Tanzania tops global remittance costs at $115 to send $200. Could stablecoins finally make money transfers cheaper, faster, and fairer? | Credit: Hameem Sarwar/CCN.com

Share

Key Takeaways

Tanzania is now the most expensive remittance corridor globally.

High costs stem from limited competition, weak financial infrastructure, regulatory burdens, currency volatility, and inefficient cross-border systems.

East Africa broadly struggles with high costs, but Kenya’s success with M-Pesa shows that innovation can lower barriers and improve efficiency.

However, there may be a solution: stablecoins.

Remittances are a lifeline for millions of families across Africa and beyond. They represent more than just financial transfers, they are a direct link between diaspora communities and their loved ones back home, helping to fund education, healthcare, housing, and small businesses.

Yet, for many countries, the cost of sending money remains painfully high. According to the latest data, Tanzania now holds the dubious distinction of topping global remittance costs, with some transaction fees reaching a staggering $115 for just a $200 transfer. This is more than half of the total sum being sent, a clearly unsustainable situation.

The question now being asked is: can new technologies like stablecoins and blockchain-based payment rails step in to offer a fairer, faster, and more affordable system?

To answer this, it’s essential to understand why remittance costs are so high, how Tanzania compares to its neighbors, and whether stablecoins can realistically fix this broken system.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Why Sending Money to Tanzania Is So Expensive: Cross-Border Inefficiencies and Intermediaries

Globally, the average cost of sending remittances hovers around 6%, far above the United Nations Sustainable Development Goal (SDG) target of 3%. In Sub-Saharan Africa, this figure is even higher, sometimes exceeding 9%.

Tanzania, however, has recently emerged as one of the most expensive corridors for remittances in the world.

Imagine sending $200 to your family—and paying $115 in fees. That’s the reality in Tanzania, which ranks highest for remittance costs 💸

There are several reasons why Tanzanian remittances are so costly:

Limited competition: A few money transfer operators dominate the market, allowing them to charge exorbitant fees.

Poor financial infrastructure: Weak digital payment systems and low banking penetration create reliance on cash-based methods, which are expensive to administer.

Regulatory hurdles: Strict anti-money laundering (AML) and know-your-customer (KYC) requirements increase compliance costs, which are passed on to consumers.

Currency volatility: The Tanzanian shilling has been under pressure, increasing foreign exchange spreads.

Cross-border inefficiencies: Transfers often go through multiple intermediaries, each taking a cut before the money arrives at its final destination.

This combination of structural and operational problems makes Tanzania a challenging and costly remittance market.

The Human Impact: $115 Is Not Just a Fee, It Hurt Families and Students

For context, Tanzania’s GDP per capita hovers around $1,200 annually. A $115 fee represents nearly 10% of an average Tanzanian’s annual earnings. Families who depend on remittances are effectively being punished for trying to support one another across borders.

Imagine a Tanzanian student in Europe who wants to send $200 home to help with school fees. Instead of their family receiving the full amount, more than half could be eaten up by fees and exchange spreads. The money that should pay for books, uniforms, or hospital bills ends up in the pockets of intermediaries.

The result is a vicious cycle: high fees discourage formal remittances, leading people to use informal channels, which are riskier and less regulated.

This undermines financial inclusion and prevents policymakers from fully understanding the scale of diaspora contributions.

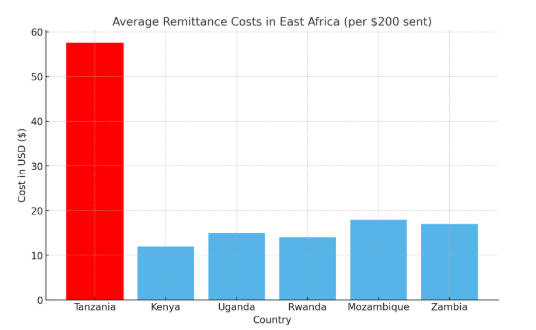

How Tanzania’s Remittance Costs Compare to Its East African Neighbors

While Tanzania is currently topping the charts for high remittance costs, it’s not the only country in East Africa struggling with this issue. Looking at its neighbors gives us a clearer picture:

Kenya: Known for its pioneering mobile money platform M-Pesa, Kenya has somewhat reduced remittance fees. While still above the global average, fees are typically lower than in Tanzania, between 5% and 9%.

Uganda: Remittance costs remain high, with many operators charging upwards of 10% for small transfers. Still, it does not approach the $115 extremes seen in Tanzania.

Rwanda: As a smaller market with a growing fintech ecosystem, Rwanda has been experimenting with digital solutions, though fees remain elevated compared to global norms.

Mozambique and Zambia: Both countries face similar challenges, including weak infrastructure and high cash dependence, which keep costs high.

Average remittance costs in East Africa per $200 sent. | Creit: Statista

This regional comparison shows that while Tanzania stands out for its exorbitant costs, high remittance fees are a systemic East African challenge. However, Kenya’s relative success with mobile money highlights that innovation can make a difference.

Stablecoins as a Potential Solution for Tanzania’s High Remittance Costs

However, a solution may already exist. Stablecoins are cryptocurrencies pegged to the value of stable assets like the U.S. dollar or euro. Unlike Bitcoin, their value does not fluctuate wildly, making them more practical for everyday transactions and cross-border transfers.

Lower fees: Stablecoin transfers on blockchain networks can cost just a few cents, compared to double-digit percentages through traditional remittance channels.

Speed: Instead of waiting several days, transfers can settle within minutes.

Accessibility: Tanzanians could receive money directly into a digital wallet with only a smartphone and an internet connection.

Transparency: Blockchain technology ensures that transfers are traceable and secure.

Currency protection: If pegged to the U.S. dollar, stablecoins shield recipients from local currency volatility.

For example, a Tanzanian abroad could buy USDC, send it to a family member’s mobile wallet, and the family could either use it directly with merchants (if accepted) or cash out through local crypto exchanges and agents.

Barriers to Stablecoin Adoption in Tanzania

While the promise of stablecoins is compelling, several obstacles must be addressed before they can fully fix Tanzania’s broken remittance system:

Regulatory uncertainty: Many African governments, including Tanzania’s, remain cautious or outright hostile toward cryptocurrencies. Clear legal frameworks are needed.

On/off-ramps: For stablecoins to be useful, people need reliable ways to convert between digital tokens and local currency. Right now, this infrastructure is limited.

Digital literacy: Many Tanzanians, particularly in rural areas, may lack the knowledge or trust to use crypto wallets securely.

Internet access: Despite progress, internet penetration in Tanzania is still lower than in some neighboring countries, limiting who can access blockchain services.

Risk of exploitation: Without strong consumer protections, there is potential for scams and fraud.

These challenges mean that while stablecoins are a promising tool, they cannot be seen as a magic bullet. Collaboration between governments, fintech firms, and regulators is essential.

One possible solution is to combine the strengths of existing mobile money platforms with blockchain-based assets. Imagine if Tanzanians could receive stablecoin remittances directly into their M-Pesa wallets.

This would eliminate the need for users to navigate unfamiliar crypto apps while reducing costs and improving efficiency.

Some companies are already experimenting with hybrid models, building bridges between traditional mobile money and blockchain networks.

These efforts could bring the best of both worlds: regulatory compliance, consumer trust, and the affordability of digital assets.

Latin America: In countries like Venezuela and Argentina, where inflation has eroded trust in local currencies, stablecoins are increasingly used for remittances.

Philippines: Migrant workers in the Middle East use stablecoins to send money home more cheaply than through banks.

Nigeria: Despite government crackdowns, Nigerians are among the most active crypto adopters for remittances and peer-to-peer payments.

These examples show that stablecoins can thrive in environments with weak currencies, high fees, and strong demand for alternatives, conditions that mirror Tanzania’s situation.

The Road Ahead for Tanzania: Making Remittances Affordable

For Tanzania to transition from being the most expensive remittance corridor to a leader in affordable digital finance, several steps are needed:

Policy reform: Regulators must establish clear, supportive rules for stablecoins and blockchain payments while safeguarding against misuse.

Infrastructure development: Investment in crypto exchanges, agent networks, and mobile money integrations will be crucial.

Education campaigns: Public awareness programs can help build trust and digital literacy.

Regional collaboration: East African countries could harmonize regulations to create a larger, more competitive market.

Private sector innovation: Fintechs and diaspora groups must continue experimenting with new solutions tailored to local needs.

If these steps are taken, Tanzania could turn a crisis into an opportunity, leveraging technology to make remittances faster, cheaper, and fairer for millions of families.

Conclusion

Tanzanians can be charged up to $115 just to send $200 home, which is nothing short of exploitative. This highlights the urgent need for systemic reform in global remittances. While Tanzania currently tops the global charts for remittance costs, it doesn’t have to remain this way.

Though not a silver bullet, stablecoins offer a genuine chance to fix a broken system. By eliminating intermediaries, reducing fees, and providing faster settlement, they could transform remittances from a financial burden into a more seamless act of support and solidarity.

The journey will require bold policy choices, innovative business models, and grassroots education. But if successful, Tanzania could shed its reputation as the most expensive remittance market and become a pioneer in leveraging stablecoins for inclusive economic growth.

Why are remittances so crucial in Tanzania and Africa?

Remittances are more than money transfers; they’re a lifeline for families. They help cover school fees, healthcare, food, and small business funding. In many African countries, remittances often exceed foreign aid and investment in impact.

Why are remittance costs in Tanzania so high?

Tanzania faces structural and regulatory issues: limited competition among money transfer operators, weak financial infrastructure, strict compliance requirements, currency volatility, and cross-border inefficiencies. These factors push fees to unsustainable levels, sometimes as high as $115 for a $200 transfer.

How do Tanzania’s remittance costs compare to those of its neighbors?

Tanzania tops the charts globally for high fees, but its neighbors struggle. Kenya’s M-Pesa has helped lower costs somewhat, though they remain above the global average. Uganda, Rwanda, Mozambique, and Zambia also have high fees, but not as extreme as Tanzania’s.

What barriers stand in the way of stablecoin adoption in Tanzania?

Challenges include regulatory uncertainty, lack of reliable on/off-ramps to convert stablecoins into local currency, limited digital literacy, patchy internet access, and the risk of scams or fraud. Without clear policies and infrastructure, adoption will remain restricted.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy