Home / Education / Crypto / Investing / Ripple’s $50B Buyback Revives the ‘SWIFT Killer’ Narrative in Global Payments: What this Means for XRP Investors

Why SWIFT's Blockchain Push Is a Win for Ripple but Not Yet for XRP

Share

Key Takeaways

Ripple’s $750M share buyback implies a $50 billion valuation, a 25% increase from its $40B valuation in November, signaling strong investor confidence.

The buyback suggests institutional investors increasingly view Ripple as financial infrastructure, not just a crypto company tied to XRP’s market price.

RLUSD, Ripple’s U.S. dollar stablecoin, has already reached about $1.5 billion in market cap, adding liquidity to the XRP Ledger.

XRP’s role as a bridge asset for cross-border payments through On-Demand Liquidity (ODL) is designed to reduce reliance on traditional banking accounts.

Ripple is once again commanding the attention of global finance. The blockchain company closely associated with the XRP Ledger has launched a $750 million share buyback program, a move that implies a company valuation of roughly $50 billion.

The buyback follows a $500 million funding round in November that valued the firm at $40 billion, meaning investors are now placing a 25% higher value on Ripple in just a few months, even amid a volatile crypto market.

For many observers, the announcement does more than signal confidence in Ripple’s balance sheet. It has reignited a narrative that has followed the company for more than a decade: the idea that Ripple, and, by extension, XRP, could become a modern alternative to SWIFT, the decades-old global payments network used by banks worldwide.

But what exactly does this buyback mean for Ripple’s strategy, the XRP ecosystem, and investors trying to understand the future of global payments?

To answer that, we need to examine Ripple’s infrastructure, its regulatory battle, its recent expansion into financial services, and the evolving role of XRP as a liquidity bridge in international finance.

Ripple’s $50B Valuation and $750M Share Buyback: Why It Matters

Share buybacks are typically used by companies to signal that leadership believes the business is undervalued or entering a strong growth phase. Ripple’s tender offer allows the company to repurchase shares from early investors and employees, providing liquidity while consolidating ownership.

The $750 million buyback program is particularly notable given recent market conditions. Over the same period since Ripple’s November fundraising round, Bitcoin and XRP both experienced price declines of roughly 30-40%, reflecting broader market volatility.

Ripple has initiated a $750 million share buyback program from early investors. | Credit: RippleXity X profile

This suggests that institutional investors may be evaluating Ripple less as a speculative crypto company and more as financial infrastructure for the next generation of payments.

The buyback also comes at a time when Ripple has been aggressively expanding its business through acquisitions and new product launches.

Ripple’s Expanding Crypto and Financial Infrastructure Ecosystem

Ripple is no longer simply a blockchain payments startup. Over the past few years, it has moved toward becoming a full-stack digital finance infrastructure provider.

Recent strategic developments include:

Hidden Road acquisition ($1.25 billion): A prime brokerage clearing trillions in institutional trades annually.

The RLUSD stablecoin alone has already grown to around $1.5 billion in market value, adding another layer of liquidity to Ripple’s ecosystem.

Together, these moves indicate a strategy of vertical integration across trading, custody, settlement, and liquidity infrastructure.

Rather than relying solely on XRP adoption, Ripple is building an ecosystem that supports tokenized assets, stablecoins, institutional trading, and cross-border settlement.

This infrastructure-first approach could be key to understanding why institutional investors are increasingly comfortable valuing the company in the tens of billions.

What Is the XRP Ledger and How Does It Work for Global Payments?

At the center of Ripple’s ecosystem is the XRP Ledger (XRPL), a blockchain network launched in 2012.

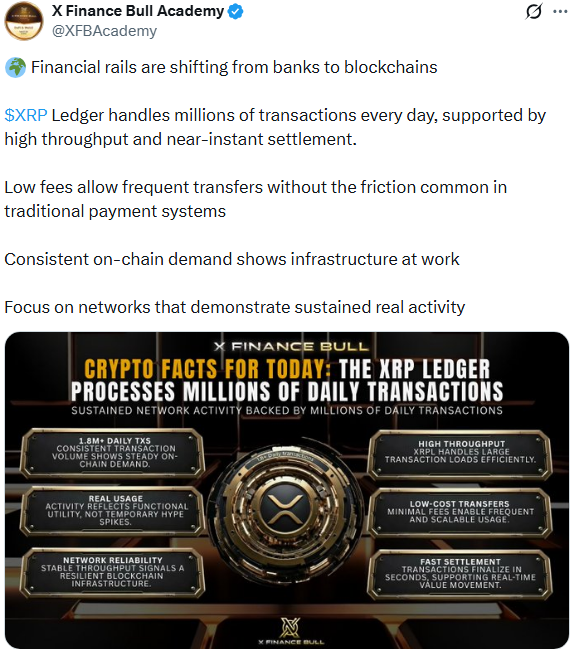

XRP Ledger handles millions of transactions every day, supported by high throughput and near-instant settlement. | Credit: X Finance Bull Academy X profile

The ledger’s architecture was designed specifically for high-volume financial settlement, not simply peer-to-peer transfers.

Ripple’s core product uses XRP as a bridge asset, allowing banks and financial institutions to move funds between currencies without holding large pools of capital in foreign accounts.

This model, called On-Demand Liquidity (ODL), could potentially reduce the need for the nostro/vostro account system that underpins traditional cross-border banking.

Why XRP Is Often Called a “SWIFT Killer” in Cross-Border Payments

The SWIFT network currently handles trillions of dollars in global financial messaging every day. However, SWIFT does not settle transactions itself. Instead, it sends payment instructions between banks, which then settle funds through correspondent banking networks.

This process can take hours or even days, particularly across different jurisdictions.

Ripple’s model aims to reduce that friction by enabling near-instant settlement using digital liquidity.

Instead of holding pre-funded accounts in multiple countries, institutions can convert local currency to XRP, transfer it across the ledger, and convert it into the destination currency.

In theory, the process could complete in seconds rather than days.

Because of this potential efficiency gain, XRP has often been described as a “SWIFT alternative” or “SWIFT killer.”

Whether it ultimately reaches that scale remains uncertain, but the narrative continues to resurface whenever Ripple expands its infrastructure or secures new institutional partnerships.

SEC vs Ripple: How the Legal Battle Shaped XRP’s Future

Ripple’s journey to institutional credibility was not straightforward.

In December 2020, the U.S. Securities and Exchange Commission filed a lawsuit against Ripple Labs, alleging that the company had conducted $1.3 billion in unregistered securities sales through XRP.

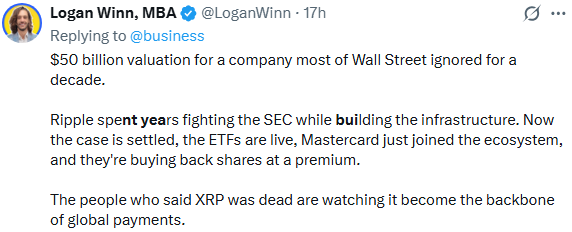

Ripple spent years fighting the SEC while building the infrastructure. Now the case is settled. | Credit: Logan Winn X profile

The token price collapsed from roughly $0.60 to below $0.20.

The legal battle lasted nearly five years and became one of the most closely watched cases in crypto regulation.

A major turning point came in July 2023, when a federal judge ruled that programmatic XRP sales on exchanges did not constitute securities transactions, though certain institutional sales did.

ETFs made XRP exposure accessible to traditional investors without direct crypto custody, opening the asset to pension funds, hedge funds, and institutional portfolios.

At the same time, Ripple continued expanding RippleNet, its network connecting financial institutions for cross-border payments.

Today the ecosystem reportedly includes over 300 financial institutions globally.

Ripple’s Strategy to Build Global Blockchain Payment Infrastructure

Ripple’s long-term strategy appears focused on building a global settlement infrastructure rather than a speculative cryptocurrency ecosystem.

Several factors support this approach.

1. Liquidity Bridge Model

XRP functions as an intermediary asset between fiat currencies, allowing funds to move without the need for multiple banking relationships.

2. Speed and Cost Efficiency

Settlement in seconds and near-zero transaction fees offer a clear operational advantage over traditional correspondent banking.

3. Infrastructure Depth

Ripple now operates across custody, stablecoins, institutional trading, and liquidity provisioning.

4. Network Effects

The more payment corridors use XRP liquidity, the deeper markets become and the more efficient transactions get.

This creates a feedback loop that could strengthen adoption over time.

Key Risks XRP Investors Should Still Consider

Despite the growing optimism surrounding Ripple and XRP, significant risks remain.

While a large portion of XRP supply was placed into escrow for predictable releases, concentration concerns persist.

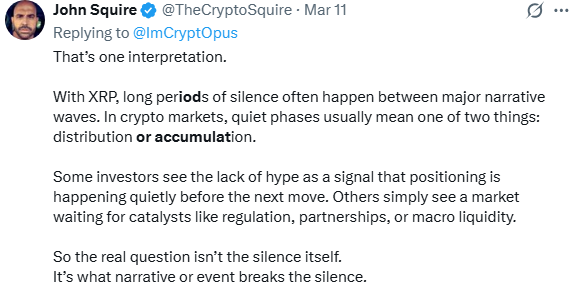

With XRP, quiet phases usually mean one of two things: distribution or accumulation. | Credit: John Squire X profile

Competition From Stablecoins

Stablecoin-based settlement models. especially those backed by major financial institutions, could compete with XRP’s role as a liquidity bridge.

Regulatory Uncertainty

Although Ripple’s SEC case has ended, global crypto regulation continues evolving, and new rules could impact digital asset adoption.

Market Volatility

XRP, like other crypto assets, remains subject to price swings that may deter risk-averse financial institutions.

What Ripple’s $750M Buyback Means for XRP Investors

Ripple’s $750 million buyback is not directly tied to the price of XRP. However, it does send several signals to the market.

First, it suggests that Ripple leadership believes the company’s long-term growth prospects are strong.

Second, it reflects growing institutional confidence in Ripple’s infrastructure strategy.

Third, it reinforces the narrative that XRP may play a role in the future architecture of global payments.

For investors, the key takeaway is that Ripple’s evolution is increasingly infrastructure-driven rather than token-driven.

XRP’s long-term value proposition depends less on speculative cycles and more on whether the XRP Ledger becomes an integral component of global liquidity rails.

How Blockchain Is Transforming Global Payments Infrastructure

The global payments industry is undergoing a structural transformation. Traditional systems built decades ago are now facing competition from:

Ripple is positioning itself at the intersection of these trends.

Its goal is not necessarily to replace existing systems overnight but to provide faster, cheaper settlement rails that integrate with existing financial institutions.

Ripple and XRP Future in the Global Payments Market

Ripple’s $50 billion valuation and $750 million buyback highlight how dramatically the company’s position has changed since its early years.

After surviving a prolonged regulatory battle and expanding into institutional infrastructure, Ripple is now attempting to build a global financial network around the XRP Ledger.

Whether XRP ultimately becomes a dominant bridge asset remains uncertain.

But the structural elements are increasingly visible:

Regulatory clarity

Institutional investment

Expanding financial infrastructure

Growing liquidity networks

For XRP investors, the story is evolving from speculative hype to long-term infrastructure adoption.

The real question is no longer whether Ripple can survive.

It is whether the company, and the XRP Ledger, can capture a meaningful share of the multi-trillion-dollar global payments market.

What does Ripple’s $750 million share buyback mean?

Ripple’s $750 million share buyback allows the company to repurchase shares from early investors and employees through a tender offer. The move implies a company valuation of about $50 billion, signaling strong investor confidence in Ripple’s long-term growth and its role in building blockchain-based financial infrastructure.

Does Ripple’s buyback affect the price of XRP?

Not directly. Ripple’s buyback involves company shares, not the XRP cryptocurrency. However, the move may indirectly influence market sentiment by signaling financial strength and institutional confidence in Ripple’s ecosystem.

Why is XRP often called a “SWIFT killer”?

XRP is sometimes described as a “SWIFT killer” because the XRP Ledger enables near-instant cross-border settlement, potentially replacing slow and expensive correspondent banking processes. While SWIFT handles messaging between banks, XRP could act as a liquidity bridge for real-time settlement.

What is the XRP Ledger (XRPL)?

The XRP Ledger is a blockchain launched in 2012 designed for fast and low-cost financial transactions. It uses the Ripple Protocol Consensus Algorithm (RPCA), enabling settlement in about 3–5 seconds, processing over 1,500 transactions per second, with transaction fees that are fractions of a cent.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy