Circle Could Lose 10% of Revenue Overnight – Here’s Who’s Challenging Its Dominance

Share

Key Takeaways

Hyperliquid’s USDH could reshape stablecoin use by introducing yield in DeFi.

Circle is countering with native USDC integration inside the Hyperliquid ecosystem.

FalconX’s custody support aims to give USDH credibility with institutional investors.

A low-rate environment makes Circle’s reliance on Treasury income a growing weakness.

In the second quarter of 2025, Circle finally crossed a milestone with its long-awaited initial public offering (IPO). The outlook was bright, yet the real test was about to begin.

The company raised $1.2 billion by selling 19.9 million shares at $31 each, securing $583 million in net proceeds. USDC supply surged 90% year-over-year to $61.3 billion, and revenue and reserve income rose 53% to $658 million. Its adjusted Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA) climbed 52% to $126 million.

Yet the momentum was clouded by a $482 million net loss tied to stock-based compensation and debt revaluation, and a 9% stock drop exposed investor unease over Circle’s reliance on interest income from U.S. Treasuries.

That fragility now converges on Hyperliquid, where a yield-bearing USDH targets the same flows that sustain USDC.

Circle’s IPO success and USDC’s rapid growth now clash with three looming threats:

Rate cuts that could erase hundreds of millions in revenue

Rivals like Tether, J.P. Morgan, and Mastercard moving in, and

This article explains how Circle could lose up to 10% of its revenue overnight.

Circle’s IPO Success Meets Three Major Stablecoin Market Challenges

Circle’s IPO win placed it at the center of attention, but the reality is even more complex. The company now faces three challenges that together could reshape its position in the stablecoin market.

New Trending Crypto Wallet Offers

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Interest rate cuts are expected to shrink the returns Circle earns on its reserves, which generate almost all of its revenue. Those reserves, mostly short-term U.S. Treasuries, generate almost all its revenue.

Circle relies on interest from USDC reserves. In 2024 that income reached close to $1.7 billion, with 99% coming from Treasuries, according to Circle’s Q2 2025 report.

The model works when rates are high. It becomes fragile when rates fall. Less revenue means less room to fund integrations and incentives on venues like Hyperliquid. Traders shape what wins there through usage and liquidity, not governance.

If Circle tries to protect margins by passing costs along, USDC users on Hyperliquid could face higher costs or weaker rewards.

On the contrary, USDH may counter with governance-driven fee adjustments that pull activity toward its pairs, eroding USDC’s share over time.

2. Competitive Pressure: Tether, J.P. Morgan and Mastercard Challenge Circle’s Position

Tether continues to dominate with nearly 60% market share and has introduced Plasma, a zero-fee blockchain designed to handle USDT transfers without relying on Ethereum or Tron. By controlling its own rails, Tether removes user transaction fees and captures more value within its ecosystem.

Mastercard has taken a different route by integrating stablecoins such as USDC into its merchant network. This move keeps global payment flows tied to Mastercard’s infrastructure, ensuring it benefits from the rise of digital dollars rather than being bypassed.

Together, these strategies show how Circle faces pressure from multiple directions: a crypto-native rival locking down its dominance, a bank offering a regulated deposit token, and a global payments company reinforcing its control over merchant rails.

3. Disruptive Challengers

New projects are entering the market with yield-bearing stablecoins. Hyperliquid’s proposed USDH passes returns back to users, something Circle cannot legally offer under U.S. regulations.

Circle’s Q2 2025 results highlight this tension. The numbers show a business that is growing quickly but remains tied to a single revenue model that works only in a high-interest-rate environment.

How Hyperliquid’s Yield-Bearing USDH Threatens Circle’s USDC Model

The most immediate and disruptive challenge to Circle’s dominance is unfolding inside Hyperliquid, a decentralized perpetuals exchange that now commands about 79% of derivatives trading volume among its peers.

Hyperliquid is releasing a native stablecoin, USDH, and this one it is designed to be yield-bearing. This feature is the primary catalyst for the competition and a direct challenge to Circle’s model, which cannot offer yield directly to holders.

Competing Proposals for USDH

The issuer’s choice has become a proxy war for the future of decentralized finance (DeFi) liquidity. Two main proposals stand out:

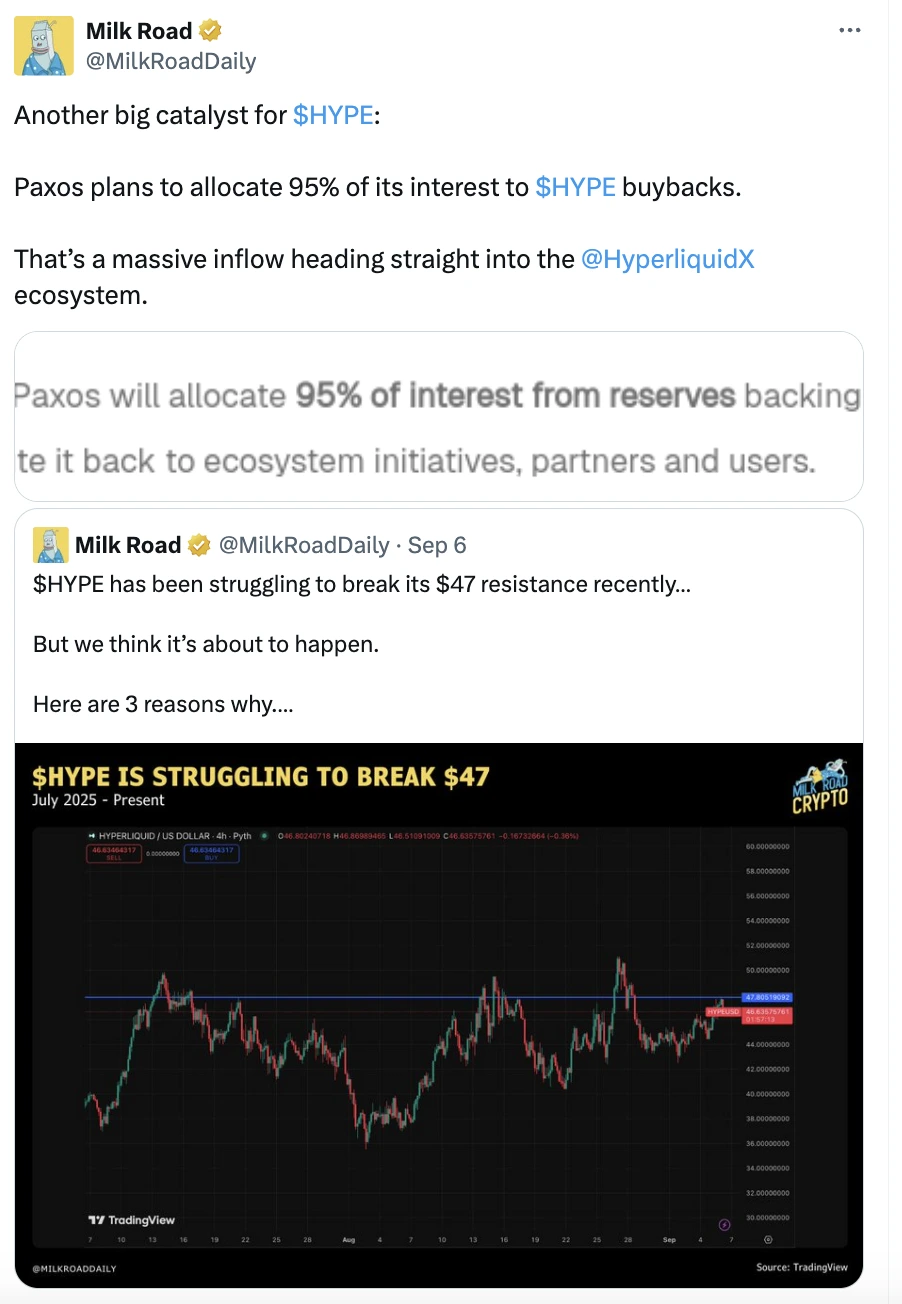

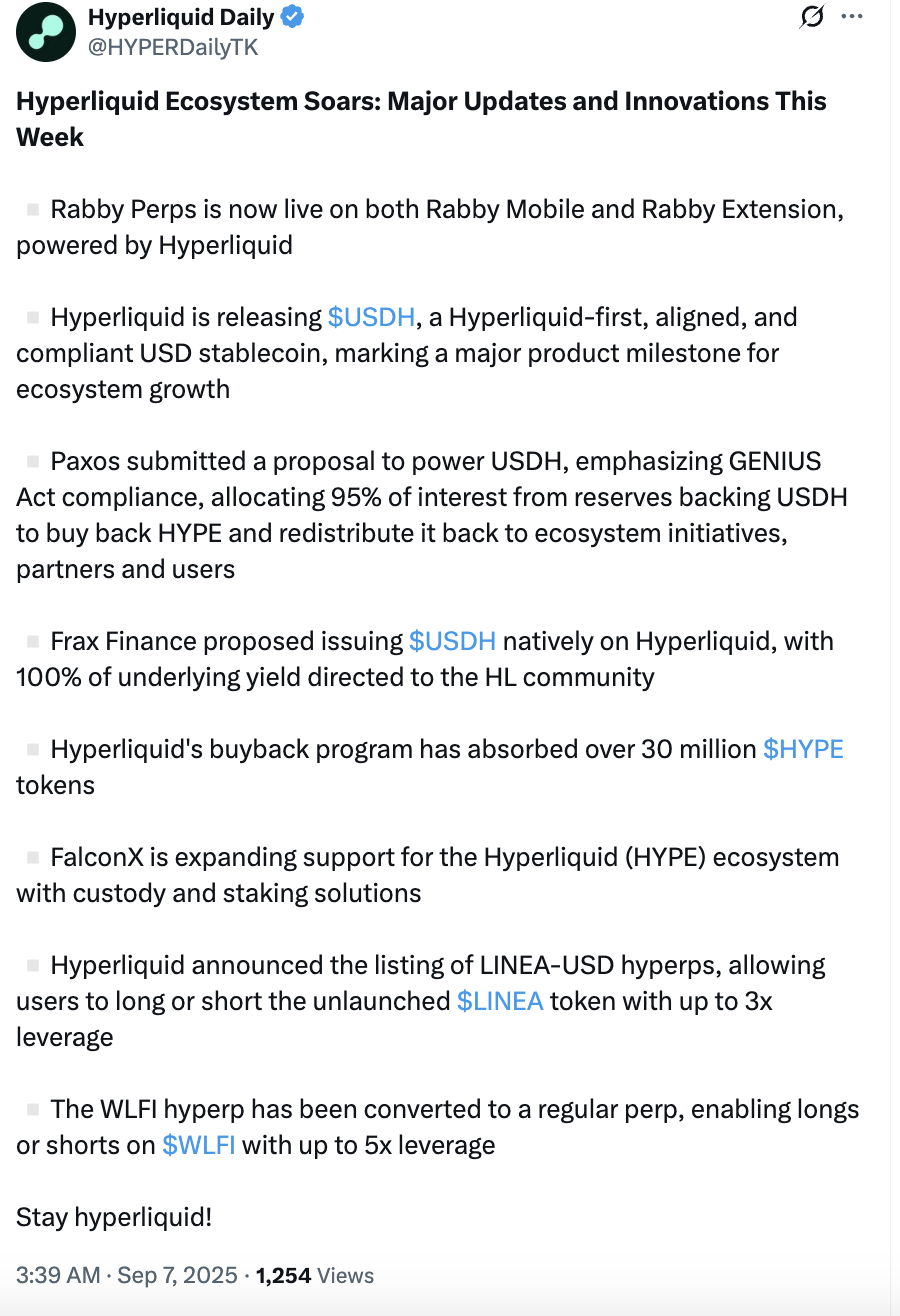

Paxos has offered a structure where 95% of income from reserves is redistributed through HYPE token buybacks, returning most of the benefit to users.

Frax Finance proposes backing USDH with its own yield-bearing frxUSD and sending 100% of the yield directly to Hyperliquid users.

In its latest bid, Agora has teamed up with industry partners, pledging to allocate all net revenue back into the coalition. Under the plan, its USDH stablecoin would run on Agora’s institutional infrastructure, with Rain providing global card and fiat gateways, and LayerZero enabling seamless cross-chain connectivity.

The Bidding War for $USDH. | Source: @eli5_defi on X

These competing visions show how USDH could either recycle value back into its ecosystem or hand it straight to holders. The decision will shape how attractive the token becomes in practice.

The Buyback Program

At the same time, Hyperliquid’s buyback program has already absorbed more than 30 million HYPE tokens.

Frax Finance proposes backing USDH with its own yield-bearing frxUSD and sending 100% of the yield directly to Hyperliquid users.

These competing visions show how USDH could either recycle value back into its ecosystem or hand it straight to holders. The decision will shape how attractive the token becomes in practice.

The Buyback Program

At the same time, Hyperliquid’s buyback program has already absorbed more than 30 million HYPE tokens.

This aggressive mechanism tightens supply, boosts token value, and signals that Hyperliquid is committed to returning revenue to its ecosystem rather than external shareholders.

By absorbing large amounts of HYPE, Hyperliquid strengthens the incentive loop around USDH, making the stablecoin more attractive to traders seeking yield plus governance exposure.

Institutional Validation Through FalconX

FalconX, a major crypto trading and custody platform serving institutional investors, has expanded support for the HYPE ecosystem with custody and staking services.

Why does it matter?

This provides trusted, regulated infrastructure for funds, hedge firms, and corporate treasuries that want exposure but require institutional-grade safeguards.

It is important because of institutional validation. If firms can safely hold and stake HYPE assets, USDH has a path to legitimacy beyond retail DeFi users.

But that’s a direct challenge to Circle, which built its narrative around being the most “compliant” stablecoin.

New Perpetual Markets

Additionally, Hyperliquid has rolled out new perpetual markets like LINEA-USD and WLFI, expanding the platform’s breadth and deepening its liquidity pools.

Why does it matter?

The expansion of markets like LINEA-USD and WLFI keeps liquidity anchored in Hyperliquid, setting the stage for USDH to become the preferred stablecoin on the platform.

More trading pairs mean more capital locked into Hyperliquid, giving USDH a ready-made marketplace.

This could be challenging for Circle: USDC could get sidelined if traders default to a native, yield-paying option tied to the platform’s growth.

Why Is USDH Different?

Under the U.S. GENIUS Act, stablecoin issuers are prohibited from paying interest directly to holders. This makes USDH fundamentally different from Circle’s USDC.

That legal boundary means Circle cannot compete on yield, even as U.S. Treasury returns shrink in a lower-rate environment.

If USDH succeeds, it could pull significant liquidity away from USDC, especially in DeFi markets where yield is the main attraction. This could weaken Circle’s role.

Thus, for Hyperliquid’s USDH to offer yield legally, it would likely need to fall outside of being treated as a “payment stablecoin” under GENIUS, or emerge via a regulatory loophole (e.g., via third-party “rewards” structuring).

MiCA effectively bans interest-bearing stablecoins by requiring 1:1 reserves, which prohibits the issuance of stablecoins that look like bank deposits, and also bans algorithmic stablecoins due to lack of reserves. While MiCA doesn’t use the term “ban” for stablecoin yield directly, the regulations’ aim to protect bank functions and prevent them from becoming too similar to banking products makes the issuance of yield-bearing stablecoins incompatible with the framework.

Also, for the U.S. market, MiCA compliance doesn’t override the GENIUS Act’s restrictions. Even if USDH were MiCA-compliant, it would still risk violating U.S. law if it provides yield to U.S. holders.

How Circle Plans to Defend USDC Inside Hyperliquid Against USDH

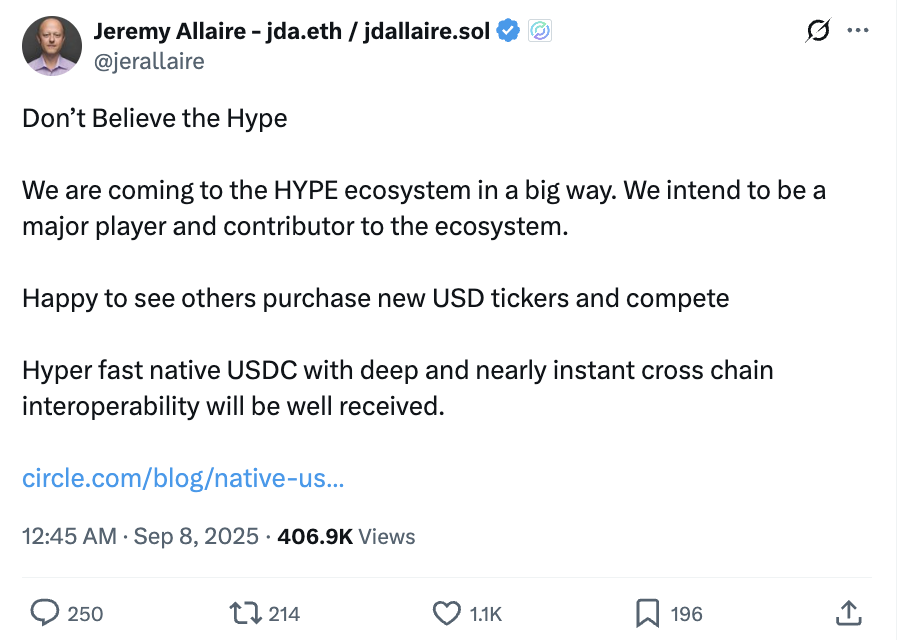

Rather than sidestep the competition, Circle is moving directly into Hyperliquid to defend its position.

According to Jeremy Allaire (co-founder and CEO of Circle), the company is preparing to launch a native USDC within the HYPE ecosystem, aiming to secure its role where USDH is poised to dominate.

This turns the contest into a head-to-head clash inside the same platform:

USDH is appealing with yield, user incentives, and new governance.

USDC appeals with scale, liquidity, regulatory trust, and interoperability.

The future of on-chain dollars may depend on which model users prefer. The outcome will reveal whether scale and regulatory approval can outweigh the pull of direct financial incentives in the evolving stablecoin market.

Circle’s IPO success gave the company momentum, but its reliance on Treasury yields makes it fragile in a shifting market. Hyperliquid’s plan to launch USDH, a stablecoin that pays yield, highlights this vulnerability like no rival before.

Inside Hyperliquid, the contest is already set. Paxos and Frax Finance are competing to shape USDH, FalconX provides custody for institutions, and new trading markets reinforce demand. Circle’s answer is to launch native USDC inside the same ecosystem, turning the clash into a direct test of yield versus trust, and liquidity versus regulation.

The broader picture adds more pressure. Tether, J.P. Morgan, and Mastercard are advancing their models, while falling U.S. interest rates threaten Circle’s core income. Still, the sharpest test will come from Hyperliquid. If USDH succeeds, Circle must prove that scale and compliance can outweigh yield attraction in DeFi.

FAQs

How does Hyperliquid’s validator governance affect traders?

It allows traders to influence stablecoin design, giving them a stake in decisions that shape USDH.

Could USDH adoption change trading fees on Hyperliquid?

Yes. If USDH becomes dominant, fee structures may be adjusted to favor its use across markets.

What risks does Circle face if it embeds USDC too deeply in Hyperliquid?

Dependence on one exchange could expose USDC to governance changes outside Circle’s control.

How might U.S. regulators view Hyperliquid’s yield-bearing design?

U.S. regulators may scrutinize Hyperliquid’s yield-bearing design, especially its stablecoin yield and staking, for potential securities violations and AML/KYC non-compliance. The GENIUS Act clarifies yield-bearing stablecoins, but Hyperliquid’s lack of KYC could trigger stricter oversight, risking its competitive advantage.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy