Project Pangea Targets $150B Trade Corridor: Can Chainlink Challenge XRP and XLM in Cross-Border Payments?

Share

Key Takeaways

Chainlink joined 47 banks to build near-instant Europe–South Korea FX settlement infrastructure.

Project Pangea uses regulated stablecoins instead of XRP-like bridge assets for cross-border payments.

Despite growing institutional adoption, LINK’s price has yet to reflect Chainlink’s expanding network.

Chainlink has joined a coalition of 47 European and South Korean banks to build near-instant foreign exchange settlement infrastructure across one of the world’s largest trade corridors, a move that places the oracle network in direct competition with the institutional cross-border payment use cases that Ripple and Stellar have spent a decade building.

Project Pangea connects Chainlink with two banking groups: Qivalis, a euro stablecoin consortium made up of 37 European banks, and UniKA, a South Korean banking alliance representing more than 10 commercial banks.

Together they represent over $10 trillion in combined assets under management.

NEW: Chainlink & multinational banking consortia launch Project Pangea to develop a novel solution redefining international FX markets.

Pangea brings together 50+ banks, representing $10+ trillion AUM, to unlock T+0 cross-border settlement via Chainlink & ISO 20022 standards 🧵 pic.twitter.com/hcEjxKthd6

Project Pangea aims to cut the standard 48-hour foreign exchange settlement window to near-instant settlement, or T+0, using regulated stablecoins tied to the euro and the South Korean won. Both sides of a currency trade would clear at the exact same time through atomic payment-versus-payment settlement, meaning if one side fails, neither side goes through.

Project Pangea is designed as middleware that lets banks use existing Swift and ISO 20022 systems while settling on the Pangea L1 blockchain network. European banks continue initiating transactions through SWIFT, which the industry has used since the 1970s, with Chainlink’s infrastructure translating those commands into atomic swaps onchain.

Chainlink’s vice president for Asia-Pacific and the Middle East, Niki Ariyasinghe, said the consortium is targeting live transactions within 12 months.

Why This Corridor Matters

Europe and South Korea process over $150 billion in goods and services annually through their bilateral trade relationship, ranking the corridor among the world’s 15 largest trade routes.

Industry data shows 60% of all global stablecoin payments are happening in Asia, making the region a natural proving ground for regulated digital currency infrastructure.

Today’s T+2 settlement cycle creates counterparty risk, ties up capital, and introduces the possibility that one side of a trade defaults before settlement completes, a risk historically known as Herstatt risk after the 1974 German bank failure that exposed bilateral FX settlement gaps.

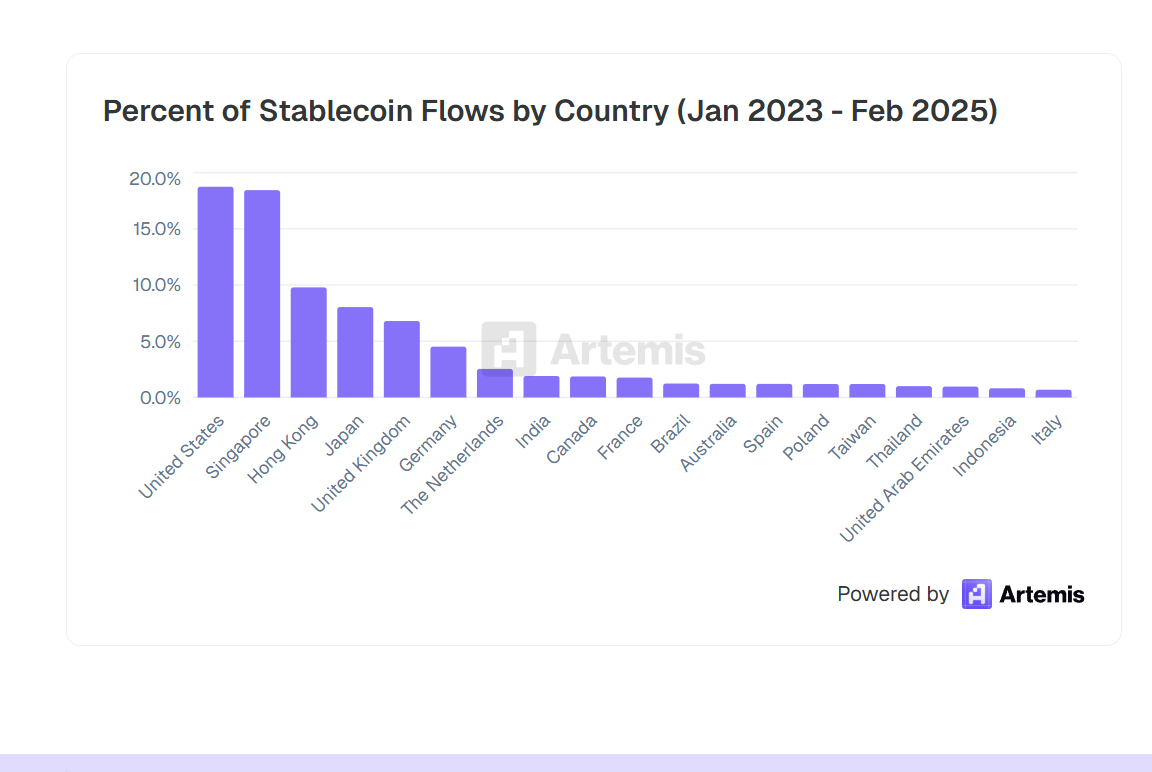

Moreover, according to Artemis, B2B stablecoin volume grew from under $100 million monthly to over $6 billion in roughly two and a half years, with Tron and Ethereum handling average transaction sizes above $219,000.

Project Pangea’s EUR-KRW corridor targets high-value institutional foreign exchange settlement rather than retail remittances, using atomic payment-versus-payment (PvP) settlement to eliminate settlement risk. The approach builds on concepts validated by the Bank for International Settlements through its Project Meridian FX research.

Stellar’s network similarly offers low-cost cross-border settlement through XLM and through assets issued by regulated anchors.

Ariyasinghe said Chainlink does not view Project Pangea as a rival to Ripple.

“We’re very much a technology provider. It’s less about creating a unified network from scratch. It’s about applying the technology, finding where that value is, and growing the network organically,” he said.

That distinction is meaningful in practice. Ripple’s ODL uses XRP as a liquidity intermediary, requiring counterparties to hold or transact in the token.

Project Pangea uses regulated fiat-pegged stablecoins, meaning banks settle in digital versions of currencies they already hold without needing exposure to a third-party crypto asset. For compliance-conscious institutions operating under MiCA and Korean digital asset frameworks, that difference carries weight.

LINK Price Has Not Moved

Despite partnerships with the DTCC, Robinhood, Amundi, Spiko, SWIFT, and now 47 banks through Project Pangea, LINK has fallen to around $7.5, trading more than 85% below its May 2021 all-time high of $52.70.

Chainlink has now facilitated more than $31 trillion in transaction value across its network, while institutional adoption continues to accelerate through initiatives such as Project Pangea and tokenized asset infrastructure.

The market’s key question is whether these real-world integrations will eventually translate into sustained demand for LINK, or whether institutional usage will continue to outpace token price performance.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.