XRP is holding above key support as the XRP Ledger adds $2.6 billion in tokenized assets, expands RLUSD infrastructure and surpasses 1.4 million AI-driven transactions. | Credit: CCN.com

Share

Key Takeaways

XRP transactions on XRPL typically finalize in three to five seconds, but total payment time also depends on local payout rails.

Traditional cross-border payments can still take several days due to correspondent chains and banking-hour limits.

ODL uses XRP as a bridge to reduce prefunding and shorten settlement time in some corridors.

The speed advantage is most visible where banking infrastructure is fragmented or time zones do not overlap.

XRP is a digital asset used on the XRP Ledger (XRPL), a blockchain network that typically finalizes transactions in about three to five seconds.

That speed matters when compared with how traditional cross-border banking still works in many corridors. Payments often move through correspondent banks, face cutoff times, and can take several days in some cases.

Even modern upgrades like SWIFT GPI improve tracking and average delivery times, but they still operate within banking hours and bank-based settlement workflows.

This guide explains how and why XRP can be faster, and where that difference shows up in real payment systems today. It focuses on four global use cases where Ripple’s On-Demand Liquidity (ODL) model uses XRP as a bridge asset to reduce settlement delays, while also explaining the limits that still apply.

A common misunderstanding is that faster settlement automatically means instant cash in hand. In reality, payments involve several steps, including currency conversion, compliance checks, and final payout delivery. XRP mainly affects the settlement leg, not every part of the process.

XRP Speed vs. Bank Transfer Speed: What Faster Really Means

When people compare XRP to banks, they often mix up three timelines.

First is blockchain finality. XRPL ledger versions typically close every three to five seconds, meaning transactions reach finality quickly at the network level.

Second is bank processing time. Banks operate within business hours, batch windows, and settlement schedules. Even same-day systems are not always available overnight, on weekends, or during holidays.

Third is end-to-end delivery, which depends on wallet systems, domestic clearing rails, compliance reviews, and liquidity availability.

ODL focuses on the middle step. Instead of routing funds through multiple correspondent banks, the sender converts fiat currency into XRP, sends XRP across the XRPL, then converts XRP into the destination currency. This reduces reliance on pre-funded accounts and shortens inter-institution settlement delays.

This does not remove regulatory checks or local payout constraints, but it can significantly reduce time spent waiting for cross-border settlement.

Below are four real-world use cases where XRP can be materially faster than traditional banking rails – along with why the speed advantage exists in each scenario.

1. Japan-to-Philippines Remittances (SBI Remit and Coins.ph)

In 2021, SBI Remit launched Japan’s first international remittance service using crypto assets for transfers to the Philippines, working with local liquidity providers and payout partners.

This corridor highlights why settlement speed matters. Japan and the Philippines operate on different banking schedules, and traditional remittance routes often rely on several intermediary banks, which can slow transfers outside standard business hours.

XRP can reduce delays in this flow for several reasons.

The settlement leg does not rely on correspondent banks that process transfers sequentially.

XRPL transactions finalize in seconds instead of waiting for interbank settlement windows.

The model reduces dependence on keeping large balances parked in destination accounts.

For senders, this can mean faster access to funds during evenings and weekends. For providers, it simplifies liquidity management across borders. Final delivery still depends on local payout methods, and regulatory screening can add time even if the blockchain settlement is fast.

XRP-based remittance models. | Credit: ChatGPT

Beyond the original Japan-to-Philippines corridor, SBI Remit expanded the XRP-powered model to support remittances from Japan into bank accounts in the Philippines, Indonesia, and Vietnam, making the service available for multiple major corridors with large worker populations.

📣 $XRP: SBI Remit, an international remittances subsidiary under Japan's SBI Holdings, has expanded its services using XRP-to-bank accounts in the Philippines, Vietnam, and Indonesia 🏦—XRP is the bridge currency 🌉 pic.twitter.com/ZvzGG3EE3u

In addition to established routes, SBI Remit has also been working with other partners such as Siam Commercial Bank (SCB) to add new real-time remittance corridors. According to Ripple’s own case study, this collaboration enables Thai nationals living in Japan to send JPY home and receive Thai baht in recipient accounts within seconds, bypassing some traditional delays and agent-based cash pickup steps.

2. Southeast Asia Multi-Corridor Remittance Networks (Tranglo)

In 2022, Tranglo enabled ODL across twenty-five payment corridors throughout Southeast Asia and nearby regions.

This matters because complexity increases with every additional corridor. Each country has different banks, payout partners, compliance rules, and domestic clearing systems, which often leads to inconsistent settlement times.

Remittances routed through Tranglo’s corridors generally connect countries such as Malaysia, Singapore, Indonesia, the Philippines, Thailand, and Vietnam, where traditional payment rails vary significantly in speed and cost.

By adding XRP as an on-demand bridge between pay-in and pay-out legs, providers can see more predictable settlement timing and fewer bottlenecks compared with a chain of correspondents.

XRP-based settlement can help standardize one part of the process because:

XRPL settlement behaves the same regardless of the destination country.

Payments can be processed continuously rather than only during overlapping banking hours.

Providers can source liquidity when needed instead of relying entirely on prefunded balances.

In hub-style payment networks, reducing settlement friction helps providers rebalance liquidity faster and respond to demand spikes without waiting for interbank transfers to complete.

3. European Marketplace and PSP Treasury Operations (Lemonway)

In 2022, Paris-based payments firm Lemonway partnered with Ripple to use ODL, a service that leverages XRP for faster cross-border settlement. The primary purpose of this integration was to improve how Lemonway manages cross-border treasury flows for marketplace payouts and internal liquidity needs.

Traditional treasury and cross-border payment processes often require firms to pre-fund destination accounts in multiple countries to ensure that payouts can be made quickly. This prefunding ties up capital that could otherwise be used for business operations or expansion.

By using RippleNet’s ODL, underpinned by XRP, Lemonway aimed to reduce the need for prefunding destination accounts abroad. According to the companies’ press announcement, this change gives Lemonway the flexibility to manage liquidity more efficiently and free up previously trapped capital, which can then be deployed elsewhere in the business.

Using XRP as a bridge can shorten the settlement portion of treasury flows.

Funds can be repositioned more quickly between currencies.

Less time is spent waiting for interbank settlement confirmation.

Liquidity can be deployed where needed without maintaining large idle balances.

This can help payment institutions respond faster to shifting transaction volumes, particularly in marketplaces where payout demand can vary sharply between countries. Compliance checks and regulatory reporting still apply and can affect timing.

Lemonway’s chief operating officer stated that ODL allows greater flexibility around when the company makes payments to partners, releasing it from traditional banking cut-off cycles and driving operational efficiencies. The expectation is that these efficiencies can be passed on to Lemonway’s marketplace clients in the form of faster and more predictable settlement.

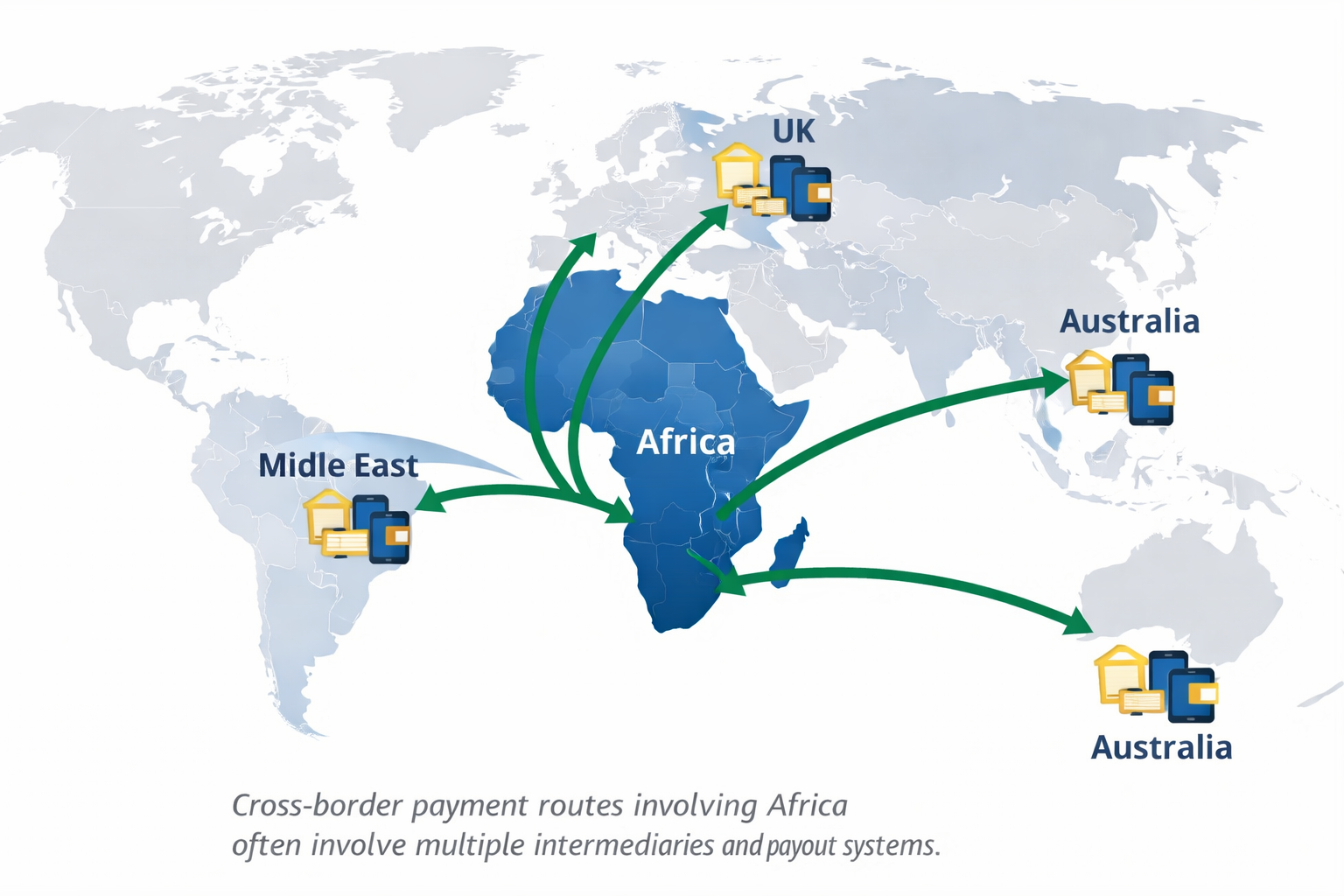

In 2023, Ripple announced a partnership with Onafriq (formerly known as MFS Africa), a major African payments fintech, to expand digital asset-enabled cross-border transfers between Africa and other regions including the Gulf Cooperation Council (GCC), the United Kingdom, and Australia.

Under the agreement, Onafriq is using Ripple Payments, Ripple’s crypto-enabled payments technology, to open three new payment corridors linking Africa with partner platforms such as PayAngel in the UK, Pyypl in the GCC, and Zazi Transfer in Australia. These corridors enable remittance and business payments to recipients in 27 countries across Onafriq’s pan-African network.

Onafriq has one of the largest mobile money footprints in Africa, connecting hundreds of millions of mobile wallets across dozens of nations. By integrating Ripple Payments, the company aims to address common constraints in traditional remittance channels, such as lengthy transfer times, higher costs, and inconsistent settlement. The partnership is framed as bringing faster, more efficient, and cost-effective international money transfers into and out of Africa, which could contribute to broader access to cross-border financial services on the continent.

Many Africa-linked corridors face structural challenges, including:

Fewer direct correspondent relationships.

Higher reliance on intermediary banks

Diverse payout systems across countries

These factors often increase settlement time and cost in traditional banking routes.

XRP-based settlement can reduce some of this friction:

Fewer settlement handoffs can reduce processing delays.

Liquidity can be accessed on demand rather than fully prefunded.

This is particularly relevant where domestic payout rails vary widely between mobile wallets, banks, and cash agents. Reducing cross-border settlement delays allows providers to focus more on last-mile delivery.

However, precise settlement times vary with payout partners and local banking or wallet systems, the integration of blockchain technology aims to reduce dependence on slow correspondent chains and banking-hour limitations that often slow traditional cross-border payments.

Beyond the four core examples above, several notable deployments and partnerships show how XRP and Ripple’s payments technology are being used in real-world cross-border and financial infrastructure contexts.

Ripple Payments Integration With Thunes

In 2025, Ripple expanded its partnership with Thunes, a global cross-border payment network, to enhance real-time payouts in local currencies across financial institutions and businesses.

Under this collaboration, Thunes uses Ripple Payments to support fast, transparent, and reliable cross-border transactions through its Direct Global Network, providing real-time delivery in over 90 payout markets. The integration is designed to improve payment speed and reach, especially in corridors with limited traditional banking infrastructure.

Stablecoin and Liquidity Expansion Around XRP

Ripple’s ecosystem has also seen the introduction and growth of XRPL-native stablecoins like RLUSD, a U.S. dollar-pegged token designed for institutional settlement.

The expansion of stablecoin infrastructure on the XRP Ledger supports faster cross-border corporate and treasury payments by offering a predictable, fiat-linked settlement alternative, which can further complement XRP’s use as a liquidity bridge.

Stablecoin adoption is often coupled with XRP liquidity to enable fast global settlement flows for enterprises and payment providers.

Hidden Road: Prime Brokerage, Collateral, and Post-Trade Settlement

In April 2025, Ripple agreed to acquire Hidden Road, a multi-asset prime broker, for $1.25 billion. Hidden Road’s scale is significant in traditional finance terms: Reuters reported it clears about $3 trillion annually and serves 300+ institutional clients.

Ripple’s stated plan is not just ownership. It intends to bring parts of Hidden Road’s post-trade operations onto the XRP Ledger, which is the piece that ties the acquisition back to settlement speed.

If post-trade settlement and collateral processes can move onto an always-on ledger, institutions potentially reduce delays caused by batch cycles, banking cutoffs, and multi-party reconciliation. The exact rollout timeline and the final scope depend on regulatory and operational implementation, but the use case is clear: XRPL as a settlement layer for institutional-grade prime brokerage workflows.

Why does this matter faster than banking?

Prime brokerage processes often rely on layers of intermediaries, clearing schedules, and collateral movement constraints. Moving parts of that stack onto an always-on ledger targets time lost in the post-trade chain, not just in cross-border remittance.

Ripple’s 2025 Acquisition of Rail: Stablecoin Payments Rails That Complement XRP Flows

In August 2025, Ripple agreed to acquire Rail, a stablecoin payments platform, for $200 million. Ripple framed the deal as expanding stablecoin-based cross-border payment capabilities and integrating them with its RLUSD infrastructure.

This does not mean “XRP equals stablecoins.” But it is a recent, concrete example of Ripple expanding the set of rails used for fast settlement. In practice, institutions may choose between a bridge-asset model (where XRP can function as a liquidity bridge) and stablecoin settlement (where a fiat-pegged asset is preferred).

Both approaches aim at the same bottlenecks traditional banking struggles with: cutoff times, multi-hop settlement, and slow reconciliation.

What Can Still Slow XRP-Based Payments

Even when XRPL settlement is fast, end-to-end delivery can still be affected by several factors, such as:

Availability of liquidity at on-ramps and off-ramps

Price volatility is also a risk institutions must manage. ODL is designed to minimize exposure by moving funds quickly, but volatility remains a consideration in liquidity planning.

Why ‘Seconds’ Matters Even When Swift GPI Can Be ‘Minutes’

It’s tempting to say: “But SWIFT GPI is already fast.” Often, it is. SWIFT says nearly 60% of GPI payments are credited within 30 minutes and almost all within 24 hours. The BIS similarly reports a median processing time under two hours, while also documenting corridor variability from minutes to more than two days.

The difference is that XRP-based settlement can compress the “value transfer” step to seconds and run 24/7, which matters most in four situations:

when corridors are slow or inconsistent,

when weekends/holidays create dead zones,

when liquidity is not pre-positioned, and

when treasury operations need rapid rebalancing.

That’s why “XRP is faster” argument isn’t that banks are always slow, it’s that the banking model still has structural constraints, while XRPL settlement is built to be continuous.

Why This Matters for the Payments Industry

The goal of faster settlement is not simply speed for its own sake. It affects how much capital institutions must lock up, how predictable payments are, and how well providers can operate across time zones.

Banks are improving cross-border payments, but correspondent banking still introduces structural delays in some corridors. XRP-based settlement offers an alternative model that can compress one of the slowest parts of the payment process.

In the cases above, XRP is used not as an investment product but as a settlement tool within regulated payment flows. The speed advantage appears most clearly where traditional banking infrastructure is fragmented or operationally constrained.

For those trying to understand blockchain’s role in finance, the takeaway is practical. Digital assets are increasingly used as infrastructure components that help money move more efficiently between institutions.

Transactions on the XRP Ledger typically reach finality within about three to five seconds, but full payment delivery also depends on conversion and payout systems.

Is XRP always faster than SWIFT payments?

Not in every case. Some SWIFT GPI payments can arrive within minutes. XRP tends to offer clearer advantages in corridors with multiple intermediaries, limited banking-hour overlap, or liquidity constraints.

What does prefunding mean in cross-border payments?

Prefunding means keeping money parked in destination accounts so payouts can be made quickly. Managing many prefunded accounts is costly and can cause delays when balances run low. ODL aims to reduce this need by sourcing liquidity when payments occur.

What limits the speed of crypto-based payment systems?

Local banking rails, compliance checks, and liquidity availability still affect delivery times even if blockchain settlement itself is fast.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

She is a fintech writer based in Canada with an academic background in psychology and project management. She has previously contributed to crypto media platforms, including Cointelegraph. Her professional experience includes work as a relationship manager in the telecommunications industry, and her writing since 2020 has focused on digital assets, blockchain technology, and artificial intelligence, with attention to their interaction with traditional finance.

Easy

Easy