5 Key Partners Strengthening Ripple Treasury’s Ecosystem — Including SWIFT

Share

Key Takeaways

The traditional SWIFT Nostro/Vostro model depends on pre-funded bank accounts and intermediary messaging.

Ripple’s On-Demand Liquidity (ODL) leverages blockchain and digital assets for real-time settlement.

SWIFT facilitates communication between over 11,000 financial institutions but still relies on correspondent banks and pre-funded Nostro accounts.

RippleNet continues to attract banks by utilizing its software layer, even without direct XRP usage.

Global payments are the arteries of the financial world, carrying trillions of dollars across borders each day.

Yet, beneath this seamless flow lies an intricate network of intermediaries, messaging systems, and liquidity accounts that determine how quickly and efficiently money moves.

Two systems now represent opposite ends of that spectrum: SWIFT’s Nostro/Vostro model, the backbone of traditional finance, and Ripple’s On-Demand Liquidity (ODL), a blockchain-powered alternative promising near-instant settlement without pre-funded accounts.

This article examines how each system operates, their key differences, and the implications of the rise of digital liquidity for the future of international payments.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) was established in 1973 to standardize financial messaging between banks.

Before SWIFT, payments were processed through telex messages, a slow and error-prone method. SWIFT created a unified, secure network that allowed banks to send payment instructions electronically, a messaging system, not a settlement system.

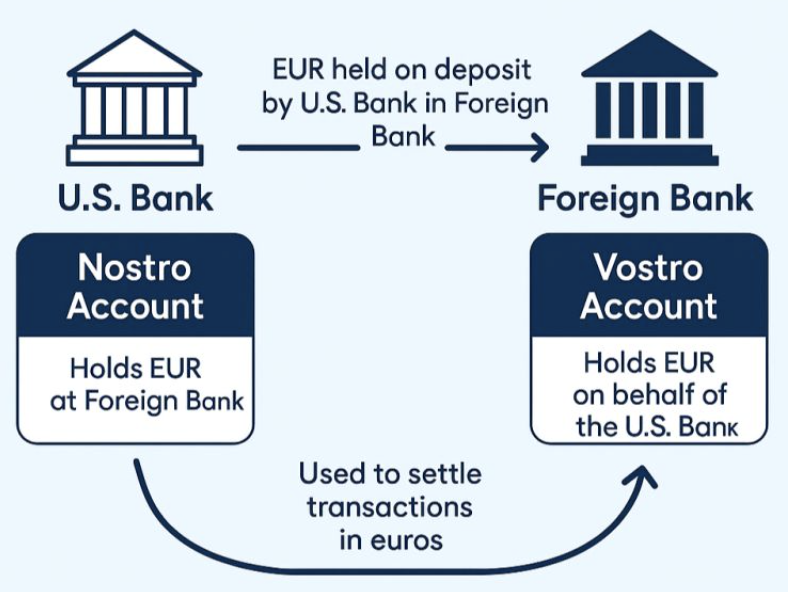

At the core of SWIFT-based settlement lies a mechanism called the Nostro/Vostro account system, which is derived from Latin terms meaning “ours” and “yours.”

Here’s how it functions in practice:

A bank in one country (Bank A) maintains a Nostro account in a foreign currency with a correspondent bank abroad (Bank B).

From Bank B’s perspective, that same account is a Vostro account, an account it holds “for you.”

These accounts allow banks to settle payments in foreign currencies without a direct local presence.

However, they require pre-funded liquidity, meaning large sums of money must sit idle in accounts around the world to facilitate settlements.

An Example

Imagine a customer at Bank A in Singapore wants to send $1 million USD to a supplier at Bank B in the U.S.

Bank A sends a SWIFT message to Bank B, instructing it to debit Bank A’s Nostro account in USD.

The payment is then credited to the supplier’s account in the U.S.

The settlement relies on Bank A’s pre-funded USD balance sitting in the U.S.

While reliable, this system involves multiple intermediaries and time lags:

Funds move through correspondent banks, adding layers of processing.

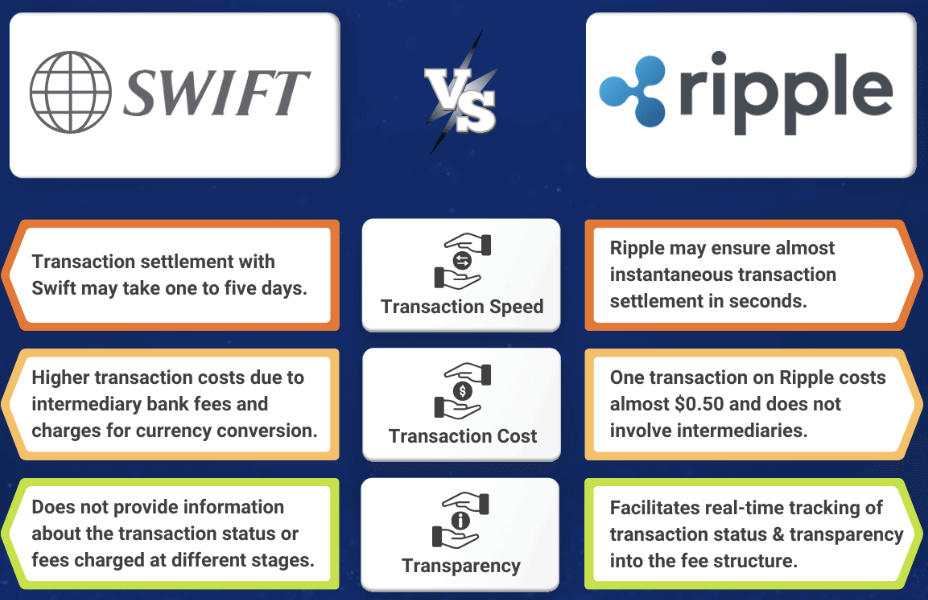

Settlement can take two to five business days, depending on the jurisdiction and time zone.

Costs accumulate like fees, FX spreads, and reconciliation processes.

The result is a system built on trust and relationships, but one that struggles with speed, transparency, and liquidity efficiency.

SWIFT GPI and SwiftNet Instant: Do They Enable Faster Cross-Border Payments?

To address long-standing criticism around slow and opaque cross-border transactions, SWIFT introduced Global Payments Innovation (GPI) in 2017 and later SwiftNet Instant, both designed to modernize and accelerate international payments.

SWIFT GPI enhances the traditional correspondent-banking system by adding real-time tracking, end-to-end transparency, and same-day settlement for many corridors. More than 4,000 financial institutions use it, enabling customers to see when funds are credited and what fees are deducted.

SwiftNet Instant goes a step further by linking domestic instant-payment networks using the ISO 20022 standard, allowing transfers to settle in seconds in select regions.

However, both systems still rely on the correspondent-banking model, meaning liquidity must often be pre-funded in destination currencies and settlement can vary by region and time zone.

True instant payments are limited to corridors where all participating banks support the same real-time systems. Costs remain relatively high due to multiple intermediaries, and smaller banks may still face delays caused by compliance or processing bottlenecks.

In contrast, Ripple’s ODL offers a blockchain-based alternative that uses XRP as a bridge currency, converting fiat to XRP and back within seconds. This design eliminates the need for pre-funded accounts, reduces intermediaries, and enables near-instant, low-cost settlement 24/7.

Yet ODL faces its own limitations, such as regulatory uncertainty, limited adoption among major banks, and exposure to crypto-market volatility.

Features

SWIFT GPI / SwiftNet Instant

Ripple ODL

Underlying technology

Upgraded correspondent banking rail

XRPL + XRP

Settlement speed

Hours → days in many corridors

Seconds (in many corridors)

Liquidity funding model

Pre-funding of foreign currency accounts common

Uses XRP as bridge → reduces pre-funding

Cost and intermediaries

Moderate improvement over legacy

Large cost reductions claimed in certain corridors

Adoption breadth

Very broad – thousands of banks

Growing, but narrower bank/fintech network

Token/crypto exposure

None (fiat-based)

Requires use of crypto (XRP) in many cases

Ripple’s Modern Alternative: On-Demand Liquidity (ODL)

Ripple Labs, founded in 2012, aimed to modernize cross-border payments by utilizing blockchain infrastructure.

Its flagship product, RippleNet, connects financial institutions through a shared network that can transmit payment messages and settle value in seconds.

How Ripple’s ODL works. | Credit: Webopedia

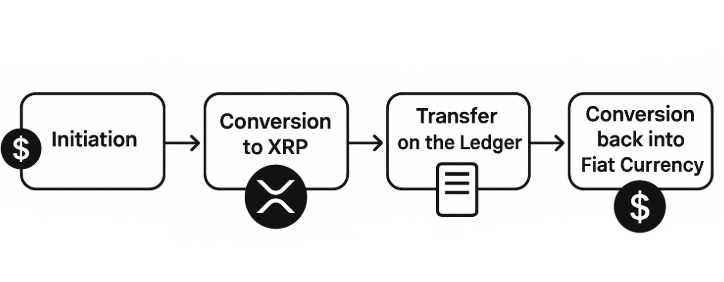

At the heart of this innovation is On-Demand Liquidity (ODL), a system that replaces pre-funded Nostro accounts with real-time liquidity sourced from XRP, Ripple’s native digital asset.

How ODL Works

ODL uses XRP as a bridge currency between two fiat currencies, enabling instant foreign exchange and settlement.

Here’s the flow in simple steps:

Bank A wants to send a payment from the U.S. to Mexico.

Bank A converts USD into XRP through a crypto exchange in the U.S.

XRP is sent across the XRP Ledger, typically in seconds.

At the receiving end, XRP is instantly converted into Mexican pesos (MXN) through another local exchange.

The recipient receives MXN in their local account, and the settlement is completed.

This process eliminates the need for pre-funded accounts in foreign countries. Liquidity is “borrowed” for seconds instead of being tied up for days.

Benefits of Ripple’s ODL

Speed: Transactions on the XRP Ledger settle in 3-5 seconds.

Cost efficiency: No idle capital or multi-bank fees.

Transparency: Each transfer is recorded on an immutable ledger visible to participants.

Capital optimization: Firms can deploy working capital elsewhere instead of holding it in dormant Nostro accounts.

Ripple reports that ODL users have seen cost savings of up to 60.70% compared to SWIFT-based corridors, particularly in emerging markets where FX spreads are wide.

This locked capital could otherwise be used for lending, investment, or market-making.

Ripple’s ODL addresses that inefficiency by freeing up liquidity; banks can settle only when needed, reducing balance sheet strain.

Cost and Speed

SWIFT: Multiple hops, reconciliation costs, and time delays.

ODL: Single atomic transaction across chains, with automatic FX conversion.

In practical terms, what takes 2-3 days via SWIFT can be completed under a minute via ODL, often at a fraction of the cost.

Transparency and Traceability

Traditional SWIFT payments rely on intermediaries for confirmation, often leaving counterparties uncertain about settlement times or fees.

ODL’s transactions are recorded on a public ledger (XRP Ledger), where participants can verify the transaction status in real-time.

Regulatory and Compliance Factors

SWIFT operates within existing banking laws and established AML/KYC frameworks.

Ripple ODL operates through licensed exchanges and regulated payment providers; however, adoption depends on local cryptocurrency regulations.

Many financial institutions use RippleNet without XRP exposure, leveraging only its messaging and settlement infrastructure, a similar approach to how SWIFT is utilized today.

SWIFT’s Strategic Move to Linea

SWIFT has announced a major step forward by trialing with Linea, ConsenSys’s Ethereum layer-2 zkEVM network, marking a significant milestone in the evolution of cross-border payments. This collaboration aims to enhance speed, efficiency, and transparency across the global financial network.

By leveraging Linea’s zero-knowledge technology, SWIFT can enable near-instant settlements, 24/7 transaction availability, and reduced operational costs compared to traditional banking systems.

The move also supports SWIFT’s broader strategy to remain relevant in a blockchain-driven financial landscape, connecting banks, fintechs, and decentralized networks seamlessly. This pilot demonstrates SWIFT’s commitment to adopting next-generation blockchain infrastructure while maintaining security and compliance standards across its global network.

Real-World Adoption and Use Cases of SWIFT vs. Ripple’s ODL

SWIFT

SWIFT remains the dominant global standard, processing over 44 million messages per day. Its GPI (Global Payments Innovation) upgrade has improved tracking and speed, reducing settlement times to hours in some corridors.

However, even GPI relies on the same Nostro/Vostro model, which limits its ability to achieve real-time liquidity optimization.

Ripple ODL

Ripple has built corridors connecting dozens of markets, including the Philippines, Mexico, Brazil, and Japan.

Partners such as SBI Holdings, Tranglo, and Remitly have used ODL to power instant remittances.

According to researchers, transaction volumes through ODL increased ninefold between 2021 and 2023, reflecting growing institutional adoption, particularly in emerging markets where cross-border costs are highest.

Limitations of of SWIFT and Ripple’s ODL

However, both SWIFT and ODL come with some risks and limitations. Here are some:

For SWIFT:

Operational inefficiency: Relies on legacy rails.

Liquidity drag: Capital locked in Nostro accounts.

Transparency issues: Limited visibility between intermediaries.

For ODL:

Regulatory uncertainty: Use of XRP may face scrutiny in certain jurisdictions.

Market volatility: XRP’s price fluctuations could impact settlement costs, though transactions occur within seconds.

Exchange dependency: Liquidity relies on local exchange depth and compliance standards.

In essence, while ODL offers a blueprint for efficiency, its success ultimately depends on global regulatory harmonization and the integration of liquidity.

Beyond Competition: How SWIFT and Ripple Are Converging on the Same Goal

It’s not a zero-sum contest.

In reality, banks and payment firms are exploring hybrid architectures that blend traditional compliance frameworks with the efficiency of blockchain.

SWIFT’s own experiments with tokenized settlement (via its Connector Network) mirror Ripple’s approach, linking blockchain platforms to fiat rails.

RippleNet continues to attract traditional institutions that utilize the network’s messaging capabilities without directly involving XRP.

Both systems are evolving toward the same goal: instant, transparent, and interoperable payments.

Where SWIFT is layering innovation on top of legacy infrastructure, Ripple is building its foundation on blockchain.

Beyond Nostro/Vostro: The Evolution of Global Liquidity

At its core, the shift from Nostro/Vostro to On-Demand Liquidity reflects a more profound financial transformation: a move away from capital-heavy intermediation toward software-driven liquidity orchestration.

In the same way that the internet digitized information, blockchain is digitizing the movement of value.

The question is not whether this transition will happen, but how quickly traditional institutions can adapt.

SWIFT’s Nostro/Vostro model and Ripple’s On-Demand Liquidity represent two eras of global payments: one defined by trust and pre-funding, the other by speed and algorithmic liquidity.

While SWIFT remains indispensable to global finance, its reliance on pre-funded accounts makes it costly and slow in a digital-first economy.

Ripple’s ODL, by contrast, demonstrates how blockchain can streamline settlement, reduce costs, and unlock trapped capital; however, widespread adoption still hinges on regulation and the depth of liquidity.

In the long run, the most likely future isn’t one system replacing the other, but interoperability between traditional and blockchain infrastructures.

SWIFT brings trust; Ripple brings efficiency. Together, they may power the next evolution of cross-border payments, a world where money moves as quickly as information does today.

SWIFT, the Society for Worldwide Interbank Financial Telecommunication, is a global network that enables banks to send standardized payment messages securely. It doesn’t move money directly; instead, it acts as a messaging system that tells banks where to debit and credit accounts during cross-border transactions.

What is Ripple’s On-Demand Liquidity (ODL)?

Ripple’s ODL is a blockchain-based payment solution that enables near-instant cross-border settlements without requiring pre-funded Nostro accounts. It utilizes XRP, Ripple’s native digital asset, as a bridge currency between two fiat currencies, converting, transferring, and settling value in seconds.

Does every RippleNet transaction use XRP?

No. Many institutions use RippleNet, Ripple’s network infrastructure, without using XRP directly. RippleNet supports messaging and fiat settlement similar to SWIFT but faster and with better transparency. ODL is the XRP-enabled layer for institutions seeking real-time liquidity.

Why is “on-demand liquidity” important?

It frees capital. Instead of banks locking billions in dormant foreign accounts, they can access liquidity only when needed, for seconds at a time. This reduces working capital requirements, boosts efficiency, and improves profitability, especially for high-volume remittance or trade corridors.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy