Explore whether Ripple’s technology can thrive without relying on the $XRP token, a deep dive into its fintech future, strategy, and innovation. | Credit: CCN.com

Share

Key Takeaways

SWIFT’s blockchain project is evolutionary, not revolutionary. Its pilot with ConsenSys’ Linea is about modernization, not replacing Ripple tomorrow.

Ripple’s real hurdles are regulatory and competitive. Ongoing global compliance uncertainty and stablecoin rivals like USDC, PYUSD, and Fireblocks pose bigger challenges.

Banking and blockchain rivals are gaining ground. Networks like Stellar, Hedera, Algorand, and platforms from JPMorgan (Kinexys) and Citi are building powerful alternatives.

Trust and market sentiment remain Ripple’s toughest barrier. Post-FTX skepticism means even strong tech must overcome institutional caution and volatility fears.

SWIFT’s recent announcement of a blockchain-based payment ledger grabbed headlines worldwide. As the global interbank messaging system connecting more than 11,000 banks across 200 countries, its move into blockchain is seen as a major step toward modernizing cross-border payments.

The initiative, built in partnership with ConsenSys’ Linea, aims to enable real-time, 24/7 settlement while eventually integrating tokenized assets such as stablecoins and central bank digital currencies (CBDCs).

Yet experts caution that this development is more of a long-term modernization than an immediate disruption for Ripple. SWIFT’s greatest strength is its vast, trusted network, a scale that competitors can only dream of matching.

As Tom Zschach, SWIFT’s chief innovation officer, put it: “I get it. Ripple Labs impressed investors such as yours truly by building local banking partnerships and meeting trade regulations in dozens of countries. These achievements can’t hold a candle to SWIFT’s truly global presence and more than 11,500 banks.”

That said, SWIFT’s blockchain ambitions are evolutionary, not revolutionary. They reinforce its dominance rather than radically upend it.

For Ripple, whose blockchain-based RippleNet and XRP token target faster, crypto-native settlement, the immediate threat doesn’t come from SWIFT’s experiment.

Ripple’s bigger challenges lie elsewhere, such as in regulation, market trust, stablecoin competition, and rival blockchains.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

SWIFT’s blockchain experiments aren’t new. Its own announcements and press coverage show a clear timeline:

In March 2024 SWIFT publicly acknowledged the value of tokenized assets and shared ledgers.

By late 2024 it was running proof‐of‐concepts (e.g. “Project Guardian” for tokenized funds) and digital‐asset messaging trials.

The big leap came in September 2025, when SWIFT announced a collaboration with ConsenSys and over 30 financial institutions to build a blockchain-based “shared ledger” layer on top of its existing rails.

This new layer is designed for real-time 24/7 payments, tokenized deposits and CBDC interoperability. Importantly, SWIFT’s plans are still experimental: live trials of digital-asset transfers are planned for 2025–26, and no production-ready platform is yet deployed.

Why Ripple’s Model is Distinct

Ripple’s business model differs fundamentally from SWIFT’s legacy network. SWIFT has been primarily a messaging utility, notifying banks to move money, whereas RippleNet and the XRP Ledger aim to cut out intermediaries entirely. Its On-Demand Liquidity (ODL) solution uses XRP to bridge currencies in seconds, without pre-funded accounts.

That makes it leaner, but also riskier for banks that prefer the neutrality and “trust scaffolding” SWIFT has built.

Critically, SWIFT’s blockchain efforts do not directly replace Ripple’s offerings. SWIFT’s network spans 11,000+ institutions in 200+ countries, but its blockchain vision is still a supplement to that system. It could take years for the shared ledger to be built and adopted.

Meanwhile, Ripple’s XRP Ledger is a functioning network capable of 1,500 transactions per second, with final settlement in seconds.

SWIFT even chose an external L2 (Linea) for its pilot rather than Ripple’s XRP Ledger, indicating different technical paths.

In short, SWIFT is racing to modernize, but its pace and focus (bank messaging, compliance) mean it’s not an immediate “XRP killer.” Rippling out elsewhere, Ripple still faces more pressing challenges.

SWIFT vs. Ripple: Market Reach and Dominance

Recent SWIFT data shows that 90% of cross-border payments sent over SWIFT reach the beneficiary bank within an hour, ahead of the G20 target of 75% within one hour.

In terms of volumes, banks still dominate the cross-border payments space. According to FXC Intelligence, in 2023, banks accounted for 92% of B2B cross-border payments globally, managing flows of $27.8 trillion.

Some reports indicate that Ripple’s CEO believes XRP could capture up to 14% of the cross-border payment volume handled by SWIFT within five years, a bold projection, though not yet borne out in data.

From all this, SWIFT’s “market share” in traditional cross-border finance remains massive.

SWIFT’s dominance is structural:SWIFT’s systems are deeply embedded in correspondent banking, regulatory frameworks, and global finance. That gives it a vast existing “market share” that is hard to unseat.

Ripple’s share is narrow but potentially scalable: Ripple’s usage is more niche — certain corridors, remittance corridors, and institutional use via ODL. Its $2.3 billion in a quarter is meaningful but tiny compared to multi-trillion annual bank flows.

Ambitious growth targets face steep headwinds: The 14% target by Ripple’s leadership is aspirational. To get there, XRP / RippleNet must do more than speed up payments, it must win regulatory acceptance, bank trust, and displace existing rails in many markets.

Comparisons must account for tradeoffs: Ripple’s strength is speed, low cost and crypto-native rails. SWIFT’s strength is ubiquity, regulatory acceptance, and entrenched infrastructure. Even if Ripple captures a large share in some corridors, SWIFT will still dominate many others.

Ripple’s Competition Beyond SWIFT

While SWIFT’s blockchain experiment has drawn plenty of attention, Ripple’s most pressing competition comes from other fronts. The company operates in a fast-evolving ecosystem where regulations, rival stablecoins, competing blockchains, banking relationships, and broader market sentiment all play a role.

These factors often pose bigger challenges to Ripple’s growth than SWIFT’s gradual modernization.

1. Regulatory Drag: The SEC Case and Beyond

Ripple operates in a patchwork of regulations that pose continual challenges. In the U.S., the landmark SEC lawsuit (December 2020–August 2025) ended with a partial victory:

A judge ruled that XRP was not a security in retail exchange trades but was a security in institutional sales, imposing a $125 million fine.

The SEC has closed the case in Ripple’s favor on appeals, but the injunction (barring institutional sales without registration) remains.

Thus, Ripple still faces limitations and uncertainty at home.

While this was a partial win, it underscores a bigger issue: regulatory fragmentation.

In Europe, the MiCA framework requires strict licensing and disclosures for stablecoins.

In the U.S., bills like the GENIUS Act mandate audits, reserves, and charters.

In Asia, CBDC pilots (like China’s digital yuan) show central banks may sidestep private tokens altogether.

As NYSE President Lynn Martin said after FTX’s collapse: “Institutional investors will be unlikely to dip their toe in unless they understand the framework.”

For Ripple, this means even strong tech or partnerships could be undermined by changing rules and enforcement actions. Navigating SEC guidance, global legal regimes, and upcoming stablecoin regulations is arguably a bigger hurdle than any tech rivalry.

2. Stablecoin Wars: RLUSD vs USDC, PYUSD and Fireblocks

Ripple’s launch of RLUSD (Ripple USD) in 2024 signaled a pivot into stablecoins. By 2025, RLUSD’s market cap reached $700M—impressive, but dwarfed by rivals.

Circle’s USDC: The dominant regulated stablecoin with roughly $60 billion in circulation (as of Q1 2025). USDC enjoys broad exchange support, banking partnerships, and is part of Circle’s business (it even IPO’d to bolster confidence.

Tether’s USDT: USDT remains the dominant stablecoin by market cap and liquidity, making it a formidable rival to Ripple in payments and settlement. As of Q1 2025, Tether held around $98.5 billion in U.S. Treasury bills, representing about 1.6% of all outstanding T-bills, putting it on par with large institutional players in the debt markets. Meanwhile, Ripple’s stablecoin (RLUSD) is still very small ($667 million in market cap) compared to USDT’s scale.

PayPal USD (PYUSD): dollar-backed coin launched in 2023 by PayPal/Paxos. It leverages PayPal’s 400+ million users on PayPal/Venmo, and is designed for fast transfers and remittances. This gives PYUSD immediate reach in retail and small-business payments.

Fireblocks Stablecoin Payments Network: Beyond tokens themselves, providers are building rails. For instance, Fireblocks recently launched “The FireblocksNetwork for Payments” spanning 100+ countries, with 40+ liquidity and compliance partners. As Fireblocks CEO Michael Shaulov calls it: “the backbone of stablecoin payments,” uniting blockchains, local rails and fiat on-ramps.”

Each competitor has advantages:

USDC’s large reserves and backing by Mastercard/BlackRock money market funds, PYUSD’s brand and easy access via PayPal, Fireblocks’ neutral network.

RLUSD’s edge is its NYDFS charter and enterprise focus, but drawing banks (especially beyond RippleNet partners) away from these existing rails is difficult.

In short, Ripple faces a crowded and growing stablecoin market where incumbents and new entrants alike vie to be the default digital dollar.

Ripple’s XRP Ledger is not the only enterprise-friendly blockchain. Several networks claim high speed, security or bank uptake that rival Ripple’s niche. Key examples include:

Stellar (XLM): An open-source fork of Ripple’s code (both created by Jed McCaleb). Stellar uses a Federated Byzantine Agreement consensus, achieving fast (seconds-scale) finality. It can process “thousands of network operations per second” and targets remittances in emerging markets. IBM and MoneyGram have run pilots on Stellar, not Ripple.

Hedera (HBAR): A public DLT using an “asynchronous Byzantine fault-tolerant” gossip protocol and rely upon council-led governance (Google, IBM, LG). Hedera touts over 10,000 TPS and has traction in supply chain and finance.

Algorand (ALGO): Known for less than 10,000 TPS with instant finality. It has been chosen for national-scale projects (e.g. the Marshall Islands’ sovereign digital currency) and has backing from investors. Algorand’s pure-PoS model (no leaders, self-selection of block proposers) and recent focus on on-chain governance and sustainability (fee-sharing) appeal to institutions valuing decentralization and throughput.

Quant (QNT): Not a blockchain in itself but an interoperability layer (Overledger) that connects different blockchains for enterprise users. Quant’s QNT token grants access to its technology. Quant has partnered with the LACChain alliance (Inter-American Dev. Bank) to enable cross-border tokenized assets, as well as with firms like Oracle and SIA. Its focus is on “the money of the future” by letting banks integrate blockchain without replacing core systems. This contrasts with Ripple’s approach of offering its own ledger and token.

In comparison, the XRP Ledger supports 1,500 TPS on commodity hardware with 3–5 second settlement, using a unique-node-list consensus (neither PoW nor PoS).

Each of the above competitors has trade-offs: e.g. Hedera’s high throughput comes with a semi-centralized council, Stellar’s decentralization comes with smaller scale, and Algorand’s model is very decentralized but newer.

Ripple must demonstrate that its performance and network (including bridge technologies like Payment Channels) are at least as good as these alternatives.

The fact that banks might prefer one architecture over another, especially if regional (e.g. XLM in Asia, Algorand in Latin America), means Ripple can lose deals to these platforms.

4. Ripple’s Banking and Fintech Partnerships: Wins & Setbacks

Ripple has cultivated partnerships with banks and fintechs, but success has been mixed. On the positive side, Ripple now boasts over 100 institutional partners globally. Recent high-profile wins include:

BNY Mellon (U.S.): In July 2025, Ripple appointed BNY Mellon as custodian for RLUSD reserves. This lends credibility: BNY will hold the dollars backing Ripple’s stablecoin and provide transaction banking services, validating RLUSD’s enterprise-grade design.

SBI Holdings (Japan): In August 2025, Ripple signed an MOU with SBI Group and SBI VC Trade to distribute RLUSD in Japan. SBI, a giant Japanese financial conglomerate, plans to offer the stablecoin by Q1 2026, reflecting demand in Asia.

Chipper Cash / Yellow Card (Africa): In September 2025, partnerships with African payments platforms (Chipper Cash, VALR, Yellow Card) rolled out RLUSD in Africa. These deals aim to make cross-border transfers cheaper and tap remittance corridors.

However, some partnerships have fizzled.

MoneyGram (U.S.): after investing $30 million in 2019, MoneyGram ended its Ripple agreement two years early in 2021 amid regulatory uncertainty. Ripple’s CEO still held out hope of future cooperation, but it was a clear setback.

Other banks have run pilots with RippleNet or XRP but not scaled them, or quietly set up private DLT instead.

To address this, Ripple is refocusing on institutional infrastructure: in July 2025 it even applied for a U.S. national trust bank charter (the “Ripple National Trust Bank”). If approved, this charter would let Ripple operate nationally (bypassing state limits), hold RLUSD reserves directly, and integrate with Federal Reserve services – a bid to gain traditional banking trust.

Meanwhile, banks continue investing in their own solutions (consortium ledgers, FedNow, SWIFT’s Instant) and may prefer sticking with familiar rails until crypto is proven and regulated.

In effect, Ripple must convince cautious incumbents that its system is safe, a hard sell when incumbents can always point to SWIFT’s track record and growing ISO standards.

So Ripple’s integration with banks remains a work in progress. Winning BNY Mellon and SBI shows promise, but MoneyGram’s exit and slow adoption by large banks underscore how tough it is.

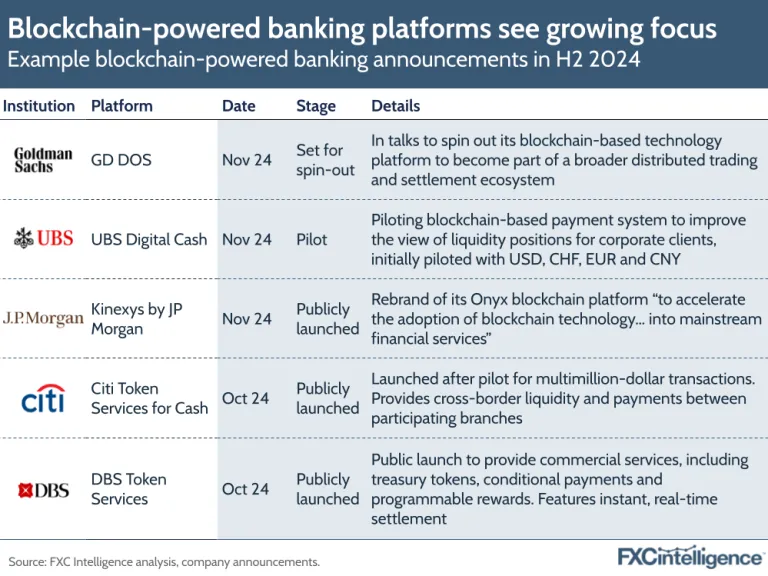

5. Rise of Blockchain-Powered Banking Platforms

Major banks aren’t just sticking with SWIFT, they’re building their own rails.

In September 2025, Citi integrated its Citi® Token Services platform with its 24/7 USD Clearing mechanism to deliver real-time, cross-border institutional payments. This setup enables liquidity management and payments across Citi and non-Citi accounts in near-instant fashion, with expansion plans beyond the U.S. and U.K. Citi’s Digital Assets arm also operates CIDAP, a platform for tokenization, FX settlement, custody and programmable asset workflows.

DBS is pushing into tokenization: it recently announced plans to issue tokenized structured notes on Ethereum for institutional investors. DBS has collaborated with Ripple and Franklin Templeton to enable trading and lending using tokenized money market funds and Ripple’s RLUSD stablecoin.

In late 2024, UBS piloted UBS Digital Cash, a private blockchain payment system handling cross-border and multi-currency settlement via smart contracts. UBS also offers UBS Tokenize, a platform for issuing and managing tokenized bonds, funds, and structured products, with blockchain-agnostic integration.

Blockchain-powered banking platforms see growing focus. | Credit: FXCintelligence

Non-Bank and Fintech Challengers

Beyond banks, non-bank players are taking meaningful share. Fintech platforms, money transfer firms, and infrastructure providers like Mastercard Move are partnering with banks to broaden capabilities. Non-bank B2B payments now account for about 6% of the market, a share that is steadily rising as SMEs and corporates seek faster, cheaper alternatives.

Thus, Ripple must offer compelling interoperability, regulatory safety, and cost advantages to remain relevant.

5. Market Volatility and Public Perception

No discussion of threats is complete without noting the volatile sentiment in crypto post-2022. The spectacular collapses of FTX (November 2022) and Terra/LUNA (May 2022) erased roughly $2–3 trillion in crypto market value. Investors and institutions have been shaken: regulators now routinely cite these events as justification for stricter rules.

This caution is evident in how the market reacts to stablecoins and exchanges:

Circle, the issuer of USDC, went public to prove transparency, and lawmakers inserted mandatory audits and reserves into bills. In other words, mainstream finance has become wary.

Morgan Stanley’s CEO put it bluntly: Crypto is too volatile and opaque for many clients. Any failure or rumor (even unrelated to Ripple) can cause broader unease that spills over to Ripple’s partnerships and pricing.

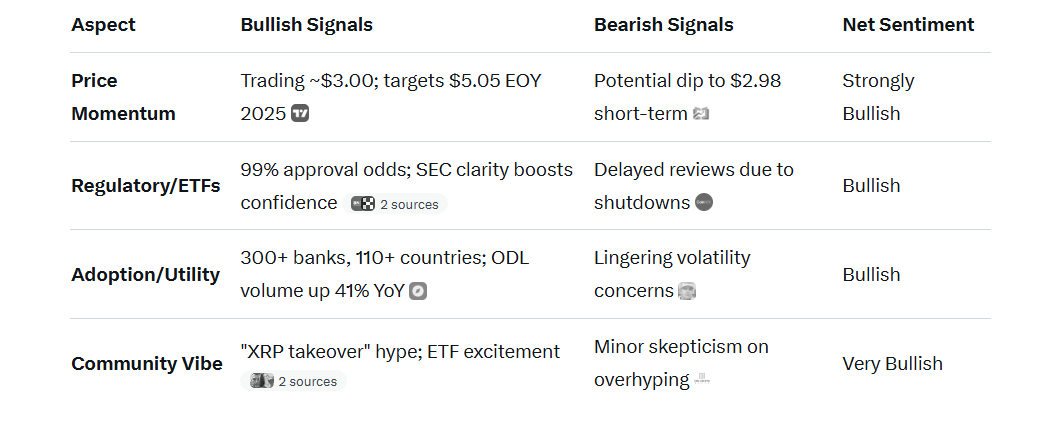

Grok’s Sentiment Analysis: Ripple, XRP, SWIFT for Cross-Border Payments

Grok reports a strongly bullish sentiment around Ripple and XRP, driven by a 400% price surge to $3.00, high ETF approval odds (95–99% by December), and growing adoption (300+ banks, 110+ countries, 41% YoY ODL volume growth).

Prompt for Grok.

Social media on X reflects excitement over XRP’s utility and partnerships, though minor concerns include U.S. government shutdowns delaying ETF reviews and short-term price dips to $2.80–$2.90.

In the Ripple/XRP vs. SWIFT narrative, XRP dominates sentiment as a disruptive force, offering 3–5 second settlements and $0.0002 fees compared to SWIFT’s 1–5 day delays and $25–$100 fees.

Ripple’s ODL processed $2.3 billion in Q1 2025, with predictions of capturing 14% of SWIFT’s $150T market in five years.

While SWIFT tests blockchain, it’s seen as lagging, with X users calling it a “lipstick on a pig.”

XRP’s interoperability and DeFi utility solidify its edge, despite SWIFT’s broader current adoption (11,000+ institutions).

Grok’s response.

The community overwhelmingly favors XRP for revolutionizing cross-border payments.

The Role of ISO 20022 in Cross-Border Payments

A key factor shaping the competition between SWIFT, Ripple, and other payment networks is the global migration to ISO 20022, the new messaging standard for financial transactions.

ISO 20022 is designed to replace legacy MT messages with richer, structured data formats. By 2025, most major payment systems, including SWIFT, Fedwire in the U.S., TARGET2 in Europe, and many central banks, are transitioning to ISO 20022.

🚨 November 2025 = FINAL ISO 20022 deadline.

No more delays. Every major bank will be forced onto new rails… and $XRP was built for this exact standard.

This isn’t speculation. It’s documented. The bridge is ready. The flows are coming.

Data richness: ISO 20022 allows much more information to travel with each payment (such as remittance details, compliance checks, and sanctions data). This helps reduce errors and manual interventions.

Regulatory alignment: Regulators and central banks favor ISO 20022 because it improves transparency, traceability, and anti-money laundering (AML) monitoring.

Interoperability: As more national payment systems adopt ISO 20022, cross-border messaging becomes smoother, creating a common language for global payments.

SWIFT and ISO 20022

SWIFT is leading the ISO 20022 migration for global banks. Its new “Cross-Border Payments and Reporting Plus (CBPR+)” program requires all members to migrate messaging to the new format by 2025–26.

This strengthens SWIFT’s role as the trusted standards-setter for international banking.

Ripple and ISO 20022

XRP as a digital asset is not ISO 20022–compliant, but RippleNet’s payment network (On-Demand Liquidity Service) is designed to meet the standard. In May 2020, Ripple became the first blockchain firm to join the ISO 20022 Standards Body. RippleNet’s full compliance with the standard allows banks and financial institutions to connect through a single API, making adoption easier.

This compatibility is crucial if Ripple wants its blockchain-based network to interoperate with banks and central banks using ISO 20022.

XRP did not prioritize ISO20022. | Credit: @HammerToe (Dev at Ripple) on X

However, ISO 20022 doesn’t guarantee success for any single network, but it does raise the bar. Banks expect every payment solution, whether traditional (SWIFT) or crypto-native (Ripple, Stellar, Algorand), to be ISO 20022-compliant.

Ripple’s compliance gives it a seat at the table, but SWIFT benefits more because it is already embedded as the de facto messaging hub for global finance.

SWIFT’s blockchain project is an evolutionary update for its massive network. It will take years to mature and isn’t designed to replace Ripple tomorrow.

Ripple’s urgent hurdles lie elsewhere:

Regulatory uncertainty that still clouds XRP and RLUSD.

Banking and blockchain rivals (Stellar, Hedera, Algorand, Quant) with compelling models.

Banking relationships that are fragile and slow to scale.

A skeptical public and cautious institutional market post-FTX.

Ripple’s fight isn’t against SWIFT alone, it’s against an entire ecosystem of competitors, regulators, and perceptions.

To sum up: “If Ripple loses, it won’t be because of SWIFT’s blockchain move. It will be because Ripple couldn’t outcompete, out-regulate, or out-trust its peers.”

SWIFT announced a pilot/initiative to build a blockchain-based “shared ledger” for tokenized payments (stablecoins, tokenized deposits, CBDCs) in partnership with ConsenSys’ Linea, aiming for 24/7 real-time settlement capabilities layered on top of its existing messaging network.

Is SWIFT replacing its current system?

No. SWIFT is layering blockchain functionality on top of its existing messaging backbone, not discarding the legacy system. The goal is to add tokenized settlement capabilities while preserving SWIFT’s role as the trusted global messaging network.

Does SWIFT’s move threaten Ripple today?

Not immediately. SWIFT’s effort is a long-term, bank-centric modernization that leverages massive scale and existing trust. Ripple’s XRP Ledger and On-Demand Liquidity (ODL) offer different values like direct crypto-native settlement and a live payment rail, so SWIFT is not an instant “XRP killer.”

How do Ripple’s technical and business models differ from SWIFT’s plan?

Ripple provides an integrated messaging and settlement stack (RippleNet + XRP Ledger) and uses XRP as a bridge (ODL) to settle cross-currency flows quickly. SWIFT intends to keep messaging centralized in its ecosystem and add settlement rails via tokenization, but it’s starting from a different, bank-centric technical approach (Linea chosen as L2 in reported pilots).

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy