Tokenized Deposits vs Deposit Tokens: XRP’s Role in 2026 Banking | Credit: Hameem Sarwar /CCN

Share

Key Takeaways

Tokenized deposits mainly target banks, large corporations, and financial institutions rather than everyday retail users.

Existing banking laws continue to apply, which limits experimentation but provides legal certainty.

Tokenized deposits improve how banks process settlement and liquidity without changing who controls money issuance.

Most tokenized deposit systems operate in closed or semi-closed networks, which restrict seamless cross-network transfers.

Tokenization has entered a decisive phase. Analysts and financial institutions no longer treat tokenization as an experiment.

Banks, payment providers, and asset managers now test live use cases tied to settlement, liquidity, and balance sheet efficiency.

Tom Zschach argues that while tokenization successfully created a digital representation of assets, it left open the harder question of how trust, verification, and transactional logic travel with those assets as scale, automation, and institutional complexity grow.

In this article, I explore why tokenization solved the “digital container” problem but left a deeper question unanswered: how trust, verification and logic move with assets as volumes grow, automation increases and institutions cross boundaries.👇https://t.co/ZvQp7cx1lt

Forecasts projecting trillions of dollars in tokenized assets by the end of the decade point to a structural shift. Yet this shift depends less on tokenized assets alone and more on the infrastructure that supports how money moves, settles, and maintains trust across institutions.

As adoption accelerates, one distinction continues to blur in industry discussions: the distinction between tokenized deposits and deposit tokens.

The terms often appear side by side and are sometimes used interchangeably.

However, these instruments differ in design, regulatory treatment, and function within the financial system. Treating them as the same obscures how tokenized money fits within existing banking rails and where new infrastructure begins to emerge.

The debate also raises a broader question around interoperability. As banks tokenize liabilities and adopt blockchain-based settlement, fragmentation becomes a growing concern.

This is where XRP enters the conversation. Ripple’s long-standing focus on cross-border payments positions its token as a potential bridge asset, offering a connective layer between fragmented banking systems and tokenized networks that do not naturally interact.

This article explains the difference between tokenized deposits and deposit tokens. Understanding that distinction provides the foundation for assessing where XRP fits within this context.

What Are Tokenized Deposits in Banking and Finance?

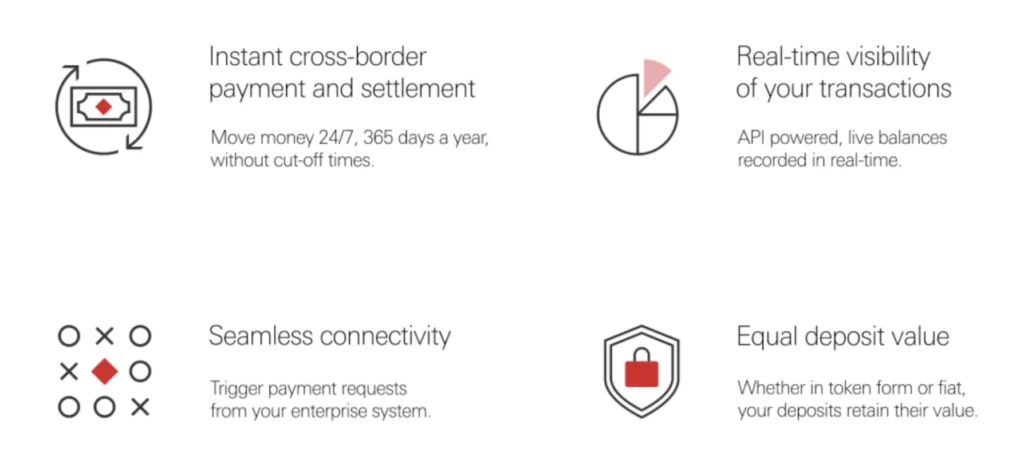

Tokenized deposits are digital representations of fiat bank deposits recorded on a distributed ledger. Banks use them to improve settlement speed, liquidity management, and operational efficiency.

Near real-time settlement reduces reliance on intermediaries and batch-based payment systems, while preserving deposit guarantees, capital requirements, and supervisory oversight.

Issued by regulated banks: A licensed bank issues tokenized deposits to mirror existing deposit liabilities on its balance sheet.

Direct claim on deposits: Each token represents a claim on a bank deposit held at the issuing institution, keeping the structure within the traditional banking system.

No independent circulation: Tokenized deposits do not circulate independently like cryptocurrencies or stablecoins.

Bank accountability: The issuing bank remains responsible for custody, redemption, compliance, and regulatory reporting.

Permissioned environments: Most implementations operate on bank-controlled or permissioned networks, where identity checks, access rights, and transaction rules follow existing financial regulations.

Tokenized deposits mainly support institutional activity rather than consumer payments.

Common use cases include:

Interbank settlement: Faster movement of commercial bank money between regulated institutions.

Corporate treasury operations: Real-time liquidity management and programmable cash flows for large enterprises.

Wholesale payments: Delivery-versus-payment settlement for tokenized securities and financial instruments.

Retail deployment remains limited, as most projects focus on back-end financial infrastructure rather than customer-facing products. Tokenized deposits seek to modernize how banks move money without replacing the existing monetary system.

Deposit Tokens: Native Digital Bank Money

As outlined earlier, tokenized deposits function as a digital mirror of existing bank deposits. Deposit tokens represent a different concept.

Deposit tokens are designed as native digital representations of commercial bank money. Rather than reflecting a pre-existing deposit, they are issued as standardized digital units intended to circulate within a regulated financial system.

Native digital issuance: Deposit tokens are created as digital units of commercial bank money rather than mirrors of existing deposit balances.

Interoperability focus: Banks and industry groups design deposit tokens to move across institutions and platforms instead of remaining confined to a single bank’s internal system.

Shared settlement infrastructure: Deposit tokens aim to operate on common rails that support cross-bank settlement and standardized payment logic.

Regulated framework: These tokens preserve core features of bank money, including regulatory oversight, compliance requirements, and settlement finality.

This approach responds to a growing challenge. As banks tokenize assets and liabilities on separate systems, fragmentation increases. Deposit tokens seek to provide a unified settlement layer that supports scale, automation, and cross-institutional activity, setting the stage for the real-world examples.

Aspect

Tokenized Deposits

Deposit Tokens

Core concept

Digital representation (mirror) of existing bank deposits

Native digital form of commercial bank money

Issuance model

Token issued to represent a pre-existing deposit on a bank’s balance sheet

Token issued as a standardized digital unit of bank money

Relationship to deposits

Direct claim on a specific bank deposit

Represents bank money itself, not a mirrored balance

Circulation

Limited circulation within the issuing bank’s network

Designed to circulate across institutions and platforms

Interoperability

Low by design; typically confined to a single bank or closed network

High by intent; built to move across banks and shared rails

Fully embedded in existing banking laws and supervision

Regulated bank money with new standardized digital frameworks

Liquidity management

Improves internal liquidity efficiency

Enables system-wide liquidity mobility

Retail usage

Rare; focused on back-end infrastructure

Potentially extensible, but currently wholesale-focused

Fragmentation risk

High as each bank operates its own system

Lower, designed to reduce fragmentation

How Global Banks Are Approaching Tokenized Deposits and Deposit Tokens in 2026

Several global banks have launched live systems or advanced pilots involving tokenized forms of bank money. These initiatives do not follow a single model. Some focus on tokenized deposits that mirror existing bank liabilities, while others explore tokenized money structures that move closer to deposit-token designs.

Most activity remains concentrated in wholesale finance, interbank settlement, and institutional payments rather than retail banking.

JPMorgan Chase (JPM Coin and Onyx Digital Assets): JPMorgan operates one of the most mature tokenized deposit systems in production. JPM Coin, also referred to as JPMD in recent deployments, represents commercial bank deposits issued by JPMorgan and used by institutional clients to move U.S. dollar and euro-denominated balances across permissioned networks and selected public blockchain environments. Use cases include intraday liquidity management, cross-border payments, and on-chain settlement within the bank’s ecosystem.

Citi (Citi Token Services): Citi has introduced tokenized deposits for corporate treasury and trade finance. The platform supports near real-time settlement, programmable payments, and automated liquidity controls for multinational firms operating across jurisdictions.

UBS (Tokenized deposit integration with SIX Digital Exchange): UBS has run advanced pilots integrating tokenized bank money with Switzerland’s regulated digital asset exchange. These initiatives support delivery-versus-payment settlement for tokenized securities, while deposits remain on the bank’s balance sheet within existing regulatory structures.

HSBC (Tokenized Deposit Service): HSBC has launched a Tokenized Deposit Service focused on wholesale payments and settlement, with initial deployments expanding across key jurisdictions. The initiative positions tokenized bank money as a regulated settlement asset, while HSBC’s Orion platform remains primarily focused on asset tokenization.

Deutsche Bank (DLT-based deposit and settlement pilots): Deutsche Bank continues to participate in distributed ledger pilots involving tokenized bank money, focusing on regulated settlement layers for wholesale payments and financial market infrastructure rather than live issuance.

Characteristics of tokenized deposits | Source: HSBC

Across these initiatives, the direction is consistent. Banks aim to modernize settlement, improve liquidity efficiency, and retain regulatory control, while testing different technical paths toward scalable, interoperable bank-issued digital money.

Where XRP Fits: Bridging Fragmented Tokenized Systems

XRP enters the debate at the interoperability layer rather than at the deposit or issuance level. As banks tokenize deposits, assets, and settlement processes on separate platforms, the ability to move value between disconnected systems becomes a limiting factor.

Ripple positions XRP as a bridge asset designed to facilitate value transfer across networks that do not share a common settlement rail.

In this model, XRP does not replace bank-issued money or deposit tokens. Instead, it acts as an intermediary asset that enables liquidity to move between institutions, jurisdictions, and tokenized environments without requiring bilateral integration.

This positioning aligns with a broader challenge facing tokenized finance. As tokenized deposits and deposit tokens proliferate across permissioned and hybrid networks, interoperability becomes a coordination problem rather than a technological one.

XRP targets that gap by offering a neutral asset layer designed to reduce friction where direct connectivity is not possible.

Whether this model gains wider institutional traction depends on regulatory clarity, network adoption, and the willingness of banks to rely on external liquidity bridges rather than shared internal standards.

How SWIFT Approaches Tokenized Finance and Interoperability

SWIFT addresses the same fragmentation challenge from a different angle. Rather than introducing a new settlement asset, SWIFT focuses on messaging, coordination, and interoperability across existing financial infrastructure.

Through initiatives such as blockchain interoperability pilots and integration with tokenized asset platforms, SWIFT aims to connect tokenized systems without altering the underlying form of money.

Its approach emphasizes compatibility with existing correspondent banking models, regulatory frameworks, and central bank systems.

This creates a structural contrast. XRP represents an asset-based bridge designed to move value across disconnected networks. SWIFT represents a coordination layer designed to connect systems while leaving settlement assets unchanged.

XRP and SWIFT: Two Approaches to Interoperability

Both approaches respond to the same underlying issue. As banks tokenize deposits, assets, and settlement processes in parallel, fragmentation increases.

The market now tests whether interoperability emerges through shared messaging standards, neutral bridge assets, or a combination of both.

Aspect

XRP (Ripple)

SWIFT

Core role

Bridge asset

Messaging coordination network

Primary function

Moves value across networks

Connects financial institutions

Settlement model

Asset-based intermediary settlement

Messaging without asset settlement

Tokenized deposit role

Does not issue deposits

Does not issue deposits

Interoperability approach

Asset-based liquidity bridge

Standards-based system connectivity

Regulatory position

Digital asset regulatory frameworks

Embedded global banking infrastructure

How Tom Zschach Frames the Interoperability Challenge and the Future

Tom Zschach has noted that while tokenization solved the problem of creating digital representations of assets, it left unresolved core elements: how trust, verification, and transactional logic scale across institutions and systems.

This unresolved problem explains why both XRP and SWIFT remain relevant in the tokenized finance debate.

SWIFT approaches the problem by extending coordination and messaging standards into tokenized environments, aiming to carry trust and logic across systems without changing the form of money.

XRP approaches the same challenge through an asset-based bridge, designed to move value where shared infrastructure does not yet exist.

Together, these approaches highlight the core issue facing tokenized finance. As banks tokenize deposits and assets on parallel systems, interoperability becomes less about technology and more about how trust and settlement travel across institutional boundaries.

Looking ahead, the future of tokenized finance will depend less on who builds the fastest or cheapest network and more on who can move trust, settlement, and finality across fragmented systems.

As banks, market infrastructures, and private networks tokenize assets in parallel, no single chain or standard will dominate. Interoperability will define whether tokenization scales beyond pilots, and success will come from frameworks that allow value and confidence to travel together across institutions, jurisdictions, and technologies without forcing the financial system into a single model.

Can tokenized deposits move across different blockchains?

Most current systems, including Kinexys by J.P. Morgan, operate on permissioned networks. By 2026, banks will have begun adopting interoperability frameworks such as SWIFT’s blockchain initiatives and the Regulated Liability Network to enable transfers of tokenized money across private ledgers and selected public blockchains, including Ethereum.

Do tokenized deposits earn interest like traditional bank deposits?

Yes. In 2026, most institutional tokenized deposits are structured as demand deposit accounts under existing banking law. This structure allows them to retain interest-bearing features, a distinction that separates them from many stablecoins used in settlement and liquidity markets.

Are tokenized deposits protected by deposit insurance?

In major jurisdictions, regulators have clarified that tokenized deposits issued by licensed banks qualify for standard deposit insurance. Coverage applies as long as the deposits remain on the bank’s balance sheet and comply with existing record-keeping and supervisory requirements.

Could tokenized deposits replace stablecoins in institutional finance?

Tokenized deposits have increasingly replaced stablecoins in wholesale settlement and interbank transfers. Stablecoins such as USDC and USDT continue to dominate retail and decentralized finance activity, while banks favor tokenized deposits for regulated, high-value transactions.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy