10 Major US Banks Quietly Building Bitcoin Products

Share

Key Takeaways

Most big U.S. banks add Bitcoin in steps: ETFs first, then custody, then loans or trading. This helps them control risk while testing demand.

“Bitcoin access” at a bank often means a Bitcoin ETF, not owning real Bitcoin. That changes what you control and what you can do with it.

Custody is the hidden backbone of bank crypto products. The big question is always who holds the asset: the bank, a partner, or a sub-custodian.

Borrowing against Bitcoin or Bitcoin ETFs can be convenient, but it adds danger. If prices fall fast, banks can demand more collateral or force a sale.

US banks aren’t advertising Bitcoin as much as they do other financial products, such as savings accounts with a high annual percentage yield (APY). Instead, they’re rolling out Bitcoin products in a typical banking way: quiet pilot programs with limited client groups.

That rollup method is anything but random. They don’t want to offer risky assets without fleshing out the surrounding product. Instead, they want crypto to fit into existing products, both because it’s easier to deploy as well as for customers to understand.

That’s why you’ll see a pattern: exchange-traded funds (ETFs) first, then custody products, and finally, lending.

This article breaks down 10 major US banks or bank-like entities building Bitcoin products right now.

New Trending Crypto Wallet Offers

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Bitcoin ETFs: You buy shares of a company that holds Bitcoin for you. You don’t hold the Bitcoin yourself. Think of buying ETFs as a Bitcoin “wrapper” rather than buying raw Bitcoin. The product is easier for tax reporting and risk control.

Loans/Collateral: A company borrows cash using Bitcoin or Bitcoin ETF shares as a backup, or the bank allows trading Bitcoin within its platform.

Say a company holds $50,000 of a Bitcoin ETF. A bank might let the company borrow against it the way a trader might borrow against stocks. However, Bitcoin’s volatility can make this risky. If Bitcoin crashes, and the company holds a loan against it, the bank might demand more collateral to cover Bitcoin’s drop.

Of course, before you touch any bank-issued Bitcoin product, ask “who owns the asset,” “what are the fees for using a product,” and “can I easily move assets out of the product?”

Now for the Bitcoin products.

1. PNC: Bitcoin Trading Inside Private Banking

As of December 2025, PNC Bank is launching a spot Bitcoin trading service for its private banking clients, powered by Coinbase’s crypto-as-a-service infrastructure.

Source: @Divay_vir on Reddit

The goal is to offer crypto custody while allowing clients direct Bitcoin exposure through buying, holding, and selling at the same place they manage traditional investments, instead of signing up for a third-party exchange.

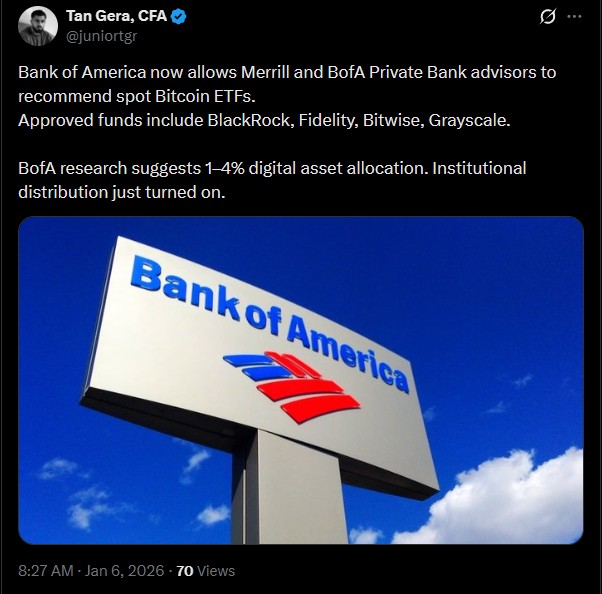

2. Bank of America: Advisors Recommend Spot Bitcoin ETFs

Starting January 5, 2026, financial advisors at Bank of America Private Bank, Merrill, and Merrill Edge can now recommend crypto exchange-traded products (ETPs) such as Bitcoin ETFs. Beforehand, advisors wouldn’t mention crypto unless a client brought it up.

Source: @juniortgr on X

At launch, Bank of America will choose from BlackRock, Grayscale, Bitwise, or Fidelity’s Bitcoin ETFs.

3. Morgan Stanley: ETF Filings and Crypto Trading

Morgan Stanley filed for a Morgan Stanley Bitcoin Trust and Solana Trust with the US Securities and Exchange Commission (SEC) in early January 2026. The goal, of course, is to offer ETFs on two of the world’s most popular cryptocurrencies.

Perhaps most interesting is Morgan Stanley’s bold approach to releasing two crypto products at once, rather than cautiously implementing one at a time.

Source: @Kylechasse on X

The entity also plans to add crypto trading on E*Trade in the first half of 2026 through a partnership with Zerohash, intending to offer Bitcoin, Ether, and Solana at launch. In-house crypto trading would pair well with Morgan Stanley’s potential crypto wallet, also set for launch in 2026.

Source: @BitcoinArchive on X

4. Goldman Sachs: Bitcoin ETFs on the Balance Sheet

Goldman Sachs invested over $600 million in spot Bitcoin exchange-traded funds in August 2024, but has yet to offer its own Bitcoin products.

However, the entity spent $2 billion on ETF issuer Innovator Capital in December 2025. This deal isn’t necessarily a Bitcoin product, but it shows that Goldman will invest in innovative ETF services, which is likely to lead toward crypto.

5. Citigroup: Crypto Custody Services

Citigroup has mentioned building a crypto custody service with plans to launch in 2026. It has been in development over the past few years, with plans to offer it to institutional clients. Citi has also discussed services related to crypto ETFs.

This includes potential roles in custody, fund administration, settlement support, and collateral management for ETF issuers and institutional investors gaining exposure to crypto through regulated market vehicles. As spot crypto ETFs expand beyond Bitcoin and Ethereum, demand for trusted custodians is expected to grow rapidly.

Citi’s move reflects a broader industry trend: traditional banks are not rushing into speculative trading but are instead focusing on infrastructure layers such as custody, clearing, and settlement. For the crypto market, this signals increasing institutional normalization—where digital assets are treated less as fringe instruments and more as financial assets requiring the same safeguards as equities, bonds, and commodities.

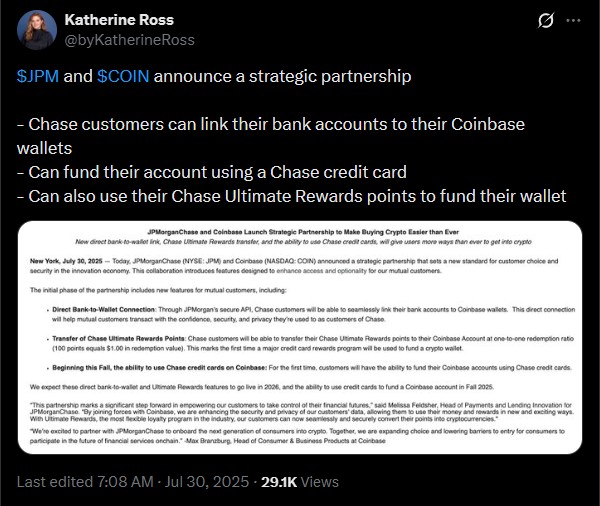

6. JPMorgan Chase: Crypto Access Through Coinbase

JPMorgan doesn’t offer direct Bitcoin investing through Chase, but it does contribute to crypto investment avenues. In July 2025, the bank partnered with Coinbase, allowing investors to use Chase credit cards to buy crypto on Coinbase and redeem their Chase reward points for USDC.

Source: @byKatherineRoss on X

That said, JPMorgan is reportedly looking into cryptocurrency trading services for institutional clients as of December 2025.

7. US Bank: Institutional Custody and ETFs

US Bank resumed its cryptocurrency custody services for institutional clients in September 2025, paired with a Bitcoin ETF offering in an attempt to provide full-service Bitcoin management.

The entity was one of the first to offer institutional crypto custody back in 2021, but paused the offering in early 2022 after the SEC issued Staff Accounting Bulletin (SAB) 121, which prevented banks from offering digital asset custody. The Bulletin has since been rolled back.

8. BNY Mellon: Institutional Custody and On-Chain Cash

BNY Mellon launched a digital asset custody platform in October 2022, allowing select clients to hold and transfer Bitcoin and Ether within its platform.

In January 2026, the bank announced tokenized deposits, or an on-chain “copy” of client deposit balances on its digital assets platform, which will make it easier for clients to manage collateral and margin trading.

9. State Street: Digital Custody and Tokenization

In August 2024, State Street announced a deal with digital asset infrastructure provider Taurus SA to develop digital custody and tokenization services.

Source: @ManoppoMarco on X

The custody part depends on regulatory approval, but alongside Citi, State Street plans to push for custody services in 2026 as US rules develop.

10. Wells Fargo: Spot Bitcoin ETFs

In January 2024, Wells Fargo began offering spot Bitcoin ETFs for purchase through its advisors. Opposite Bank of America, however, Wells Fargo advisors only recommend the asset when clients ask.

Banks are adding Bitcoin support in small steps. They’re incorporating ETFs, then custody, then loans/trading. Recent moves like Morgan Stanley’s crypto ETF filings and BNY’s tokenized deposits show that progress is being made even as early as January 2026.

If you’re a normal customer, understand that most banks aren’t trying to turn you into a day trader. They’re trying to fit Bitcoin into products that traditional investors are already aware of. While these movements can make Bitcoin easier to access, they don’t necessarily make Bitcoin “safe” in terms of risk and volatility.

The asset can still swing fast, fees can add up, and you can still owe taxes when you sell. If you see a bank Bitcoin product, delve into its rules and terms, including fees and withdrawal features. That’s the safest way to get involved in digital assets.

Sometimes, but many banks start with Bitcoin ETFs instead. Direct Bitcoin trading is usually limited to private banking or select clients.

What’s the difference between a Bitcoin ETF and owning Bitcoin?

A Bitcoin ETF gives you price exposure through shares of a fund. Owning Bitcoin means you hold the actual asset, usually with more control but also more responsibility.

Why do banks care so much about custody?

Because custody is about security, rules, and accountability. If a bank can’t store assets safely and report them properly, it won’t offer the product at scale.

Is borrowing against Bitcoin a good idea?

It depends on your situation, but it can backfire quickly. Bitcoin’s price can drop fast, which can trigger collateral calls or forced selling at the worst time.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy