Can gold, the yuan, Bitcoin, or the euro replace the U.S. dollar? ChatGPT, Gemini, and Claude reveal why the future of global money may be multipolar. | Credit: CCN.com

Share

Key Takeaways

The Federal Reserve is expected to lower interest rates by 25 basis points on Oct. 29.

ING analysts say the September CPI came in below expectations, giving policymakers a “green light for a 25bp cut.”

However, the Fed’s attention has turned squarely to the labor market.

Every Fed cut adds liquidity and weakens the dollar, a bullish setup for Bitcoin and altcoins.

The Federal Reserve looks all but set to slash interest rates by 25 basis points on Oct. 29, marking another pivot in the U.S. central bank’s long battle to keep growth alive without reigniting inflation.

After a year of mixed economic signals and a messy government shutdown, the Fed’s next move could shake up everything, from Bitcoin and Ethereum to U.S. Treasuries and the Nasdaq 100.

While inflation may finally be cooling, analysts warn that jobs are the real driver now and that the Fed could be flying blind.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

US Inflation Cools and the Fed Gets Its “Green Light”

The latest U.S. inflation report confirmed what many traders suspected: price pressures are losing steam. That gives the Fed exactly the cover it needs to justify a cut.

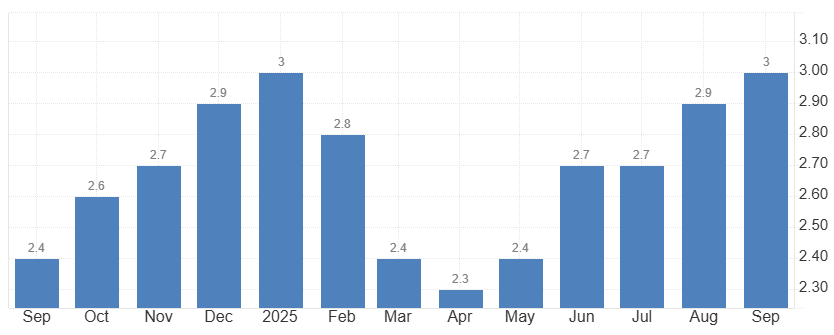

ING analysts told CCN, “U.S. inflation undershoots expectations. US September inflation was softer than expected, rising by 0.3% month-on-month and 3.0% year-on-year for headline inflation and 0.2% MoM / 3.0% YoY for core (excluding food and energy). The consensus forecast was for a 0.4% MoM headline print and 0.3%MoM core.”

U.S. inflation accelerated less than expected in September. | Credit: TradingEconomics

“As such, we have a green light for a 25bp Fed rate cut next week, even though the core month-on-month rate (blue bars) continues to track above the 0.17% MoM rate we need to average to bring the annual rate of inflation down to the 2% target.”

That “green light” has markets in rally mode. Treasury yields tumbled, stocks surged, and Bitcoin reclaimed $111,000 within hours of the report’s release.

ING’s breakdown shows inflation easing across the board: core goods rose just 0.2%, while housing, one of the biggest inflation drivers, barely budged.

“Housing was benign, with owners’ equivalent rent rising just 0.1% and primary rents up 0.2%… The biggest upside numbers were airline fares (+2.7% MoM), tobacco (+0.6%), and gasoline (+4.1% MoM). But with global energy prices falling fairly broadly in recent months, we think gasoline and airline fares should be softer again soon.”

With headline inflation now hovering near 3%, the Fed can claim progress toward its target, but there’s a new problem brewing.

What a 25 Basis Point Cut Means

A basis point equals one one-hundredth of a percentage point. When the Federal Reserve cuts rates by 25 basis points, it’s reducing its benchmark rate by 0.25%. Even small rate moves ripple through the global economy, influencing borrowing costs, mortgage rates, bond yields, and investor appetite for risk assets.

At its September meeting, the Fed trimmed its target funds rate by 25 basis points to a range of 4.00%–4.25%, marking a clear shift toward easier policy after months of tight financial conditions. The move immediately weakened the U.S. dollar, sent Treasury yields lower, and lifted risk assets from equities to cryptocurrencies.

Lower rates make credit cheaper and generally push investors toward higher-return assets. For Bitcoin and other digital currencies, easier monetary policy typically brings greater liquidity and “risk-on” sentiment, which can fuel rallies similar to those seen after previous Fed pivots.

Lower borrowing costs improve corporate earnings and boost risk appetite.

Bonds (e.g., 10-Year Treasuries)

Bond prices often rise while yields fall

As rates drop, older bonds with higher coupons become more attractive.

U.S. Dollar (DXY Index)

Often weakens

Lower rates reduce the dollar’s appeal to global investors seeking higher yields.

Cryptocurrencies (e.g., Bitcoin)

Frequently surge after cuts

Increased liquidity, a weaker dollar, and rising risk appetite often support crypto markets.

Historical Context

In 2019, during a mid-cycle adjustment, the Fed cut rates three times, and risk assets rallied across the board. Stocks climbed, bond yields declined, and Bitcoin gained more than 40% in the months that followed.

Similar patterns appeared in 2020’s pandemic-era easing cycle, when massive liquidity injections drove both equities and crypto to record highs.

Why It Matters Now:

With the Fed preparing another 25-basis-point cut on Oct. 29, these historical trends suggest that stocks, bonds, and crypto could benefit once again.

However, this time the outlook is complicated by weak labor data, tariff-related price pressures, and the risk that missing government reports could leave policymakers navigating without full visibility.

Without Jobs Data, the Fed Faces One of Its Toughest Decisions Yet

According to Nigel Green, founder and CEO of deVere Group, inflation is no longer the main obstacle. The Fed’s concern is the labor market, where things get messy.

“The inflation data was anticipated, and it’s no longer the deciding factor,” says Green.

“The Fed’s attention has turned squarely to the labor market. Jobs data will move the needle on rate cuts, but if the shutdown continues, the Fed may not even have that data in time.”

The Bureau of Labor Statistics can’t publish employment data during the government shutdown. Without that report, Fed officials would have to make one of the most consequential calls of the year without their key economic compass.

“The labor market is the Fed’s most important compass right now,” says Nigel Green. “Without it, policymakers will have to make one of the year’s biggest decisions without their clearest guide to economic health.”

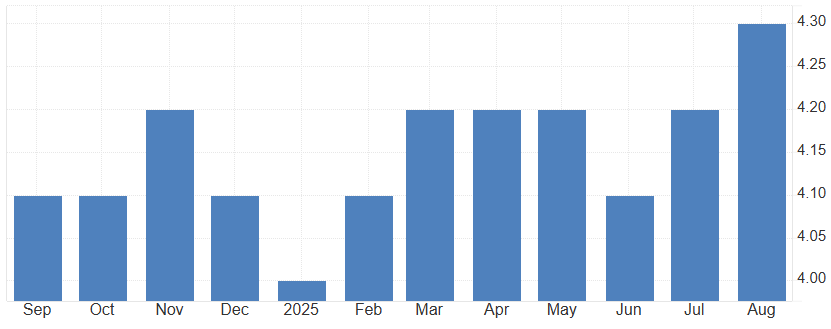

U.S. labor market over the last year. | Credit: TradingEconomics

The last available jobs report wasn’t pretty. The U.S. added only 22,000 jobs in August, and unemployment climbed to 4.3%, its highest since 2021.

“The Fed can tolerate inflation around 3%,” says Nigel Green. “What it cannot risk is a rise in unemployment that damages confidence and spending. The labor data will determine the pace and depth of future rate cuts.”

If the shutdown drags on, the next FOMC meeting could happen without official jobs data, forcing policymakers to make significant decisions based on partial information.

“This creates a dangerous blind spot,” says Green. “Inflation tells the Fed where it’s been. Jobs tell it where it’s going. Without those numbers, the central bank must rely on judgment, not evidence.”

Fed Rate Cuts Won’t Stop at 25bps, Says Pantheon Economist Oliver Allen

Oliver Allen, Senior U.S. Economist at Pantheon Macroeconomics, says the inflation data fit a broader narrative: the Fed is about to enter an extended easing cycle.

“We provisionally estimate that today’s CPI data are consistent with a 0.3% increase in the core PCE deflator, but we will refine that forecast when September’s PPI numbers, which make up one-third of the underlying source data, are released, once the federal government reopens.”

He adds that the inflation outlook remains uneven but manageable.

“Looking ahead, we expect core PCE inflation to peak at about 3¼% around the turn of the year, mostly due to a further climb in core goods inflation, as retailers pass on more of the tariff costs to consumers. Services inflation, however, is likely to grind lower, given the weak labor market and clear signs that shelter inflation has further to fall,” he said.

Expectations for future Federal Reserve’s moves. | Credit: CME Group

“The tariff boost to goods inflation will be fleeting, but softer services inflation and the moribund labor market will require the Fed to act. We therefore retain our long-standing forecast that the Fed will ease policy by a further 125bp in the coming year, including 25bp easings later this month and in December.”

In other words, the Oct. 29 cut won’t be the last. Pantheon expects another 25 bps in December and more in 2026, enough to bring rates near 3.75% by mid-year.

“The pace of rate cuts will slow, not stop,” notes Green.

“The Fed is adjusting its stance, but unreliable data raises the risk of miscalculation. It’s one thing to ease policy; it’s another to do it blind.”

Schroders Warns: “Don’t Get Too Comfortable”

While markets are already celebrating, George Brown, Senior Economist at Schroders, warns that complacency could be dangerous.

“A softer inflation print may offer temporary relief, but we caution against complacency. Tariffs are yet to be fully passed on by firms, compounding the potential for second-round effects as the Fed presses ahead with cutting rates for an already strong economy. An inflation resurgence is at risk of being underappreciated by the Fed and underpriced by the market.”

He also flagged a key risk for next month’s data: “The CPI is a wildcard. With many prices ordinarily collected in person having to be imputed due to the U.S. government shutdown, interpreting next month’s print will be especially challenging at a critical time for the Fed.”

Translation: the Fed’s “soft landing” could get rocky, and the markets may not fully price that in.

Data Scarcity Becomes Wall Street’s Biggest Risk — and Crypto’s Edge

As Washington dithers, Wall Street’s biggest challenge isn’t inflation or jobs: it’s data scarcity.

“With official reports delayed, investors are turning to private-sector measures such as the ADP employment estimate and online job postings to fill the information gap. But these indicators provide only partial insights, increasing market sensitivity to every release,” says Nigel Green.

“This data blackout is unsettling for markets,” he adds.

“Every unofficial number, survey, or rumor becomes magnified. This makes for sharper swings in bonds, equities, and currencies in the weeks ahead.”

Without real jobs data, traders are guessing, and that volatility is exactly what crypto thrives on.

Bitcoin Bulls Bet on Fed Rate Cuts to Fuel the Next Rally

Bitcoin bulls are watching closely. Every Fed cut boosts liquidity, weakens the U.S. dollar, and reignites the “risk-on” narrative that sent Bitcoin soaring in past easing cycles.

The last time the Fed pivoted dovish in late 2019, BTC jumped nearly 50% in two months. Analysts say history may rhyme.

Still, not everyone’s convinced this time will be smooth sailing. With the Fed cutting into an economy already strained by weak job growth, crypto markets could face volatility if investors shift from “liquidity optimism” to “recession fear.”

For now, though, crypto traders are betting the Fed will keep easing through 2026, and that’s bullish for risk assets.

Why Fed Rate Cuts Impact Stocks and Bonds

When the Federal Reserve cuts interest rates, it directly changes how investors value risk and returns across markets. Lower rates reduce the cost of borrowing, making it cheaper for businesses to finance operations and for consumers to spend. This typically boosts corporate earnings, sending stock prices higher, especially in growth sectors like technology, which rely heavily on credit and future earnings potential.

In the bond market, rate cuts move prices in the opposite direction from yields. As policy rates fall, existing bonds with higher yields become more attractive, driving bond prices up and yields down. This is why Treasury prices often rally immediately after a Fed cut.

At the same time, lower U.S. yields can weaken the dollar, as global investors seek higher returns elsewhere. A softer dollar makes American exports more competitive and tends to support commodity and cryptocurrency prices, which are often denominated in dollars.

The combined effect, higher stock valuations, rising bond prices, and a weaker dollar, typically signals a “risk-on” environment, where investors shift from defensive assets toward growth-oriented investments like tech stocks and Bitcoin.

Yields Drop, Stocks Surge — and the Fed’s Next Move Remains a Mystery

Bond markets are the clearest beneficiaries. The 10-year Treasury yield fell below 4.1%, the lowest in nearly three months, signaling investor confidence in the Fed’s dovish path.

Stocks followed: the S&P 500 is up by 2.4% this month, and the Nasdaq 100 nearly 3.2%, as tech and growth names rally on lower discount rates.

But as Nigel Green warned, the real danger isn’t inflation; it’s uncertainty.

“Inflation is becoming predictable. Employment is not. The Fed’s real concern is momentum, and that depends entirely on jobs.”

“Today’s CPI report doesn’t change the story. Jobs data will move the needle, but if the shutdown blocks it, the Fed will be forced to make its November decision without the single most important indicator it has. This uncertainty will influence markets long before the next cut is announced.”

What Crypto and Bitcoin Investors Should Watch Next

With the Federal Reserve poised to cut rates again, crypto investors should look beyond the headlines and monitor the broader economic signals that shape digital asset performance.

The strength of the U.S. dollar: Bitcoin has historically moved inversely to the U.S. dollar. A weaker dollar following rate cuts tends to lift BTC as investors seek alternatives that can hold value. However, if global demand for safe-haven assets rises during economic uncertainty, the dollar could rebound and cap crypto gains.

Liquidity and market sentiment: Every Fed rate cut injects liquidity into financial markets. For crypto, this often fuels rallies, but liquidity can quickly dry up if investors shift from optimism to risk aversion. Watch credit markets and Treasury yields for clues about how sustainable the “risk-on” mood really is.

Inflation vs. recession narrative: Bitcoin benefits when inflation fears dominate, reinforcing its appeal as a hedge. But if rate cuts are seen as a response to recession risks, demand for risk assets can fade. Investors should pay close attention to how markets interpret the Fed’s tone in its October and December meetings.

On-chain activity and institutional flows: Institutional adoption remains a critical driver of Bitcoin’s price direction. Tracking on-chain transaction volumes, ETF inflows, and exchange balances can provide early signals of changing investor confidence as monetary conditions ease.

Policy and regulation: Any Fed decision that impacts financial stability discussions could spill into digital asset regulation. Statements from U.S. Treasury and SEC officials following the October meeting may influence both market sentiment and compliance expectations.

If the Fed continues easing into 2026, liquidity will remain supportive for Bitcoin and altcoins, but volatility will persist. Crypto investors should balance optimism about easier policy with caution about a slowing economy and potential data-driven surprises.

The Fed’s Oct. 29 Cut Is Certain — But Easing Policy in the Dark Is the Real Risk

The Fed’s Oct. 29 cut looks like a lock. But the bigger story is what happens next.

If inflation stays tame and the job market softens further, expect the Fed to push ahead with multiple cuts into 2026, a scenario that historically lifts both stocks and crypto.

If tariffs and missing data create policy “blind spots,” the market’s euphoria could fade fast.

For now, liquidity is back, and Bitcoin, equities, and bonds are all racing to price it in.

But as the Fed prepares to act, one truth stands out: easing policy in the dark is the most dangerous cut.

Why is the Federal Reserve expected to cut rates on Oct. 29?

The Fed is preparing to cut interest rates by 25 basis points as inflation continues to cool and growth momentum slows. September’s CPI data was softer than expected: headline inflation rose 0.3% month-on-month, and core inflation (excluding food and energy) increased just 0.2%. That gives policymakers the “green light” to ease policy without stoking new inflation pressures.

How does the government shutdown affect the Fed’s decision?

The Bureau of Labor Statistics can’t release official jobs data during a shutdown, leaving the Fed without its most critical gauge of economic health. As Nigel Green warned, this creates a “dangerous blind spot.” The central bank may have to decide on rate cuts without employment data, relying more on judgment than hard evidence.

What do analysts expect after the October rate cut?

Economists like Oliver Allen of Pantheon Macroeconomics expect a series of cuts ahead, totaling 125 basis points over the next year. That includes another 25 bps in December and more in 2026, potentially lowering rates to around 3.75%. The pace may slow, but the easing cycle is far from over.

How could the rate cut impact crypto markets like Bitcoin and Ethereum?

Lower rates typically mean cheaper liquidity and a weaker dollar, both bullish for Bitcoin and Ethereum. Historically, when the Fed eases, crypto rallies. Bitcoin already increased after the CPI release. However, volatility could spike if investors shift from optimism to fear of recession.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy