Key Takeaways

- ISO 20022 standardizes how financial data is exchanged; it does not certify cryptocurrencies.

- Ripple and Stellar are technically aligned with ISO 20022 but not officially certified.

- True value lies in compliance, interoperability, and real-world integration with financial systems.

- The migration rewards adoption and utility, not marketing claims or speculation.

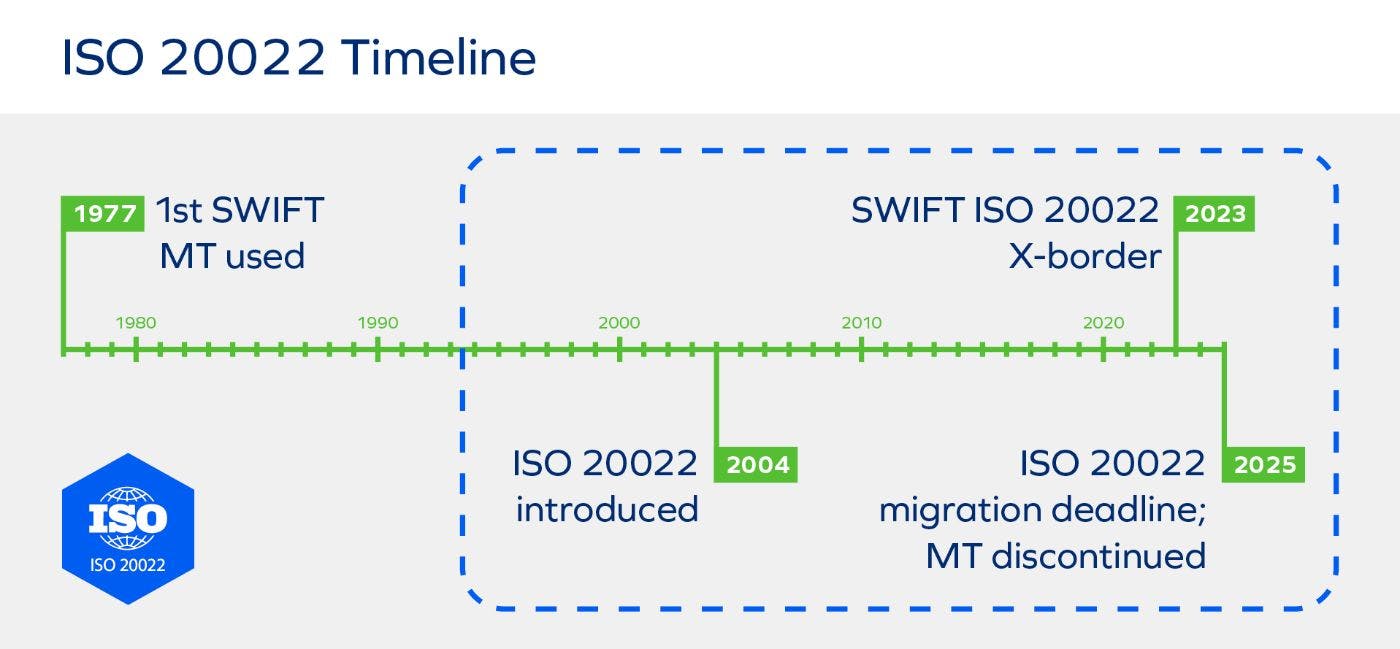

November 22, 2025 marks a milestone for international finance: the official cut-over to the ISO 20022 messaging standard.

From now on, all SWIFT FI-to-FI payment messages will be exchanged in the richer ISO 20022 format, ending the coexistence with legacy MT messages.

It’s more than a technical switch. ISO 20022 reshapes how money talks, delivering structured data, clearer compliance, and automation potential that could redefine cross-border payments.

Amid this transformation, two of the most frequently discussed are Ripple’s XRP Ledger (XRPL) and the Stellar Network (XLM).

Both are often mentioned in connection with ISO 20022, but who’s truly ready to thrive in this new era?

What ISO 20022 Really Is (and Isn’t)

ISO 20022 is a global standard that governs the format and content of financial-message traffic. It replaces older MT formats, which were text-based and often unstructured, with XML or JSON formats that carry richer metadata such as party identifiers, remittance data, purpose codes, and structured addresses.

The benefits for banks and payment systems include:

- More detailed and consistent data for automation and analytics

- Enhanced compliance and transparency in AML and KYC processes

- Easier interoperability across different financial systems and geographies

Crucially, ISO 20022 is not a certification for cryptocurrencies or blockchains. It defines the messaging structure between institutions, not the underlying assets or settlement rails. With the coexistence period now ending, institutions that fail to migrate risk rejected messages, data loss, or costly translation processes.

Before ISO 20022

For decades, banks worldwide have used MT messages under the old SWIFT standard. These were mostly plain-text messages, like short notes between banks.

Imagine you’re sending money overseas and the message says something like:

“Send $1,000 to Account 12345, Reference: Invoice 56.”

That’s all — short, simple, and limited.

The problem? There’s no consistent structure, and every bank might format it differently. Important details (such as who’s paying, why, or what the funds are for) may be buried in free text. This makes automation hard and compliance checks (like anti-money laundering or sanctions screening) slow and error-prone.

After ISO 20022

Now, ISO 20022 messages use structured, data-rich formats — built in XML or JSON, similar to what modern software uses.

Instead of a short text note, each message carries well-labelled data fields, such as:

- Sender and receiver names and IDs

- Purpose of payment (salary, invoice, tax, refund, etc.)

- Address and account details in standard formats

- Currency, timestamps, and transaction references

Think of it like the difference between a handwritten note and a spreadsheet:

- The note just tells you something happened.

- The spreadsheet captures exactly what, when, where, why, and by whom.

With ISO 20022, computers, not just humans, can read and understand every part of a payment message automatically. That means faster processing, fewer errors, better fraud detection, and more transparency for regulators and customers alike.

Ripple’s XRP Ledger (XRPL) — Institutional Integration and ISO Alignment

Ripple positioned itself early within the ISO 20022 landscape. The company joined the ISO 20022 Registration Management Group in 2020, becoming one of the first distributed-ledger-technology participants to do so.

RippleNet, Ripple’s enterprise payments network, is built to send and receive ISO 20022-formatted messages, allowing banks to maintain structured data as payments move across borders.

In practical terms, this means that banks can communicate directly through RippleNet without converting message formats. Combined with Ripple’s On-Demand Liquidity (ODL) solution, which uses XRP as a bridge asset for settlement, the infrastructure is technically well aligned with ISO 20022’s principles.

On X, SMQKE states that “the ISO 20022 site is showing an approved request to enable Interledger Protocol (ILP)” by Ripple in the context of the SWIFT/ISO 20022 framework.

However, the XRP token itself is not “ISO-certified.” The standard governs messaging, not digital assets. The real advantage lies in Ripple’s infrastructure and partnerships, not in any formal compliance label. Institutional adoption will still depend on regulatory clarity, liquidity, and the extent to which banks choose to use ODL for actual value transfer.

Stellar Network / XLM — Low-Cost Rails and Financial Inclusion

Stellar takes a complementary path. Its network is optimized for speed and affordability, typically settling transactions within seconds and at a fraction of a cent in fees. The Stellar Development Foundation has explored how ISO 20022-style messages can be mapped to Stellar transactions, allowing institutions to interface with its network while preserving structured metadata.

Stellar’s mission has long focused on financial inclusion and accessibility, connecting fintechs, remittance providers, and humanitarian organizations. These corridors differ from Ripple’s bank-centric focus, yet they also stand to benefit from ISO 20022’s structured data, which improves traceability and compliance even in low-value transfers.

While Stellar is not a formal member of ISO’s governance structures, its architecture supports compatibility with the standard’s message structures. The main constraint lies in scale: fewer major banking relationships are publicly disclosed compared with Ripple’s ecosystem, and broader adoption may take longer to materialize.

Overall, Stellar and XLM are well positioned for smaller, faster, and lower-cost transactions that align with ISO 20022’s goal of interoperability, even if their institutional footprint is currently more modest.

| Features |

Ripple / XRPL |

Stellar / XLM |

| ISO 20022 messaging support |

Full support through RippleNet |

ISO-style mapping demonstrated |

| Institutional focus |

Banks, payment providers, corporates |

Fintechs, remittances, NGOs |

| Settlement asset |

XRP used for On-Demand Liquidity |

XLM used for network liquidity |

| Transaction speed and cost |

3–5 seconds, low fee |

2–5 seconds, ultra-low fee |

| Adoption and scale |

Broader institutional footprint |

Smaller scale, high accessibility |

Ripple’s XRP Ledger leads in institutional integration and messaging alignment, while Stellar excels in agility, affordability, and inclusion. Each serves a different segment of the payments landscape but both reflect ISO 20022’s core philosophy of better data and frictionless movement of value.

SWIFT’s Linea Initiative: Bridging ISO 20022 and Blockchain Networks

As global finance completes its transition to ISO 20022, SWIFT continues to explore how standardized messaging can coexist with digital-asset ecosystems. Its Linea initiative, developed in collaboration with ConsenSys and a consortium of major financial institutions, represents an early step toward integrating ISO-formatted data with blockchain-based networks.

Linea operates as a shared ledger experiment, designed to test how traditional payment and settlement messages could move securely across distributed-ledger environments while maintaining regulatory and operational integrity. The goal is not to replace existing SWIFT rails but to extend their reach into tokenized assets, digital currencies, and blockchain-native transactions.

The initiative reflects its role as a neutral connector, linking public and private blockchains with the same reliability that underpins global interbank messaging. This effort reinforces a key message from SWIFT’s Chief Innovation Officer, Tom Zschach:

“This isn’t about replacing existing payment systems or issuing new money. Settlement remains in central-bank money, commercial bank money or tokenized deposits. What changes is the ability to lock in commitments, execute complex cross-border transactions atomically, and share a single auditable record across networks.”

By embedding ISO 20022 principles into the architecture of blockchain interoperability, SWIFT’s Linea could mark the next phase in unifying traditional finance and digital-asset infrastructure, showing that standardization, not speculation, remains the true bridge between both worlds.

Crypto Compliance and the ISO 20022 Era

One of the most significant implications of ISO 20022 for digital assets is data transparency. The standard introduces a uniform structure for identifying counterparties, transaction purposes, and regulatory classifications, precisely the areas where crypto transactions have historically been scrutinized.

For crypto compliance officers and CFOs, ISO 20022 presents both relief and responsibility:

- Relief because it enables cleaner integration between digital-asset systems and traditional banking compliance checks.

- Responsibility because richer message fields mean every payment carries explicit identifiers, making it harder to obscure origins, destinations, or intent.

Financial officers managing crypto operations must now ensure their messaging and transaction systems can capture, store, and transmit ISO 20022 data fields in ways that align with institutional AML and audit expectations.

Many CFOs in crypto-native firms are preparing for a dual challenge:

- Bridging structured ISO 20022 data into decentralized transaction systems without losing traceability.

- Proving audit readiness as regulators begin expecting the same level of reporting from digital-asset institutions as from traditional banks.

In practice, that means upgrading treasury systems, transaction monitoring tools, and blockchain analytics to handle ISO-level data granularity. For Ripple and Stellar, which already promote interoperability and structured payment flows, this creates a strong narrative for compliance alignment.

CoinMarketCap’s ISO 20022 Coin Category: A Reflection of Market Interest, Not Certification

In late 2025, CoinMarketCap introduced a new category titled “ISO 20022 Coins,” featuring a collection of digital assets such as XRP, Stellar (XLM), Algorand (ALGO), Quant (QNT), IOTA, XDC Network (XDC), and Hedera (HBAR). The list quickly drew attention from investors and enthusiasts alike, reflecting a growing curiosity about blockchain projects positioned for financial-system interoperability.

However, it’s important to note that ISO 20022 does not certify cryptocurrencies. The standard defines how financial data is structured and transmitted, not which assets meet its criteria.

In that sense, CoinMarketCap’s list serves as a market reference rather than a regulatory statement. It helps investors track projects exploring compatibility with global payment messaging formats, but does not imply any formal approval from ISO or SWIFT.

The category underscores a larger trend: the digital-asset sector’s effort to align itself with the infrastructure and data standards of traditional finance, even as definitions of “compliance” remain fluid.

What to Watch Next

Going forward, you should keep an eye on:

- Institutional integration: Whether banks formally announce partnerships or live corridors using RippleNet, Stellar, or similar DLT rails.

- Transaction volume and liquidity: Changes in on-chain activity, cross-border settlement volume, and liquidity depth on XRPL and Stellar.

- Regulatory environment: Ongoing clarity for XRP and XLM in key jurisdictions will strongly influence institutional willingness to engage.

- Competition: Other blockchain networks, such as those using Algorand or Hedera, are also positioning themselves for ISO 20022 interoperability.

- Bank operations: Observing how banks adjust to richer message data and whether they leverage DLT for real-time settlement or remain on upgraded legacy systems.

The Road Ahead: Data, Trust and Interoperability

As ISO 20022 becomes the backbone of global payments, its impact on digital assets will extend far beyond messaging alignment. The standard’s true promise lies in creating a shared financial language – one that unites banks, fintechs, and blockchain networks through structured, transparent data.

Projects like Ripple and Stellar exemplify this shift, each bridging different parts of the financial ecosystem. Yet, as the CoinMarketCap category shows, technical alignment should not be mistaken for certification. The next phase of progress will be measured not by labels, but by how effectively blockchain infrastructure integrates with regulated financial systems.

At the same time, SWIFT’s Linea initiative signals that traditional finance is also evolving, exploring blockchain connectivity while maintaining its core principles of governance, compliance, and trust. The convergence of these efforts suggests a future where value moves as seamlessly as information, such as securely, transparently, and across networks.

In the end, ISO 20022 isn’t about hype or hashtags, it’s about building a more connected, data-driven financial world. The winners in this new era will be those who turn compatibility into capability, and alignment into adoption.

FAQs

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy