Bitcoin’s price can fall even without heavy spot selling. Learn how derivatives, leverage, and liquidations now drive BTC price discovery. | Credit: CCN.com

Share

Key Takeaways

Holding large amounts of Bitcoin doesn’t automatically mean controlling price or supply.

ETFs change how Bitcoin trades, not whether it can be sold.

When high-conviction holders begin distributing, even tight supply can give way fast.

The real question isn’t who owns Bitcoin, but what prevents them from selling, and for how long.

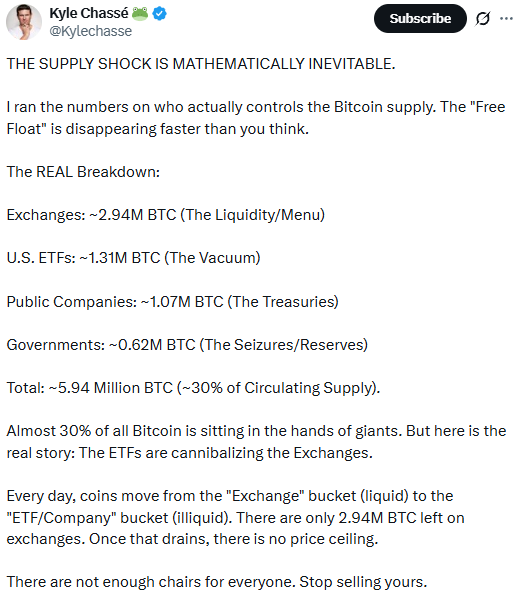

“The supply shock is mathematically inevitable.”

It’s a powerful line, used by crypto experts like Kyle Chassé, and it captures something real about Bitcoin’s structure. But the viral version of this argument often skips the most important nuance: control isn’t the same as custody. And liquidity isn’t the same as supply.

The popular framing breaks Bitcoin ownership into four buckets: exchanges, ETFs, public companies, and governments. And concludes that coins are steadily moving from “liquid” venues into “sticky” hands, setting the stage for an unstoppable price squeeze.

That story is directionally interesting, but incomplete. The more profound truth is this: Bitcoin’s supply is controlled at the margin by whoever is willing, or forced, to sell, not by whoever holds the most coins.

Where Bitcoin’s Supply Really Sits: ETFs, Corporations, Governments and Exchanges

At a high level, a meaningful share of circulating Bitcoin now sits with large entities:

ETFs hold a growing slice of supply inside regulated wrappers.

Public companies increasingly treat Bitcoin as a treasury asset.

Governments collectively control hundreds of thousands of coins, mostly via seizures.

Exchanges hold a shrinking pool of readily tradeable BTC.

The supply shock is mathematically inevitable. | Credit: Kyle Chassé X profile

Add those categories together, and you arrive at a striking conclusion: a large chunk of Bitcoin is concentrated in the hands of institutions and sovereigns, not retail traders.

That’s real. However, concentration alone does not equate to control.

What matters is how easily that supply can re-enter the market when conditions change.

Myth #1: Exchanges Control Bitcoin’s Supply

Exchanges don’t really own Bitcoin. They primarily hold it on behalf of users. When people point to “BTC on exchanges,” what they’re actually describing is:

Customer deposits.

Pooled hot and cold wallets.

An inventory that exists to facilitate trading.

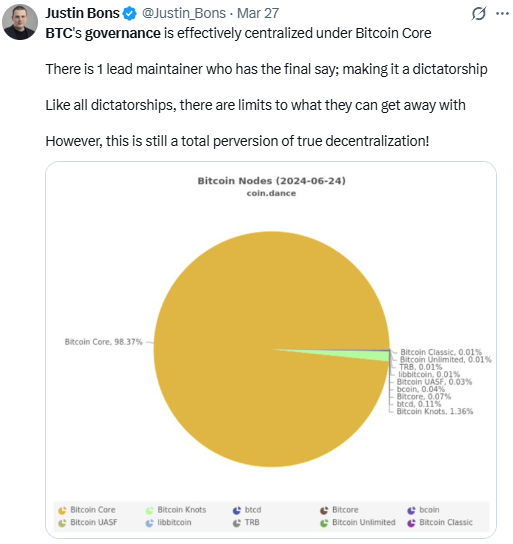

BTC’s governance is effectively centralized under Bitcoin Core. | Credit: Justin Bons X profile

That’s not a coordinated actor making strategic decisions; it’s a liquidity layer. Why this distinction matters:

Coins moved off exchanges into self-custody can still be sold quickly.

Coins moved from exchanges into ETFs can still be sold, just via shares instead of spot orders.

Coins don’t need to sit on an exchange to be liquid.

So, while declining exchange balances reveal something about the structure, they don’t reveal who controls the selling pressure.

Myth #2: ETFs Are Draining Exchanges, So Price Has No Ceiling

ETFs absolutely matter. They are one of the most important structural changes in Bitcoin’s history.

But “no price ceiling” is marketing language, not market mechanics.

ETFs Reduce Float, Not Supply

Bitcoin’s supply is fixed and predictable. What changes is the free float, which is the amount of BTC actually available at current prices.

ETFs tend to:

Move coins into regulated custody.

Align ownership with longer-term investors.

Reduce day-to-day trading churn.

This makes supply stickier, not unreachable.

If ETF investors decide to sell:

Shares are sold.

Redemptions occur.

BTC can re-enter the market, often without touching a retail exchange order book.

Price Is Set at the Margin

Bitcoin doesn’t move based on how many coins exist. It moves based on the next buyer and the next seller.

Even with millions of BTC locked up, the price can fall sharply if:

Leverage unwinds.

Miners increase selling pressure.

Macro risk shifts.

Long-term holders distribute into strength.

Tight float amplifies moves, but it works in both directions.

Many coins are held by early buyers who rarely engage in transactions. When they decide to sell, even a little, it can overwhelm incremental demand. This is not about wallet size, but psychology.

During accumulation phases, these buyers can be relatively price-insensitive. But this cuts both ways. When financing tightens or equity sentiment turns, treasury strategies can slow, or reverse quickly.

Their “control” comes from reflexivity, not permanence.

These coins rarely affect daily trading, but they matter enormously for tail risk. Announcements, auctions, or policy shifts can introduce sudden supply or remove long-standing overhangs.

4) Crypto Derivatives Market

Even when spot BTC looks locked up, derivatives can create a synthetic supply.

Liquidations, funding shifts, and hedging flows can:

Force selling.

Transmit pressure to spot markets.

Cause sharp drops even during “supply squeeze” narratives.

This is why Bitcoin can fall fast in markets that supposedly have no sellers.

Liquidity Is A Layer, Not A Place

A better way to think about Bitcoin supply is by liquidity tiers, not wallet locations:

Immediate liquidity: Coins that can be sold instantly.

Rapid liquidity: Coins held by funds, custodians, or whales that can move quickly.

Sticky liquidity: Coins constrained by mandates, governance, or long horizons.

Inert supply: Lost coins, deep cold storage, rarely touched holdings.

ETFs tend to move Bitcoin from immediate to sticky liquidity. That amplifies rallies when demand spikes, but it doesn’t eliminate the need to sell. It simply changes when, how, and why selling happens.

What The “Supply Shock” Narrative Gets Right And Wrong

ETFs have become a structurally important class of Bitcoin holders, reshaping how supply is warehoused and accessed rather than how much exists.

Corporate treasury adoption is no longer marginal, introducing balance-sheet-driven demand and reflexive risk into Bitcoin’s market structure.

Government-held Bitcoin is both sizable and concentrated, creating a latent supply that matters less on a day-to-day basis and far more in moments of policy or legal change.

These shifts are real and consequential, but they don’t equal centralized control.

Large holders do not act as a single coordinated bloc. Their incentives, constraints, and timelines differ dramatically.

ETF sponsors don’t “own” Bitcoin; end investors do, and their behavior ultimately determines whether the supply remains stable or returns to the market. Falling exchange balances don’t eliminate selling; they simply move it into different channels and structures.

A tight float does not prevent drawdowns when leverage, funding stress, or forced liquidations enter the system.

Bitcoin can be structurally scarce and violently volatile at the same time—and history shows that it often is.

When Bitcoin Supply Actually Hits the Market: Signals That Matter More Than Ownership Charts

Bitcoin’s most significant moves rarely start where most people are looking. They don’t begin with ownership charts or static supply snapshots; they start when incentives change and constraints are broken. The signals that matter are forward-looking, subtle, and often invisible until the price reacts.

Here’s what to watch if you want to understand when Bitcoin’s supply will truly hit the market:

ETF flows, not AUM headlines: Net creations and redemptions matter far more than total assets, they reveal whether “sticky” demand is accumulating or quietly turning liquid.

Corporate balance sheets under stress: Treasury-led Bitcoin strategies thrive when capital is abundant. Watch for early signs that forced discipline could replace discretionary buying in financing conditions, equity performance, and credit markets.

Government signals, not rumors: Policy statements, auction frameworks, and legal developments around seized Bitcoin matter more than speculation, they determine when latent supply becomes real.

Leverage beneath the surface:Funding rates, basis trades, and liquidation clusters often drive short-term price action, even in markets that appear supply-constrained on-chain.

No single entity controls Bitcoin’s total supply. Issuance is fixed by protocol. What is influenced is the available supply at current prices, which depends on who is willing or forced to sell.

If ETFs hold a lot of Bitcoin, doesn’t that reduce liquidity?

It reduces immediate float, not ultimate liquidity. ETF-held Bitcoin is “stickier,” but it can still re-enter the market through share sales and redemptions. Liquidity shifts form, it doesn’t disappear.

Are Bitcoin ETFs long-term holders by default?

The structure encourages longer holding periods, but the end investors are still humans and institutions. If sentiment or macro conditions change, ETF shares can be sold just as quickly as stocks.

Can Bitcoin crash even if most supply is “locked up”?

Yes. Price is set at the margin. Leverage unwinds, forced liquidations, or sudden shifts in sentiment can drive sharp declines even when long-term supply looks tight.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy