SWIFT's Blockchain Ledger Goes Live With HSBC, Citi and 15 Other Banks: Threat to XRP, XLM Cross-Border Plays?

Share

Key Takeaways

SWIFT’s blockchain ledger enables 24/7 tokenized payments without requiring XRP.

XRP supporters see an opportunity, as several SWIFT pilot banks have ties to Ripple.

Real XRP demand depends on banks choosing Ripple’s ODL rails for settlement.

SWIFT announced on July 9 that its blockchain-based shared ledger is ready for initial use, with 17 banks across six continents, including HSBC, Citi, UBS, BNY, Wells Fargo, Standard Chartered, and BNP Paribas, preparing to pilot 24/7 tokenized cross-border payments.

SWIFT Chief Business Officer Thierry Chilosi called it a step that extends the trust and stability of established finance into the frontiers of digital money.

Implemented in 9 months. Global from day one.

Swift's blockchain-based ledger is ready for use, with ANZ, BNP Paribas, BNY, Citi, DBS Bank, First Abu Dhabi Bank (FAB), FirstRand, HSBC, Itaú Unibanco, Lloyds Banking Group, Mashreq, MUFG, OCBC, Standard Chartered, UBS, UOB and… pic.twitter.com/kOg9DumptG

The system was designed and built in nine months, following feedback from international financial institutions, and enables banks to move tokenized deposits overnight and on weekends before completing final settlement through existing infrastructure.

The launch reopened a years-long argument about what this means for XRP, and the data support both sides more than either camp’s slogans suggest.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

TipRanks called the launch bluntly XRP’s worst nightmare, arguing that if legacy banks can now handle 24/7 global transfers on infrastructure they already own and control, fewer banks have a reason to route liquidity through Ripple’s On-Demand Liquidity product, directly undercutting the token’s core utility case.

SWIFT already reports that 75% of payments on its existing network reach beneficiary banks within 10 minutes, often in seconds, meaning the speed gap XRP has historically marketed itself against is narrower than the community narrative assumes, and SWIFT’s own scale dwarfs Ripple’s: SWIFT-associated payment instructions cover roughly $150 trillion in annual transaction value against Ripple’s cumulative institutional payment volume of just over $95 billion, with monthly ODL flows exceeding $15 billion, a fraction of a single day’s global cross-border volume.

Could XRP Still Power Liquidity Behind SWIFT’s Tokenized Future?

The bullish counter rests on the overlap between the ledger’s bank list and Ripple’s existing network. At least 30 of the more than 50 banks in SWIFT’s broader payments framework already have ties to Ripple’s ecosystem, and roughly 40% of those Ripple-connected banks use On-Demand Liquidity, the product that actually requires XRP as a bridge asset.

Versan Aljarrah, founder of BlackSwanCapitalist.io, argued on X that XRP isn’t replacing SWIFT so much as becoming the liquidity bridge inside it, pointing to the same bank overlap.

SWIFT just named 30+ @Ripple connected banks in its new 2026 payments framework.

HSBC, Deutsche Bank, Santander, Standard Chartered, JPMorgan… the list goes on.

— Versan | Black Swan Capitalist (@VersanAljarrah) July 9, 2026

Ripple has separately built distribution well beyond the token itself, holding more than 75 regulatory licenses, counting over 300 financial institutions on its network, and gaining NSCC clearing access through Ripple Prime, which is part of DTCC’s Tokenized Securities working group launching its pilot this month.

SWIFT’s own routing chain via payments firm Thunes gives banks optional access to Ripple’s ODL rails, meaning a payment can flow through SWIFT’s messaging layer and still settle using XRP as a bridge, without any bank being forced into that choice.

We’ve secured our preliminary Electronic Money Institution license approval from Luxembourg’s Commission de Surveillance du Secteur Financier (CSSF). 🇪🇺

This is a pivotal step toward scaling Ripple Payments across the EU, bringing institutional-grade digital asset infrastructure… pic.twitter.com/GW3c9gVhDs

In addition, Ripple received full Crypto Asset Service Provider (CASP) authorization from Luxembourg’s CSSF on July 6, 2026, completing its MiCA compliance alongside its existing EU Electronic Money Institution license. This followed a preliminary “Green Light Letter” on June 23. The license, combined with EEA passporting, lets Ripple offer regulated payments, custody, exchange and transfer services across all 30 EEA countries from a single authorization.

XRP Technical Signals Flash Caution After SWIFT Ledger Announcement

XRP traded near $1.10 following the announcement, posting modest gains as traders reacted to the bank list. But institutional positioning moved in the opposite direction: spot XRP ETFs recorded $7.29 million in net outflows on July 8, the largest single-day withdrawal since March, even as the price ticked higher.

Technically, XRP faces resistance near $1.114 and $1.127, the 61.8% and 50% Fibonacci retracement levels. While MACD remains above its signal line, the histogram has started to fade, suggesting momentum is slowing rather than building.

SWIFT vs XRP Debate Depends on Adoption, Not Bank Partnerships

Neither side has definitive proof yet, and the honest framing is optionality, not obligation. SWIFT’s ledger is deliberately neutral and deposit-based, built to move value without touching any external chain, while Ripple’s rails remain reachable but not required inside it.

The real test arrives when SWIFT’s first retail corridors go live in mid-2026: if banks in high-cost remittance markets choose to route through Thunes into Ripple’s ODL infrastructure because it’s genuinely faster or cheaper than SWIFT’s own new ledger, that is when real XRP demand would show up in onchain volume rather than in social media discourse.

Until then, both the threat case and the opportunity case are reading the same bank list and drawing opposite conclusions from it.

XLM Faces the Same SWIFT Question as XRP: Adoption vs Token Demand

Stellar faces a version of the same argument, with a different data profile. SWIFT’s new ledger is not built on Stellar’s network any more than it’s built on the XRP Ledger, so the direct threat logic applies equally: a bank-owned, deposit-based settlement layer competing on the same “always-on, low-cost” pitch Stellar has used for a decade.

SWIFT itself has grouped the two together in its broader framing, with earlier SWIFT-linked commentary explicitly naming both Ripple and Stellar as blockchain-native networks that its new infrastructure could directly compete with.

But Stellar’s institutional trajectory looks different from XRP’s in ways this ledger doesn’t touch. The Depository Trust and Clearing Corporation, which oversees $114 trillion in US capital market assets, chose Stellar as the first public blockchain to host tokenization of DTC-custodied assets, with availability targeted for the first half of 2027, and that announcement alone sent XLM up 28% in a single trading day against a broadly falling crypto market.

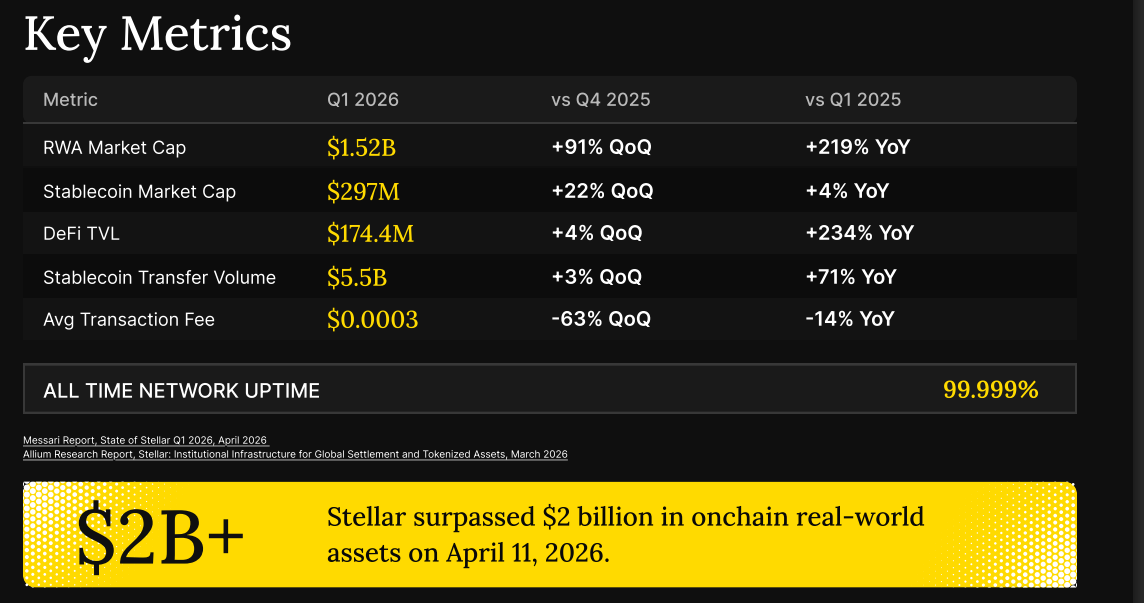

Stellar processed $5.5 billion in payment volume in Q1 2026, marking a 71% year-over-year increase as tokenized assets and multi-currency stablecoin activity shifted from issuance to real-world use.

Stablecoin transfer volume also grew 3% quarter-over-quarter, while the network maintained an average transaction fee of just $0.0003 and 99.999% uptime.

Stellar Network’s Q1 2026 by the numbers. | Source: Stellar

The Stellar Development Foundation said the growth was driven by the convergence of tokenized assets, stablecoins, FX rails, and payment access points, with assets increasingly moving across wallets, DeFi platforms, and global payment corridors.

PayPal’s PYUSD stablecoin and a substantial portion of Franklin Templeton’s government money fund already settled on Stellar’s rails, and CME Group listed regulated XLM futures in February 2026.

PYUSD on Stellar helps businesses by delivering near-immediate settlement and reducing friction in everyday transactions. | Source: Stellar.org

The structural weakness is the same one XRP has: usage and token demand remain disconnected. XLM exists as a bridge asset and anti-spam mechanism on Stellar’s network, meaning banks and institutions can transact on Stellar’s infrastructure without materially increasing demand for the token itself, the same gap that limits XRP’s price sensitivity to Ripple’s own growth.

XLM has also historically struggled to convert network usage into sustained price movement, trading well below its highs even as institutional integrations accumulated through 2025 and 2026.

For both assets, SWIFT’s ledger launch reinforces the same unresolved question rather than answering it: whether deep institutional plumbing eventually forces real token demand, or whether banks simply route value through public chains without ever needing to hold the coin that secures them.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.