SWIFT Completes Multi-Bank Tokenized Bond Settlement Trial Using Stablecoins and ISO 20022 — What Does This Mean for XRP and XLM?

Share

Key Takeaways

SWIFT is integrating a blockchain-based shared ledger to enable instant, 24/7 cross-border settlements, bringing crypto-level speed to traditional finance.

Unlike XRP Ledger (XRPL) or Hedera Hashgraph (HBAR) networks, SWIFT’s system will remain token-agnostic, supporting regulated assets.

Built with ConsenSys Linea (Ethereum layer-2), SWIFT’s ledger combines scalability, privacy, and interoperability.

SWIFT’s model connects traditional banking rails to tokenized finance, allowing banks to move digital assets securely across networks.

Cryptocurrency enthusiasts have long promised a revolution in finance: instant cross-border payments, around-the-clock settlements, lower fees, and a more inclusive global system.

More than a decade since Bitcoin’s birth and years into experiments like Ripple’s XRPL network, that promise remains only partially fulfilled. While crypto networks can move money in seconds, traditional banking still leans on slower, older systems for most international transfers.

Now, an unlikely player, SWIFT, the 50-year-old cooperative backbone of global banking, is stepping in with a bold initiative. SWIFT plans to integrate a blockchain-based shared ledger into its infrastructure, aiming to deliver many of crypto’s benefits without relying on any cryptocurrency token.

This article explores whether SWIFT’s new ledger could realize crypto’s vision in mainstream finance, how it compares to crypto-native solutions, and what it means for the future of money movement. We will break down the technical and practical implications in an accessible way, balancing journalistic neutrality with a deep dive into facts.

By the end, you’ll have a clear understanding of the stakes and whether the “crypto revolution” might arrive via familiar banking rails instead of Silicon Valley startups.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Crypto’s Role in Revolutionizing Cross-Border Finance

The global financial system has long struggled with slow, expensive, and fragmented cross-border payment networks. Sending money across countries often involves multiple intermediaries, high fees, and delays that can stretch for days.

Cryptocurrencies and blockchain technology emerged as a response to these inefficiencies, offering a vision of a faster, cheaper, and more transparent financial infrastructure.

By replacing traditional intermediaries with decentralized networks, crypto has introduced the possibility of real-time, peer-to-peer value transfer that transcends borders and banking hours.

Fast, Low-Cost, Always-On Payments

One of cryptocurrency’s greatest promises is the ability to move money globally as quickly and easily as sending an email. On blockchain networks, digital tokens can be transferred within seconds, without relying on the chain of intermediary banks that slow traditional systems.

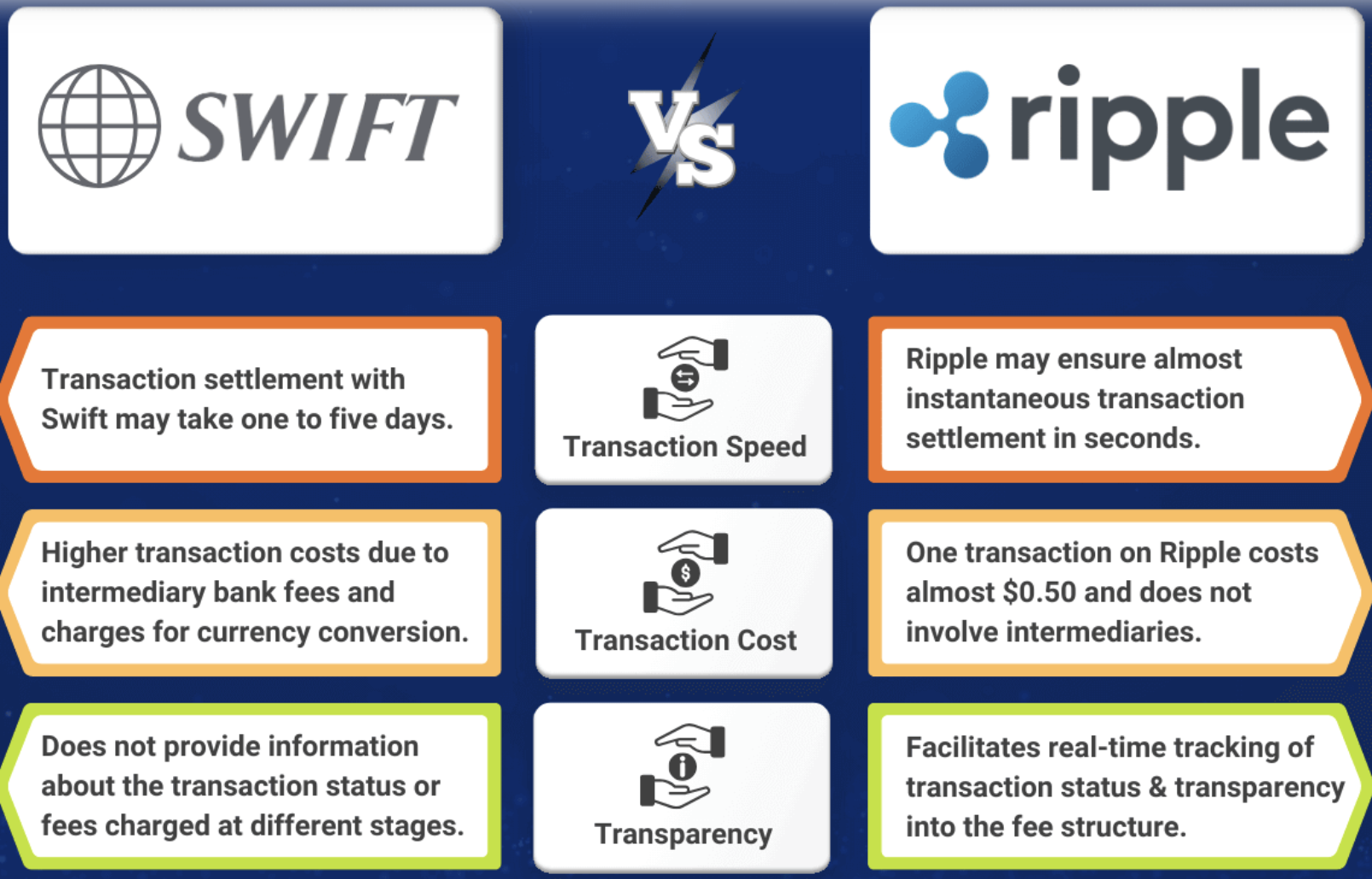

For example, the XRP Ledger (XRPL) can settle international payments in just 3–5 seconds with fees as low as $0.0002. In contrast, a standard SWIFT wire transfer may take 1–3 business days and incur significant fees as transactions pass through multiple correspondent banks.

Beyond speed and affordability, cryptocurrency networks operate 24/7, unaffected by weekends, holidays, or business hours. This “always-on” accessibility creates a true global payment system that functions in real time, ideal for businesses and individuals operating across borders.

Disintermediation and Financial Inclusion

Cryptocurrency technology was also designed to disintermediate global finance, removing the need for centralized clearinghouses such as SWIFT or large correspondent banks.

In an ideal blockchain-powered world, a small business in Nigeria could send funds directly to a supplier in Brazil using a shared digital asset or interoperable tokens. This approach eliminates dependency on correspondent banking relationships and opens financial access to those underserved by traditional institutions.

Stablecoins, which are cryptocurrencies pegged to fiat currencies like the U.S. dollar, have become especially popular for cross-border payments. In many regions with limited banking infrastructure, stablecoins provide a reliable digital alternative for remittances and international transfers.

Transactions using dollar-linked stablecoins on networks such as Stellar or Ethereum can settle in minutes rather than days, often at a fraction of the cost charged by money transfer operators.

The Growing Bridge Between Crypto and Banking

As blockchain technology matures, the line between decentralized finance and traditional banking continues to blur. Financial institutions are no longer dismissing crypto as a passing trend; instead, many are exploring how digital assets, blockchain-based settlement systems, and tokenized liquidity could enhance their operations.

Fintech firms are leading pilot programs for instant remittances, treasury management, and liquidity sourcing through blockchain rails. These initiatives represent early steps toward integrating crypto efficiency into regulated financial ecosystems, setting the stage for broader adoption and policy development.

Progress and Limitations

Despite clear advantages, mainstream adoption by major banks and payment networks remains slow. A few fintech-oriented institutions have begun experimenting with crypto-based solutions.

Ripple, the company behind XRP, reported processing more than $1.3 trillion in transaction volume during the first half of 2025, with some banks using its network for remittances across Asia and Latin America.

Yet, most large financial institutions have not shifted to public blockchains for moving customer funds. Concerns about volatility, regulatory uncertainty, and operational trust remain key barriers.

Crypto tokens can fluctuate significantly in value, which is unacceptable for institutions requiring predictable settlement amounts. Additionally, regulatory ambiguity, such as unclear classifications of whether tokens are securities or commodities, has led to legal challenges and compliance risks.

This creates a paradox: while public blockchains are designed to be “trustless,” traditional banks depend on trust, such as legal frameworks, accountable entities, and mechanisms for dispute resolution. The decentralized nature that makes crypto so powerful also makes it challenging for institutions that must comply with strict governance and financial laws.

XRP vs. the Banking System: A Case Study

Ripple’s XRP Ledger is often presented as a potential successor to the SWIFT network. It uses XRP as a bridge currency, converting one party’s local currency to XRP, transferring it across the ledger, and converting it back into the recipient’s currency.

This system eliminates the need for pre-funded nostro and vostro accounts, freeing up capital and improving liquidity. Ripple’s On-Demand Liquidity (ODL) service claims to reduce capital requirements by up to 45% by removing idle funds in foreign accounts.

However, banks remain cautious. Many executives argue that relying on an external token for settlement introduces risks that traditional finance is not structured to manage. While crypto can provide liquidity and speed, institutions prioritize legal enforceability and compliance.

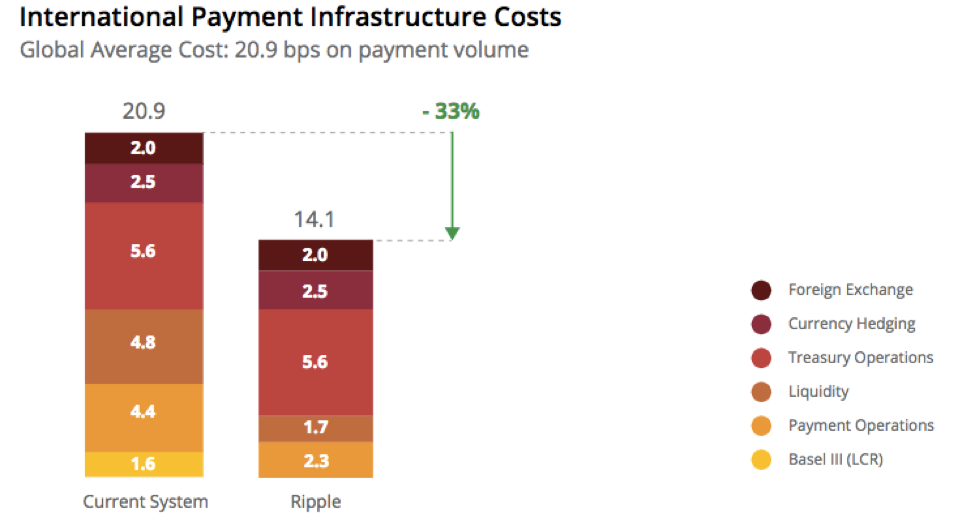

International payment infrastructure costs. | Credit: Penser

Banks prefer instruments they issue and control, such as deposits or central bank money, over decentralized tokens that sit outside regulated balance sheets.

Moreover, crypto networks lack the established trust and governance frameworks that financial institutions depend on. Without standardized legal protections or shared oversight, public blockchains can feel like “a fast engine with no cockpit” from a risk management perspective.

This explains why, despite impressive technological achievements, banks have largely remained on the sidelines.

What Is SWIFT’s Blockchain-Based Ledger

In a twist of fate, the global banking cooperative SWIFT is now adopting the same blockchain technology that once posed a threat to its dominance.

In September 2025, the network announced plans to launch a blockchain-based shared ledger, a landmark move unveiled at the annual Sibos conference. The project aims to make instant, 24/7 cross-border payments a reality across its global network of over 11,000 institutions.

Unlike public crypto systems, SWIFT is not issuing a new coin. Instead, it is creating a permissioned, token-agnostic ledger in collaboration with ConsenSys and more than 30 major financial institutions. The initiative blends the speed of blockchain with the trust, governance, and regulatory standards expected in global finance.

Key highlights of SWIFT’s blockchain initiative:

Purpose: To provide a shared, tamper-proof ledger for secure and real-time interbank transactions.

Functionality: Each transaction, payment or asset transfer, is recorded, validated, and sequenced on the ledger, with smart contracts enforcing compliance rules automatically.

Scope: Designed to support any regulated tokenized value, such as central bank digital currencies (CBDCs), tokenized deposits, and digital securities.

Neutral design: SWIFT will not issue its own cryptocurrency. Instead, banks or central banks can use their own digital tokens, maintaining SWIFT’s traditional neutrality as the network provider, not a money issuer.

Participants: Over 16 leading global banks are already involved, shaping the system for real-world scalability and compliance.

This initiative marks SWIFT’s transformation into a neutral digital bridge, connecting traditional banking systems with the emerging world of tokenized finance.

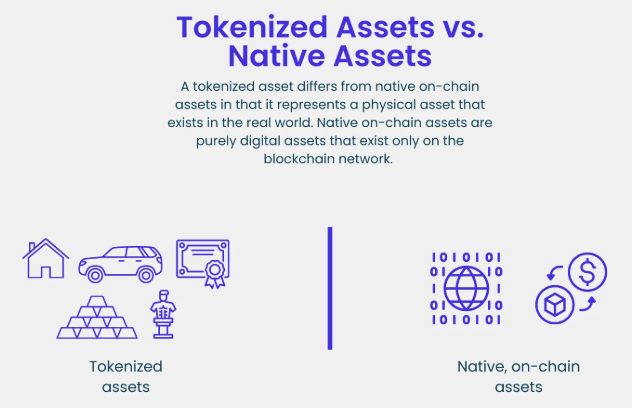

Neutral Infrastructure vs. Native Crypto Assets

At the core of today’s financial transformation lies a key philosophical divide:

Should a payments network depend on a native cryptocurrency to move value, or remain neutral, letting participants choose their own assets?

Tokenized assets vs. native assets. | Credit: Kaleido

SWIFT’s new blockchain-based ledger firmly takes the neutral infrastructure approach, in contrast to networks like XRP Ledger (XRPL) or Stellar, which rely on their own tokens.

1. Settlement Asset

Crypto-ledgers (e.g., XRPL, Stellar): Use a bridge token (like XRP or XLM) to facilitate currency conversion and liquidity across borders.

SWIFT’s model: Uses regulated digital assets, such as tokenized bank deposits or CBDCs, as the settlement medium.

There is no SWIFT Coin: The system allows multiple token types chosen by banks or central banks, maintaining flexibility and avoiding conflicts of interest.

2. Trust Model and Governance

Public blockchains: Open and decentralized; anyone can participate, but accountability and legal recourse are limited.

SWIFT’s ledger: Permissioned and governed by regulated institutions with shared rules and legal frameworks.

This ensures clear accountability, compliance, and dispute resolution, crucial for institutions handling billions in value.

3. Liquidity and Market Access

Native-token systems offer global, built-in liquidity through open markets.

SWIFT’s system relies on existing bank liquidity, FX markets, and market makers, giving institutions control over how and where they source funds.

This aligns with how banks already operate, reducing volatility risk.

4. Compliance and Transparency

Public networks allow pseudonymity, creating regulatory challenges.

SWIFT’s permissioned design embeds KYC/AML controls, data privacy, and auditable transactions, ensuring regulatory confidence from day one.

Ultimately, SWIFT’s approach represents a cooperative, institution-grade middle ground, combining blockchain innovation with the governance, security, and neutrality global finance demands.

Beyond Buzzwords: Tokenized Deposits, Stablecoins and CBDCs Explained

When discussing SWIFT’s blockchain initiative, three terms dominate the conversation: tokenized deposits, stablecoins, and CBDCs. These represent the foundation of the new “digital money stack” that SWIFT’s ledger is designed to support. Here’s what they mean in plain terms and why they matter.

Stablecoins

What they are: Digital tokens issued by private companies and pegged to fiat currency (e.g., 1 token = $1).

How they work: Operate on public blockchains like Ethereum, allowing instant, global, 24/7 value transfer.

Benefits: Combine the stability of fiat money with crypto’s speed and flexibility.

Risks: Depend on issuer transparency and reserve backing; regulators are tightening rules through frameworks like the EU’s MiCA and proposed U.S. stablecoin laws.

Tokenized Deposits

What they are: A bank deposit represented as a digital token on a blockchain, still a direct liability of the issuing bank.

Example use cases: JPMorgan and Citi have issued tokenized dollar deposits for interbank payments and trading.

Advantages:

Instant settlement across platforms.

Smart-contract compatibility (for escrow, trade finance, and delivery-vs-payment).

Legal certainty since they remain regulated deposits.

Scope: Primarily used among KYC-verified institutions, forming part of permissioned finance rather than open crypto markets.

Central Bank Digital Currencies (CBDCs)

What they are: Digital versions of national currencies issued directly by central banks (e.g., the digital yuan or e-krona).

Challenges: Cross-border use and interoperability between different jurisdictions remain complex.

Why They Matter for SWIFT’s Ledger

SWIFT’s blockchain isn’t launching its own currency, it acts as a neutral platform.

Banks and central banks can move any regulated digital form of money, tokenized deposits, CBDCs, or regulated stablecoins.

SWIFT provides the rails, rules, and interoperability, while the money itself remains issued and backed by trusted institutions.

This neutrality ensures SWIFT modernizes money movement without competing with banks, reinforcing its role as the global connector for regulated digital finance.

ISO 20022: The Data Upgrade Enabling This Shift

Behind SWIFT’s blockchain modernization is another quiet revolution — ISO 20022, a new global messaging standard for financial communications. While it may sound technical, this data upgrade is the backbone of how digital money and tokenized assets will move across systems.

What Is ISO 20022?

A modern language for payments: It replaces SWIFT’s legacy MT messages with a richer, structured format (XML/JSON-based).

Data-rich messages: Enables banks to include detailed information, such as invoice numbers, purpose codes, and beneficiary details, within each transaction.

Global adoption: All major payment systems are migrating to ISO 20022, with full enforcement for cross-border payments expected by late 2025.

Why It Matters for Blockchain and Tokenized Money

Smart contract automation: Structured data can directly trigger on-ledger actions, such as compliance checks, conditional settlements, or automated trade payments.

Compliance built-in: Richer data allows real-time KYC/AML screening, reducing manual interventions and fraud risk.

Interoperability: A common standard ensures traditional banking systems can interact seamlessly with blockchain networks and digital asset platforms.

Transparency and analytics: Standardized data improves auditability and enables deeper insights into transaction flows for banks and regulators alike.

How It Complements SWIFT’s Blockchain Ledger

SWIFT’s new ledger will natively support ISO 20022 messages, allowing legacy systems to connect easily.

Payments, digital tokens, and smart contracts will “speak the same language,” ensuring continuity between old and new infrastructure.

As the coexistence period with MT messages ends in November 2025, the timing aligns perfectly with SWIFT’s blockchain rollout, merging data modernization and distributed ledger innovation.

Delivering on Crypto’s Benefits – What Changes and What Stays the Same

SWIFT’s blockchain project aims to capture the speed, efficiency, and transparency that made cryptocurrencies revolutionary, while retaining the trust and control of regulated finance. Here’s what could truly change, and what might remain the same, as banks move onto blockchain rails.

Speed and Settlement Time

Current system: Cross-border transfers often take 1–3 days due to multiple intermediaries.

With SWIFT’s ledger: Transactions could settle within seconds or minutes, operating 24/7 regardless of time zones or bank hours.

Traditional process: Each intermediary bank charges fees and manual compliance adds operational cost.

New model: Direct settlement between banks on a shared ledger eliminates many intermediaries and automates compliance.

Result: Lower transaction costs and fewer reconciliation delays, benefiting both large institutions and smaller banks.

Transparency and Traceability

Before: Tracking payments across borders required multiple confirmations and often lacked real-time visibility.

After: The blockchain ledger provides a single, immutable audit trail, showing the exact status of every transaction.

Value add: Enhances dispute resolution and allows regulators controlled visibility for systemic oversight.

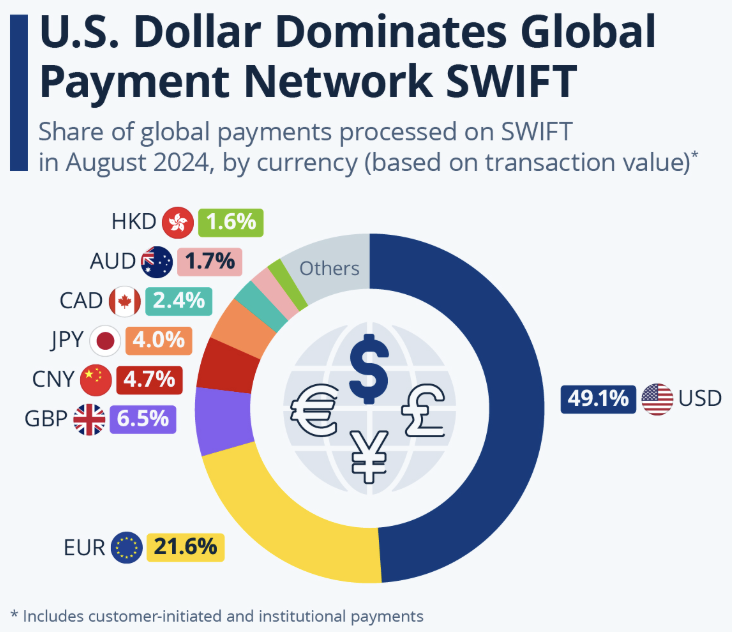

U.S. dollar dominates global payment network SWIFT. | Credit: SWIFT

Interoperability and Unified Access

Vision: SWIFT’s ledger connects to multiple blockchain networks, CBDC platforms, and legacy payment systems.

Function: Acts as a universal translator of value, allowing banks to settle tokenized assets and cash across diverse platforms.

Outcome: Simplifies integration — one connection to SWIFT could enable access to multiple digital asset ecosystems.

Liquidity and Capital Optimization

Problem today: Banks tie up billions in Nostro accounts worldwide to ensure liquidity for payments.

Solution: Instant settlement and payment-versus-payment (PvP) mechanisms reduce the need for pre-funded accounts.

Benefit: Frees capital, boosts treasury efficiency, and allows real-time liquidity management, similar to crypto’s “always-on” markets.

Challenges and Questions Ahead

While SWIFT’s blockchain-ledger vision holds enormous promise, its success depends on overcoming a set of technical, regulatory, and operational hurdles. Transforming the backbone of global finance is no small feat. Here are the key challenges SWIFT and its member banks must navigate.

1. Regulatory Harmony Across Borders

The challenge: Banking and digital asset regulations differ widely across countries — from data privacy to anti-money-laundering (AML) and sanctions rules.

Risk: A cross-border payment on the ledger may be subject to conflicting regulations, slowing adoption or creating compliance gaps.

What SWIFT must do:

Build flexible rulebooks that satisfy the strictest common denominators among regulators.

Integrate travel rule compliance (originator and beneficiary data) into the ledger’s design.

Maintain close collaboration with central banks and oversight bodies, leveraging SWIFT’s long history of regulatory partnership.

2. Integration with Legacy Systems

Current reality: Banks rely on decades-old core systems that can’t easily “talk” to blockchains.

Transition risk: A sudden migration could disrupt operations or cause data mismatches.

Practical path forward:

Run dual systems temporarily (traditional + blockchain) until stability is proven.

Offer “ledger-as-a-service” or integration toolkits for smaller banks.

Provide shared infrastructure and technical support to ensure equal access across institutions.

3. Operational Resilience and Security

New risks: Even permissioned blockchains face cyber, governance, and smart contract vulnerabilities.

Key requirements:

Strict cybersecurity and node certification standards (similar to SWIFT’s CSP framework).

Robust incident response plans and fallback mechanisms to traditional rails.

Continuous software synchronization and security updates across participating banks.

Goal: Maintain SWIFT’s reputation for reliability while introducing next-generation infrastructure.

4. Governance and Legal Clarity

Governance question: Who sets the rules and maintains the ledger’s integrity?

SWIFT’s advantage: Its cooperative structure allows shared decision-making, but large banks may dominate unless governance is balanced.

What’s needed:

Transparent, multi-tier governance models giving a voice to regional and mid-sized banks.

Clear legal recognition that on-ledger transactions represent final settlement under global law.

Standardized dispute-resolution mechanisms for smart contract or settlement errors.

5. Competition and Coexistence with Crypto Networks

Market reality: Public crypto and fintech platforms (Ripple, Stellar, Lightning, Visa, Mastercard) are evolving rapidly.

SWIFT’s challenge: Stay relevant and agile while maintaining compliance-heavy standards.

Likely outcome: Coexistence — SWIFT for regulated interbank flows, public networks for open, retail, and DeFi use cases.

Opportunity: If SWIFT’s platform can bridge to public blockchains, it may unify both ecosystems, enabling value exchange between regulated finance and crypto.

6. Achieving Broad Adoption

Network effect: The system only works if a critical mass of banks join.

SWIFT’s blockchain initiative represents a historic moment in financial innovation, an acknowledgment that the infrastructure powering global money movement must evolve for the digital era.

The question is not whether blockchain can transform finance, but whether it can do so without the “crypto” part, without public tokens, anonymous participation, or open access.

Delivering on Crypto’s Vision — the Institutional Way

In many ways, SWIFT’s project captures the essence of crypto’s promise:

Near-instant settlement across borders.

24/7 availability, unaffected by time zones or bank holidays.

Lower costs and fewer intermediaries, thanks to shared infrastructure.

Transparent, auditable transactions, visible in real time to participants and regulators.

Yet, unlike Bitcoin or XRP, SWIFT’s ledger achieves these through regulated, permissioned collaboration among banks, not decentralized competition. This structure gives the system what crypto has often lacked: legal clarity, accountability, and institutional trust.

By avoiding the launch of its own currency, SWIFT ensures that banks use digital money they already issue or regulate, removing volatility and compliance risks that have slowed crypto adoption.

A Hybrid Model for the Future of Finance

SWIFT’s strategy effectively merges the efficiency of blockchain with the stability of traditional finance. It retains central oversight while enabling tokenized value to move globally with crypto-like speed. In doing so, SWIFT positions itself as the “bridge” between central banks, commercial banks, and emerging digital asset networks.

This model may not be “open finance” in the pure crypto sense, but it could deliver the best of both worlds:

The innovation of digital tokens and smart contracts.

The regulatory assurance and governance that the banking sector requires.

For banks, this means modernization without disruption. For customers, it means payments that work — faster, cheaper, and more predictable.

The Likely Outcome

If successful, SWIFT’s blockchain ledger could become the global backbone for digital value exchange, fulfilling much of crypto’s original vision, but through a trusted institutional framework. The open crypto world will continue to innovate independently, but SWIFT’s move ensures that traditional finance evolves alongside it, not against it.

In short, crypto’s promise may not vanish into regulation, it may be realized through it. SWIFT’s ledger doesn’t replace banks; it redefines how they connect, proving that the future of money might be decentralized in technology, but centralized in trust.

SWIFT’s new ledger is a permissioned blockchain platform that enables instant, 24/7 cross-border settlements between banks. It records and validates transactions in real time, using smart contracts for compliance and automation, but without issuing its own cryptocurrency.

How is SWIFT’s blockchain different from crypto networks like XRP or Bitcoin?

Unlike public crypto networks, SWIFT’s ledger is closed and regulated. It doesn’t rely on a native token or open participation. Instead, it uses tokenized bank deposits, CBDCs, or stablecoins issued by trusted institutions, ensuring compliance and stability for global finance.

What role does Ethereum play in SWIFT’s new system?

SWIFT’s prototype is built with Ethereum layer-2 (Linea) technology, developed by ConsenSys. This gives it the speed and scalability of modern blockchain networks while maintaining privacy, control, and interoperability required by regulated banks.

When will SWIFT’s blockchain ledger launch?

Pilot testing began in 2025, with early participation from over 30 major global banks. Full rollout is expected to align with SWIFT’s ISO 20022 migration completion by late 2025–2026, marking the next phase of global payment modernization.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy