Explore whether Ripple’s technology can thrive without relying on the $XRP token, a deep dive into its fintech future, strategy, and innovation. | Credit: CCN.com

Share

Key Takeaways

ChatGPT argues that SWIFT and Ripple can complement each other, combining traditional financial governance with blockchain efficiency.

AI will play a pivotal role in optimizing settlements, monitoring compliance, and managing liquidity across both rails.

Regulatory clarity and operational trust are essential before large-scale deployment can occur.

The future of global payments is collaborative, driven by interoperability between legacy systems, digital assets, and intelligent automation.

For over 50 years, SWIFT has powered the global banking network, connecting more than 11,000 institutions worldwide. But in an era demanding instant and low-cost payments, traditional correspondent banking faces growing pressure.

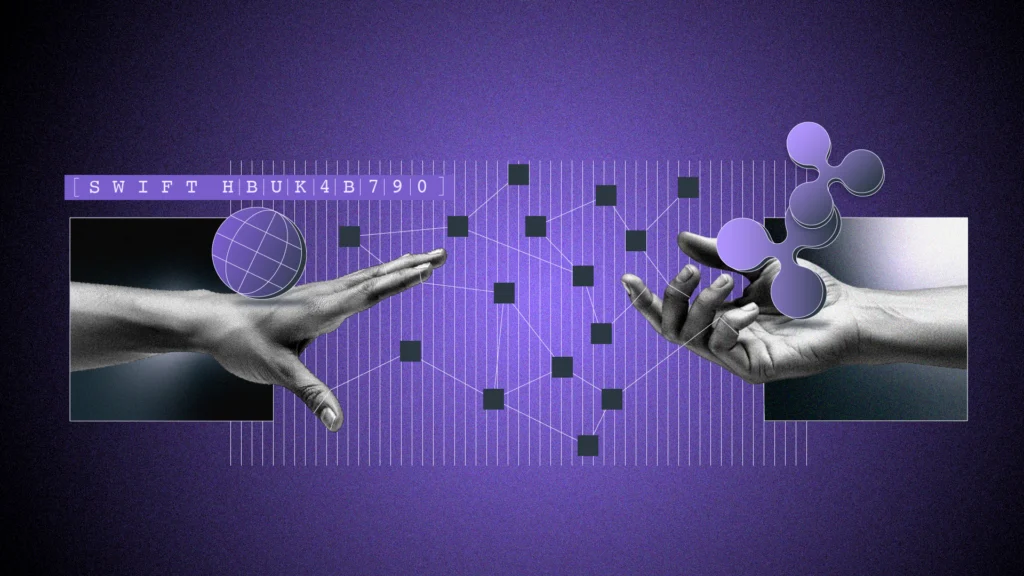

Now imagine a future where SWIFT and Ripple join forces. A dual-rail global settlement system could revolutionize how money moves across borders, combining SWIFT’s reach with Ripple’s real-time efficiency.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

How a SWIFT–Ripple Dual-Rail System Would Work: ChatGPT Weighs In

A dual-rail payment system connects two distinct yet interoperable layers, each handling a different part of the cross-border transaction process.

1. SWIFT for Messaging and Compliance

SWIFT would continue to manage secure financial messaging, ISO 20022 data formats, and global regulatory compliance. This preserves the trust, governance, and standardization that banks depend on.

2. Ripple for Instant Settlement

Ripple’s blockchain would handle actual fund settlement using either digital assets (such as XRP) or tokenized fiat currencies. This approach reduces reliance on pre-funded Nostro accounts and enables faster liquidity management.

3. API Connectors and Gateways

Banks and payment providers could adopt standardized API connectors that translate SWIFT messages into Ripple blockchain transactions and back again.

This allows seamless interoperability without replacing existing legacy systems.

Key Benefits of a SWIFT–Ripple Partnership

A potential SWIFT–Ripple partnership could redefine how money moves across borders by combining the global trust and standardization of SWIFT with the speed and transparency of Ripple’s blockchain network. This dual-rail approach would not only modernize international settlement but also deliver measurable improvements in speed, cost efficiency, and regulatory compliance.

Below are the key benefits such a collaboration could unlock for banks, payment service providers, and end users alike.

Faster payments across borders: Traditional SWIFT transactions can take two to three days. In contrast, Ripple’s blockchain can settle in seconds, offering instant confirmation and payment finality.

Lower costs and reduced nostro balances: Using on-demand liquidity eliminates the need for large, idle pre-funded accounts. This frees up working capital and reduces foreign exchange exposure for banks and corporates.

Continuous 24/7 global operations: Ripple’s blockchain operates around the clock, unlike traditional banking hours. This is ideal for real-time treasury operations, e-commerce, and cross-border remittance flows.

Enhanced transparency and compliance: By combining SWIFT’s ISO 20022 messaging with Ripple’s immutable ledger, financial institutions gain faster reconciliation, improved auditability, and better compliance reporting.

SWIFT and Ripple’s Dual-Rail System: ChatGPT Explores the Concept

Challenges Facing a SWIFT–Ripple Integration

Despite its strong potential, a number of obstacles must be addressed before such a model could scale globally:

Regulatory uncertainty surrounding the use of digital assets for settlements.

Liquidity management challenges and XRP volatility in large-value corridors.

Legal finality concerns and dispute resolution across multiple jurisdictions.

Cybersecurity and operational readiness for blockchain gateway infrastructure.

Sanctions and AML compliance requirements in decentralized environments.

Until clear frameworks and regulated liquidity providers are established, most banks are likely to proceed cautiously.

Step-by-Step Path to a Dual-Rail Future

A dual-rail system will not emerge overnight. A phased implementation is far more realistic:

Pilot programs: Begin with low-value remittance and SME payment corridors using hybrid settlement models.

Corporate treasury use cases: Explore after-hours or weekend liquidity transfers to test performance.

Institutional integration: Expand into major corridors once compliance and cost advantages are proven.

Standardization and governance: Develop shared rulebooks covering settlement finality, liability, and fallback procedures.

This measured approach lets banks experiment with Ripple’s settlement capabilities while keeping SWIFT’s compliance infrastructure intact.

What SWIFT–XRP Powered Dual-Rail System Could Mean for Banks, PSPs and Regulators

A SWIFT–XRP powered dual-rail system could mark a turning point for global finance, offering banks, payment service providers, and regulators a unified infrastructure that balances innovation with compliance.

For banks: Adopt blockchain-ready connectors and begin pilot projects under controlled regulatory environments to measure real-world performance.

For payment service providers (PSPs): Use real-time settlement options to offer faster and cheaper cross-border payment services, improving competitiveness and customer satisfaction.

For regulators: Establish clear and harmonized frameworks for digital asset settlements, liquidity management, and compliance data exchange.

For end users: Experience faster, more transparent, and lower-cost cross-border payments, often without realizing blockchain technology is behind it.

The Bottom Line: Collaboration, Not Competition

A SWIFT–Ripple dual-rail global settlement system is not about replacing the legacy infrastructure, it’s about modernizing it.

By combining SWIFT’s compliance network with Ripple’s blockchain efficiency, the global financial system could finally achieve real-time, interoperable, and inclusive payments at scale.

As ChatGPT puts it:

“Strategically sensible, tactically hard, but inevitable.” The future of global payments will not belong to a single network. It will belong to the systems that can connect them all.

The idea of a SWIFT–Ripple dual-rail system remains speculative, a forward-looking concept rather than an established roadmap. The analysis presented here reflects ChatGPT’s interpretation of current financial and technological trends, not a confirmed plan by SWIFT, Ripple, or any regulatory body.

While AI can help visualize potential outcomes, it operates on available data and modeled reasoning. These insights should be viewed as analytical forecasts, not certainties.

Artificial intelligence could, in theory, enhance such a system by automating compliance checks, predicting liquidity flows, and monitoring real-time risks across both rails. Yet the same technology introduces its own set of challenges.

AI models can misinterpret complex financial signals, reflect bias in training data, or produce inaccurate conclusions when faced with incomplete or outdated information. Over-reliance on automated systems could also reduce human oversight, raising systemic and ethical concerns.

SWIFT’s CIO on Ripple/XRP: Governance, Trust and the “Competitor’s Rails” Concern

In recent LinkedIn posts and comments, Tom Zschach has offered a blunt critique of the narrative around Ripple and XRP as a settlement rail for banks and payment networks.

These remarks are significant for anyone considering a joint or dual-rail model involving SWIFT and Ripple.

Zschach’s Key Messages

He has argued that “surviving lawsuits isn’t resilience,” emphasizing that what truly matters in global payments is neutral and shared governance of infrastructure, not simply regulatory victories or individual company survival.

Zschach has also questioned whether banks would ever feel comfortable relying on an external digital token such as XRP for settlement finality, pointing out that such assets are not deposits, not regulated money, and do not appear on a bank’s balance sheet.

He further stressed that financial institutions prefer neutral networks where no single participant or vendor controls the infrastructure. As he put it, “institutions don’t want to live on a competitor’s rails.”

While Zschach acknowledges the potential of tokenization and public blockchains to improve liquidity and efficiency, he remains cautious about adopting them as full replacement rails for cross-border settlement in the absence of stronger governance, compliance, and legal frameworks.

What Zschach’s Stance Means for a SWIFT–Ripple Dual-Rail Scenario

Zschach’s focus on governance and neutrality highlights one of the biggest challenges facing a potential dual-rail model. Even if Ripple’s technology proves technically sound, banks will ask who controls the rail, who governs the rules, and how settlement finality is enforced.

His comments suggest that SWIFT’s cooperative model, owned and governed by its member institutions, remains the standard for institutional trust. Any new settlement rail, including one powered by Ripple or XRP, would need to align with that structure to gain widespread adoption.

In his view, regulatory approval alone is not enough. Banks will also consider issues such as legal enforceability, accounting treatment, and balance-sheet risk. If a blockchain settlement rail introduces exposure to non-bank assets or privately controlled infrastructure, adoption is likely to remain limited.

For the dual-rail concept to succeed, the settlement layer must be perceived as neutral, interoperable, and collectively governed, rather than operated by a single corporate entity.

Caution! Please note that the above observations are based on Zschach’s public remarks and summaries of his commentary. They should not be interpreted as SWIFT’s official or final position on Ripple or XRP. Instead, they reflect a broader industry sentiment: while innovation is welcomed, trust, neutrality, and governance remain the deciding factors in how global payment systems evolve.

Conclusion

The concept of a SWIFT–Ripple dual-rail global settlement system represents more than a technological experiment, it’s a blueprint for the next evolution of cross-border finance.

If realized, it could seamlessly blend the trust, standardization, and governance of SWIFT with the speed, liquidity, and transparency of Ripple’s blockchain. Yet, this future will depend on collaboration: between fintech innovators and global banks, regulators and technology providers, AI systems and human decision-makers.

In the end, it’s not about replacing one rail with another, it’s about building a resilient, interoperable financial ecosystem that connects them all.

What is SWIFT, and what role does it play in global payments?

SWIFT (the Society for Worldwide Interbank Financial Telecommunication) is a cooperative network that enables secure financial messaging between more than 11,000 institutions in over 200 countries. It does not move money itself but provides the standardized communication system that banks use to exchange payment instructions and settlement details.

What is Ripple, and how does it differ from SWIFT?

Ripple is a technology company that offers blockchain-based payment solutions designed to enable real-time cross-border value transfers. Unlike SWIFT, Ripple’s network can facilitate both messaging and settlement, using digital assets like XRP or tokenized fiat to provide on-demand liquidity and faster transaction completion.

Has SWIFT officially partnered with Ripple or adopted XRP for settlements?

No. As of Oct. 21, 2025, SWIFT has not announced any official partnership with Ripple or the adoption of XRP for payment settlements. SWIFT continues to focus on its ISO 20022 migration, its gpi (Global Payments Innovation) initiative, and blockchain-based research projects under its own governance framework.

What is SWIFT’s current stance on blockchain and digital asset integration?

SWIFT has publicly acknowledged the potential of blockchain and tokenization technologies to improve settlement efficiency and transparency. The organization is running pilots and experiments connecting tokenized asset platforms to its network. However, SWIFT maintains that any future integration must meet strict governance, compliance, and interoperability standards before being considered for production use.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy