Why SWIFT's Blockchain Push Is a Win for Ripple but Not Yet for XRP

Share

Key Takeaways

Over 50 banks are adopting a new framework designed to make cross-border retail payments faster, more transparent, and predictable.

The initiative promises upfront fee transparency, full-value delivery, faster settlement, and end-to-end tracking.

Up to 80% of payment delays occur after funds reach the destination bank, something SWIFT aims to fix with this new framework.

As SWIFT improves speed, cost transparency, and introduces blockchain features, the core value proposition of crypto payment networks is being challenged.

The global payments landscape is undergoing a profound transformation. For decades, the SWIFT network has served as the backbone of international banking, connecting over 11,500 financial institutions across more than 200 countries. Now, in a significant evolution of its infrastructure, SWIFT is rolling out a new cross-border payments framework supported by more than 50 banks, while simultaneously exploring blockchain-based settlement rails.

This dual-track strategy is not only aimed at modernizing international payments but also places SWIFT in direct competition with blockchain-native networks such as Ripple (XRP) and Stellar (XLM), which have long positioned themselves as faster, cheaper alternatives to traditional banking rails.

Cross-Border Payments Future: SWIFT’s New Retail Payments Framework

SWIFT’s latest initiative focuses on improving cross-border retail payments, transactions typically used by individuals and small businesses for remittances, e-commerce, and international transfers. These payments have historically been plagued by inefficiencies, including unclear fees, long settlement times, and limited transparency.

SWIFT’s latest initiative focuses on improving cross-border retail payments. | Credit: Real World Asset Watchlist X profile

The new framework seeks to address these issues head-on by offering:

Upfront cost certainty: Senders know exactly how much will be deducted before initiating a transfer.

Full-value delivery: Beneficiaries receive the exact amount sent, without intermediary deductions.

Faster processing speeds: Including instant settlement where possible.

End-to-end traceability: Full visibility throughout the transaction lifecycle.

More than 25 banks are expected to go live with the system by June 2026, covering key payment corridors such as Australia-Bangladesh, India-Pakistan, and UK-U.S. These routes are particularly significant, as they include some of the largest remittance markets globally.

Countries like India, China, Bangladesh, and Pakistan rank among the top recipients of remittances worldwide, making them critical testing grounds for any new cross-border payments infrastructure.

Solving the “Last Mile” Problem in International Money Transfers

Despite major improvements in recent years, such as 75% of SWIFT transactions reaching destination banks within 10 minutes, significant inefficiencies remain. According to SWIFT, up to 80% of a transaction’s total processing time occurs after it reaches the destination bank, during the so-called “last mile.”

SWIFT’s new framework is specifically designed to address this bottleneck by standardizing processes and improving coordination between banks at the domestic level.

By doing so, SWIFT aims to ensure that the speed gains achieved within its own network are not lost once funds exit the system.

ISO 20022 Explained: The Standard Powering Faster Global Payments

A key enabler of this transformation is SWIFT’s adoption of the ISO 20022 messaging standard, which allows for richer, more structured payment data.

This standard improves:

Interoperability between financial institutions.

Compliance and regulatory reporting.

Automation of payment processing.

In contrast to legacy formats, ISO 20022 enables more detailed information to travel alongside each transaction, reducing errors and increasing transparency.

While blockchain networks like Ripple and Stellar have emphasized speed and cost efficiency, SWIFT’s approach leverages standardization and global coordination, areas where it already has a significant advantage.

Perhaps the most notable aspect of SWIFT’s strategy is its move toward blockchain technology. While its new retail payments framework operates within the traditional banking system, SWIFT is also developing a blockchain-based shared ledger to support:

On-chain settlement of regulated financial instruments

SWIFT upgrades cross-border payments. | Credit: SWIFT X profile

This blockchain layer is not intended to replace SWIFT’s existing infrastructure but to complement it. By integrating distributed ledger technology (DLT) into its network, SWIFT aims to enable the seamless movement of tokenized value across its global ecosystem.

Importantly, SWIFT’s approach emphasizes regulated, institutionally compliant blockchain usage, distinguishing it from many public crypto networks.

50+ Global Banks Join SWIFT’s Next-Gen Payments Network

The scale of adoption is one of the most compelling aspects of SWIFT’s rollout. More than 50 major banks have signed on to support the new framework, including:

Global giants: JPMorgan Chase, Bank of America, HSBC, Citi

European leaders: Deutsche Bank, BNP Paribas, Santander, UBS

This broad participation underscores the industry’s confidence in SWIFT’s ability to modernize cross-border payments without abandoning the existing financial system.

It also highlights a key difference between SWIFT and blockchain-native competitors: network effects. SWIFT already connects the vast majority of the global banking system, giving it a powerful distribution advantage.

SWIFT vs Ripple (XRP) and Stellar (XLM): Who Wins the Payments Race?

For years, Ripple and Stellar have marketed themselves as solutions to the inefficiencies of cross-border payments. Their core value proposition centers on:

Near-instant settlement

Lower transaction costs

Reduced reliance on correspondent banking

Ripple’s XRP, for example, is designed to act as a bridge currency, enabling liquidity between different fiat currencies. Stellar’s XLM focuses on financial inclusion and low-cost remittances.

However, SWIFT’s latest developments challenge this narrative in several ways.

1. Speed and Efficiency Are No Longer Unique

With most SWIFT transactions already settling within minutes, and new initiatives pushing toward instant settlement, the speed advantage of XRP and XLM is diminishing.

2. Cost Transparency Is Improving

By introducing upfront fee certainty and full-value delivery, SWIFT is addressing one of the most common criticisms of traditional banking transfers.

3. Trust and Regulation Matter

While blockchain networks offer decentralization, many financial institutions prioritize:

Regulatory compliance

Security and resilience

Established governance frameworks

SWIFT’s infrastructure is deeply embedded within the global financial system, making it a trusted intermediary for banks and regulators alike.

If SWIFT can offer blockchain-based settlement within a regulated, bank-friendly environment, the need for separate networks like Ripple or Stellar may be reduced, at least for institutional use cases.

How SWIFT Aligns With the G20 Cross-Border Payments Roadmap

SWIFT’s initiative is closely aligned with the G20’s roadmap for improving cross-border payments by 2027. The G20 has identified key targets across:

Speed

Cost

Transparency

Access

By addressing these areas, SWIFT is positioning itself as a central player in the global effort to modernize financial infrastructure.

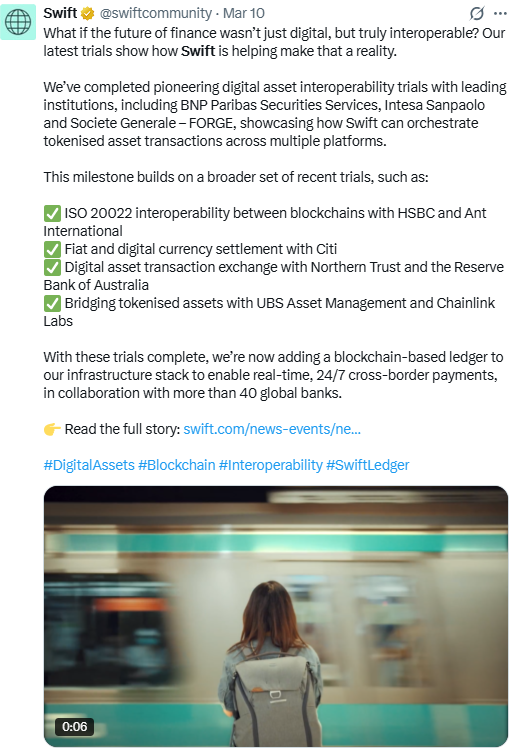

SWIFT completed digital asset interoperability trials with leading institutions. | Credit: SWIFT X profile

Nasir Ahmed, Head of Payments Scheme at SWIFT, emphasized this vision: “Everyone should be able to transact internationally at pace, safe in the knowledge that the full value will arrive with the recipient and that the fees will be affordable and fixed from the start.”

This focus on inclusivity and efficiency reflects broader industry trends toward financial accessibility and digital transformation.

Rise of Hybrid Finance: Where Traditional Banking Meets Blockchain

SWIFT’s expansion into faster payments and blockchain represents a pivotal moment for the financial industry. Rather than being disrupted by crypto, SWIFT is adapting, integrating new technologies while leveraging its existing strengths.

Several key implications emerge:

1. Hybrid Financial Systems Will Dominate

The future of payments is likely to be a hybrid model, combining:

What SWIFT’s Blockchain Expansion Means for the Future of Global Payments

SWIFT’s latest initiative marks a significant step forward in the evolution of global payments. By combining a new retail payments framework with blockchain-based innovation, SWIFT is addressing long-standing inefficiencies while positioning itself for the future of digital finance.

With over 50 banks onboard and real-world deployment already underway, this is not a theoretical upgrade: it is a live transformation of the global financial system.

At the same time, it raises important questions about the role of blockchain-native networks. As SWIFT adopts many of the features that once defined crypto-based payment solutions, the competitive landscape is shifting.

Ultimately, the race to redefine cross-border payments is no longer a battle between traditional finance and blockchain. It is a convergence, one in which the most successful players will be those that can seamlessly integrate both worlds.

What is SWIFT’s new cross-border payments framework?

SWIFT’s new framework is a global payments scheme designed to make international transfers faster, more transparent, and predictable. It offers upfront cost certainty, full-value delivery, near-instant processing speeds, and end-to-end traceability for retail cross-border payments.

How many banks are participating in SWIFT’s new payments initiative?

More than 50 banks worldwide have signed up to support the framework, with over 25 banks expected to go live by June 2026. Participants include major institutions like JPMorgan, HSBC, Deutsche Bank, and Bank of America.

Which countries and payment corridors are included in the rollout?

The initial rollout includes key remittance corridors such as Australia-Bangladesh, India-Pakistan, and UK-U.S. It also spans major markets like China, Germany, Spain, Thailand, and Canada.

How fast are SWIFT cross-border payments now?

Currently, around 75% of SWIFT transactions reach the destination bank within 10 minutes. The new framework aims to further improve this by enabling instant settlement where possible and reducing delays in the final processing stage.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy