5 Key Partners Strengthening Ripple Treasury’s Ecosystem — Including SWIFT

Share

Key Takeaways

ISO 20022 applies to financial messaging, not tokens. The relevant question is whether the infrastructure around a blockchain supports ISO 20022-compatible data and workflows.

Supporting ISO 20022 means preserving full payment and identity metadata across messaging, execution, and settlement, not just settling value on-chain.

Banks will only use blockchain systems that align with regulatory controls, liquidity needs, governance standards, and operational reliability, not because a token appears on a “compliant coins” list.

Chainlink’s work with SWIFT and major financial institutions shows that the bridge between ISO 20022 systems and blockchain settlement is where practical adoption will occur.

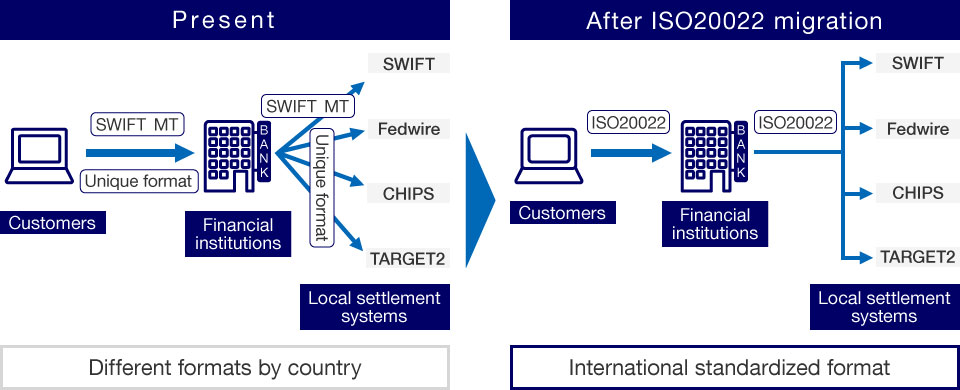

ISO 20022 is a global standard for financial messaging created by the International Organization for Standardization (ISO). It defines a universal language and data model for payments and other financial communications, replacing legacy formats (such as SWIFT’s MT messages) with rich, structured XML/JSON data.

MT stands for Message Type and refers to the legacy SWIFT financial messaging format used globally for decades in cross-border payments and interbank communication. MT messages rely on fixed text-based fields, which limit the amount of structured data they can carry. This makes tasks like compliance screening, reconciliation, and remittance clarification more difficult. Because of these limitations, MT formats are being phased out and replaced by the richer, structured ISO 20022 (MX) message standard.

Because ISO 20022 messages can include granular payment details, purpose codes, remittance data, and party identifiers, they enable greater transparency, stronger compliance screening, and more automation in processing.

In practical terms, migrating to ISO 20022 helps banks and payment systems achieve enhanced interoperability, richer data exchange, and higher efficiency in moving money across borders. The standard already live in many domestic payment systems across more than 70 countries and is becoming the de facto global standard for high-value and cross-border payments.

For crypto-aware readers, the crucial point is this: ISO 20022 is not a blockchain or a cryptocurrency. It is a messaging standard used by financial institutions to communicate payment instructions, securities trades, settlement information, and more.

As banks and market infrastructures upgrade to this common language, the question becomes how blockchains and digital assets can integrate with ISO 20022 rails and what it really means when a project claims to be “ISO 20022 compliant.”

SWIFT’s ISO 20022 Migration: Timeline And Global Impact

SWIFT, which connects 11,000+ institutions worldwide, is in the middle of a phased migration to ISO 20022 for cross-border payments and high-value transfers.

March 20, 2023: SWIFT began the “coexistence period” for cross-border payments. From this date, banks could send ISO 20022 (MX) messages while still supporting the legacy MT format. All SWIFT participants had to be able to receive ISO 20022 payment instructions (or a translated equivalent).

Late 2023: Major market infrastructures moved domestic high-value systems to ISO 20022. In Europe, for example, TARGET2 completed its migration so that domestic and cross-border flows increasingly carry the same rich data structure.

November 22, 2025: End of coexistence. SWIFT retires legacy MT for cross-border payments and requires ISO 20022 exclusively. After this date, institutions that haven’t fully migrated will rely on conversion utilities at best and face operational risk at worst. Functionally, the interbank world will speak one structured data language.

ISO 20022 migration for cross-border payments. | Source: mizuhogroup.com

Why does this matter?

ISO 20022 isn’t just a tech refresh, it rewires how value moves. Richer end-to-end data means fewer manual repairs, faster reconciliation, better sanctions screening and fraud controls, and fewer payment investigations.

For businesses and consumers, that translates into fewer delays, clearer remittance information, and smoother cross-border experiences. Strategically, a universal syntax paves the way for interoperability across countries and between traditional and emerging platforms.

“ISO 20022 Compliant” Vs. “ISO 20022 Compatible”: Clearing The Confusion

A common misconception is that there is a formal ISO 20022 certification for cryptocurrencies. There isn’t. ISO 20022 is a family of message standards and models, not a regulatory license. No committee “rubber-stamps” a coin as ISO 20022-compliant.

When people say a crypto project is “ISO 20022 compliant,” they typically mean one of two things:

Technical compatibility: The project’s infrastructure can support ISO 20022 messages. For example, by mapping a PACS.008 credit transfer or other MX message into on-chain operations without losing structured fields.

Standards participation: The organization behind the network participates in ISO 20022 governance (e.g., the Registration Management Group or maintenance bodies), aligning product design to the evolving standard.

4 different types of ISO 20022 adopters. | Source: corporates.db.com

Crucially, even if a project supports ISO 20022-style messaging, that does not guarantee bank adoption. Banks evaluate security, liquidity, governance, regulatory alignment, resilience, and business value. Compatibility removes friction; it doesn’t create demand on its own.

The idea is straightforward: a bank can originate an ISO 20022 payment instruction and have RippleNet handle orchestration and settlement (which can include the XRP Ledger) without abandoning the standard’s structured data.

Bank adoption is separate. ISO 20022 alignment makes integration easier, but institutions still decide if and when to use Ripple’s services or XRP for liquidity.

In practical terms, a bank could use RippleNet and XRP for cross-border settlement and not have to translate or deviate from the standard messaging formats it’s implementing for SWIFT. This compliance at the messaging layer means Ripple’s system can slot into banks’ workflows more easily than a system that speaks a completely different language.

However, it’s worth noting that while RippleNet can carry ISO 20022 messages, actual adoption depends on banks signing up for Ripple’s network. As of now, Ripple has some banking and fintech clients, but the global SWIFT network is also upgrading to ISO 20022, reducing one advantage Ripple used to highlight. In summary, Ripple (via RippleNet) truly supports ISO 20022 messaging – this is not just marketing; it’s confirmed by their membership in the standards body and technical integration.

Stellar (XLM) And ISO 20022

Stellar’s remit has always been low-cost, cross-border value movement. The Stellar Development Foundation has engaged with the ISO 20022 ecosystem, and independent engineering efforts have demonstrated direct mappings of ISO 20022 payment messages onto Stellar transactions while retaining KYC/AML-relevant metadata (e.g., using established Stellar protocols for identity and compliance).

This means a bank can take an ISO 20022 instruction and settle via Stellar (including with regulated stablecoins on Stellar) without losing structured fields along the way. Earlier enterprise initiatives (such as IBM’s World Wire) showcased how a Stellar-based rail could interface with bank systems designed around ISO 20022. As with XRP, the emphasis is on infrastructure compatibility, not a certification badge.

On a technical front, Stellar has seen concrete development to support ISO 20022 messaging. In March 2023, a U.S.-based blockchain consulting firm, BP Ventures (BPV), announced it had “completed development of support for ISO 20022 on the Stellar blockchain.” This implementation essentially mapped ISO 20022 payment messages onto Stellar transactions. According to BPV, this opens the possibility for “trillions of dollars” of financial transfers to migrate to Stellar, leveraging its 5-second settlements and low fees while handling all transaction metadata in the ISO 20022 format.

Hedera Hashgraph (HBAR) And ISO 20022

Hedera’s enterprise orientation makes it a frequent entrant in “ISO 20022” conversations. Technically, the Hedera Consensus Service can act as a high-throughput, tamper-evident log for standardized messages, including ISO 20022 payloads, while the Hedera Token Service handles asset operations.

In practice, institutions can anchor ISO messages on-chain for auditability or trigger token movements that correspond to those messages.

Hedera’s governance council, composed of global enterprises and financial firms, adds institutional credibility. Still, the accurate way of understanding is that Hedera is ISO 20022-ready or aligned, not officially certified. As with others, proof will come from sustained production usage by financial institutions.

Cardano (ADA) And ISO 20022

Cardano (ADA) is often listed alongside “ISO 20022 coins,” but most of that is community inference rather than formal alignment initiatives. Cardano has obtained an ISO-affiliated Digital Token Identifier (DTI), useful for market clarity but separate from ISO 20022 – it’s more like getting a catalog entry for the asset in a registry of tokens.

Cardano is often included in lists of “ISO 20022 compliant cryptos,” likely because it has a robust architecture and the Cardano Foundation has engaged with regulators and standards in various ways. However, there is no evidence that Cardano’s technology or governance has any direct role in the ISO 20022 standard or its working groups.

The fair characterization today is: Cardano could be made ISO 20022-compatible via APIs or middleware that map ISO messages into on-chain logic and back. That is technically feasible, but it is not the same as demonstrable production integrations with banks using ISO 20022 over Cardano.

Algorand (ALGO) And ISO 20022

Algorand’s performance and focus on regulated use cases (including pilots with public-sector entities) make it a sensible candidate for ISO 20022 compatibility. Its layer-1 features (smart contracts and native assets) are well-suited to implementing clean mappings between ISO messages and on-chain operations.

As of now, the most accurate framing is “ISO 20022-aware and technically compatible” rather than formally certified or widely deployed for ISO-native bank workflows. As with Cardano, watch for official announcements or production gateways that explicitly handle ISO 20022 payloads end-to-end.

Chainlink’s Role In ISO 20022 Integration With SWIFT And Banks

Oracle platforms like Chainlink support ISO 20022 messaging. | Source: @ChainLinkGod on X.

Here’s what stands out:

Cross-network tokenization pilots: SWIFT collaborated with Chainlink and a large cohort of financial market infrastructures and banks to show that a single SWIFT interface can instruct actions across multiple blockchains. Chainlink’s Cross-Chain Interoperability Protocol (CCIP) served as the secure interoperability layer, allowing ISO 20022 instructions carried over SWIFT to result in standardized on-chain operations. Participants spanned global custodians, CSDs, and tier-one banks, evidence that the approach is being tested by institutions who actually run capital markets plumbing.

Corporate actions standardization: In a separate industry initiative, market infrastructures and banks worked with Chainlink to normalize corporate actions data (e.g., dividends, splits) and express confirmed results as ISO 20022-compliant messages transmitted over SWIFT, while also recording attested data across multiple blockchains. The aim: reduce operational risk and cost in an area historically plagued by unstructured announcements and manual work.

Additionally, work on tokenized fund subscription/redemption demonstrated how institutions can use existing systems (and ISO 20022 messages over SWIFT) to interact with tokenized assets. A notable production example is a tokenized fund operated by a major global bank, where SWIFT messaging plus Chainlink’s interoperability layer streamline the workflow to an Ethereum-based instrument.

Finally, SWIFT’s Standards Release 2025 (SR 2025)securities updates reflect ongoing interoperability work: the message catalogue is being expanded to accommodate fields relevant to external price sources and blockchain transaction references. The direction of travel is clear, standards are evolving to recognize on-chain activities as first-class citizens in post-trade data flows.

How to Build ISO 20022-Ready Crypto Infrastructure

Before discussing specific projects and technical approaches, it is important to shift from coin-focused narratives to infrastructure thinking. ISO 20022 is fundamentally about data structure, interoperability, and message standardization, not about certifying digital assets.

For a blockchain network, wallet provider, custody platform, or oracle layer to operate in an ISO 20022 environment, it must handle structured financial messaging end-to-end, maintain data integrity, and interface cleanly with banking systems that are migrating toward ISO 20022 as their default communication standard.

That means success depends not on whether a token is labeled “ISO compliant,” but on whether the surrounding infrastructure actually supports accurate, lossless, auditable financial messaging flows.

Use the right vocabulary: Say “supports ISO 20022 messaging” or “ISO 20022-compatible interfaces,” not “ISO-certified coin.” There is no such badge for tokens.

Prioritize end-to-end data integrity: If you map ISO messages on-chain, preserve structured fields (parties, purpose, remittance data) and produce evidence trails for audits.

Meet banks where they are: SWIFT and market infrastructures are standardizing on ISO 20022. Provide APIs and connectors that accept/emit MX messages without lossy translations.

Target real use cases: Cross-border treasury, corporate actions, and tokenized funds have clear pain points solved by structured data plus on-chain finality.

Plan for 2025 and beyond: With legacy MT retired for cross-border payments after November 22, 2025, ISO 20022 fluency becomes table stakes for serious integrations.

Hype Vs. Reality In ISO 20022 Crypto Compliance

ISO 20022 is about data interoperability, a universal syntax that allows financial systems to speak clearly. Some networks (notably Ripple and Stellar) have aligned product design and standards participation around that reality.

Others (like Hedera, Cardano, and Algorand) are technically capable and positioning for compatibility, with varying degrees of enterprise traction.

Meanwhile, Chainlink has emerged as critical middleware, showing how ISO 20022 messages flowing over SWIFT can securely trigger on-chain actions and how standardized ISO messages can be produced from blockchain-anchored data.

Remember: compatibility is necessary but not sufficient for adoption. Banks choose solutions that are secure, compliant, resilient, liquid, and cost-effective.

Treat “ISO 20022-ready” as a starting point. The projects that convert compatibility into production-grade integrations, especially in areas like corporate actions, tokenized funds, and cross-border treasury, will be the ones that matter in the ISO 20022 era.

Can a cryptocurrency be officially certified as ISO 20022 compliant?

No. ISO 20022 is a messaging standard, not a regulatory approval system or certification program. There is no formal ISO 20022 badge for tokens. What can be ISO 20022–compatible is the infrastructure around a crypto network, its APIs, messaging gateways, and data models, not the coin itself.

Does supporting ISO 20022 mean banks will automatically adopt a blockchain?

No. Even if a blockchain network supports ISO 20022 messaging, bank adoption requires regulatory clarity, liquidity management, governance assurances, security audits, and business justification. ISO 20022 compatibility removes a technical barrier, but it does not guarantee usage.

Why does ISO 20022 matter for tokenization and on-chain settlement?

ISO 20022 enables structured, detailed transaction data to accompany asset movements. When tokenized securities, funds, or payments interact with banking systems, this structured data ensures clear audit trails, automated reconciliation, and compliance checks, making institutional settlement workflows more efficient.

How does Chainlink fit into ISO 20022 adoption?

Chainlink provides interoperability and message translation infrastructure that allows ISO 2002-compliant systems (like SWIFT) to trigger and verify on-chain transactions across multiple blockchains. Instead of a blockchain needing to be “ISO certified,” Chainlink bridges ISO 20022 messaging to blockchain execution, which is what institutions actually require.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy

-Light-Grey.jpg?language_id=1)