linea. The system is token-agnostic, meaning banks can settle using tokenized deposits, CBDCs, or stablecoins in a permissioned environment—without relying on a SWIFT-issued or crypto-native token.

What are the main trade-offs between SWIFT and Ripple?

SWIFT is ompliance-friendly, bank-trusted, token-agnostic, but slower to adopt liquidity innovations.On the other hand, Ripple’s XRPL is faster and cheaper with native liquidity, but dependent on XRP’s market performance and regulatory status.

Who’s testing SWIFT’s blockchain system?

Over 30 major financial institutions, including JPMorgan, HSBC, Citi, BNP Paribas, and Deutsche Bank, are collaborating on SWIFT’s pilot projects.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy