The Fed’s Sept. 17 rate cut could send ripples through Bitcoin and digital assets. | Credit: Kevin Dietsch/Getty Images

Share

Key Takeaways

The Fed cut rates by 0.25% on Sept. 17, its first step away from a restrictive stance in more than two years.

By mid-2026, analysts see over five cuts, pushing the terminal rate near 3%.

Fed Chair Powell faces growing political heat from President Trump and dissent within the FOMC.

Eyes turn on cryptocurrencies too, as Bitcoin and risk assets often rally when the Fed eases.

The Federal Reserve delivered a 0.25 percentage point cut on Sept. 17 at 2 PM EST, marking the central bank’s first step away from the restrictive stance that has defined monetary policy since 2022.

While modest, this shift could have sweeping implications for global markets, from equities and bonds to foreign exchange and crypto.

September FOMC

*The Fed cuts rates by 25 bps

*A narrow majority of officials pencil in a total of at least 3 cuts this year

Understanding what this quarter-point move means requires examining the immediate market reaction and the Fed’s reasoning, the balance of risks it sees, and how different sectors, including digital assets, might respond.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

A single 25 basis point cut is not huge in absolute terms; it signals the start (or renewal) of easing, rather than a dramatic pivot.

Here are the channels through which it works, and what immediate and medium impacts can be:

Transmission Mechanisms

Short-term interest rates fall: The federal funds rate influences overnight interbank lending, and rates for many short duration liabilities. This lowers the cost of short‐term credit.

Expectations and forward guidance: What the Fed signals matters a lot. If it says there are more cuts coming (or sets projections accordingly), that moves market expectations, which influences longer term rates, investment decisions, risk asset valuations.

Bond yields and curves: Yield curves (e.g. 2-year vs 10-year) tend to respond. If short rates are cut while long rates remain historically high (because of inflation expectations or risk premia), the curve can steepen, which often stimulates borrowing.

Borrowing costs downstream: Mortgages, business loans, auto loans, credit card rates can eventually be influenced, though the impact is larger and faster for adjustable rate or floating rate instruments; fixed rates lag.

Asset prices risk appetite: Lower rates reduce the attractiveness of cash / low yield fixed income, making riskier assets more appealing, everything else being equal. Also, with lower discount rates, the present value of future cash flows rises, supporting equities, real assets, etc.

What It Does Not Do Instantly

It doesn’t immediately drop fixed mortgage rates in a big way, those depend on longer term interest rates (10-year Treasuries etc.), which are influenced by inflation expectations, global demand, and risk.

It does not instantly solve supply side inflation or inflation arising from tariffs, oil, supply chain issues.

It cannot instantly revive a housing market if buyers are constrained by affordability, down payments, or supply constraints.

WHY POWELL MIGHT CUT RATES

The reason is weak jobs data: ✓ YTD job cuts: +66% YoY ✓ Unemployment: 4.3% and rising

For the first time since 2020, the people unemployed are more than job openings

Historical Timeline: Recent Fed Rate-Cut Cycles & Their Impacts

Below is a summary of several recent US federal funds rate easing cycles (post-2000), what prompted them, what the course was, and what the observed effects were, especially on housing, equities, and crypto (where applicable).

Cycle

Period / Trigger

Size & Timing of Cuts

Economic Context

What Followed (Housing, Equities, Crypto)

2001 (Dot-com bust + 9/11)

Early 2001: Tech bubble burst, 9/11 shock

From 6.5% in 2000 down to 1.75% by end-2001; continued to 1% in 2003

Housing affordability modestly improved; equities volatile but near records; crypto buoyant, already pricing easing

Why the Fed is Cutting Rates in 2025

The Federal Reserve has held interest rates at their highest level in two decades to bring down inflation, which surged following the pandemic and the subsequent energy and supply chain shocks.

While the policy effectively cools consumer prices, it came at the cost of slower growth, tighter credit conditions, and rising pressure in labor markets.

In August, inflation moved far from the Fed’s 2% target, as pockets of stickiness remained in services and housing. At the same time, forward-looking indicators point to weaker business investment, falling job openings, and slowing wage growth. This mix gave Fed officials the confidence to dial back policy restraint, but only cautiously.

A 0.25% cut is as much a signal as it is an action: the Fed is telling markets that fighting inflation is no longer the only priority and that supporting growth is back on the table.

However, a single quarter-point cut will not revolutionize borrowing conditions overnight. Mortgage rates, credit card APRs, and auto loans will still hover at elevated levels relative to pre-2022 norms.

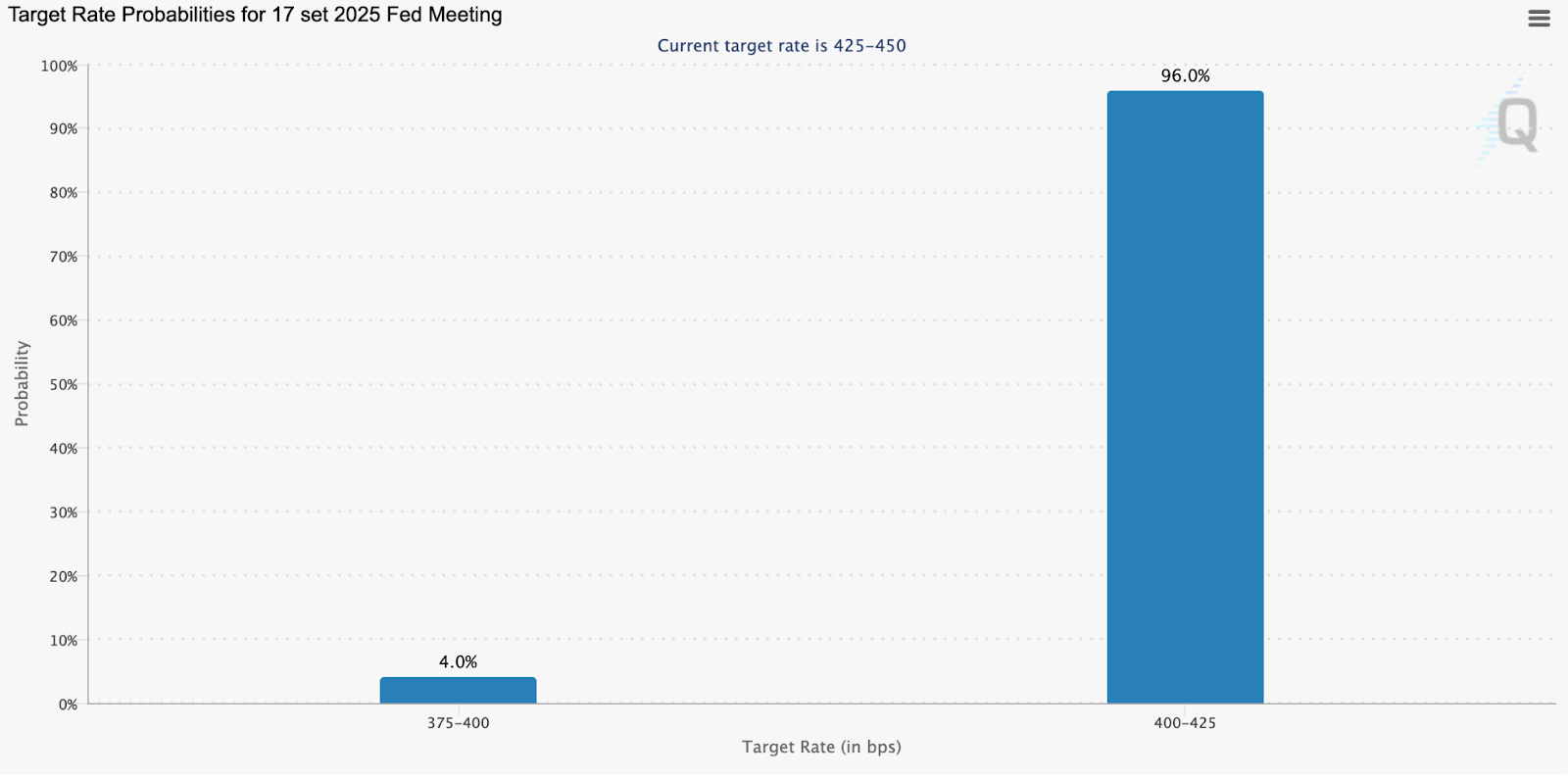

A Fed cut is in the bag, according to analysts. | Credit: CME FedWatch Tool

Fed Rate Cut Outlook: Why 25bp Is Priced In and 50bp Would Shock Markets

As mentioned, rate cuts does not mean the Fed is abandoning vigilance. Officials are acutely aware that cutting too quickly could reignite inflation.

By starting small, they leave room to observe how markets react and how economic data evolve over the next few months.

Expectations stand at 2.7 cuts by year-end, with the Fed funds rate projected around 3.7%. Looking further ahead, markets see 5.3 cuts by July 2026, taking the terminal rate down to 3%.

“The sharp repricing lower in both rates and the U.S. dollar suggests investors are positioned for a dovish outcome, particularly given new Fed Board member Stephen Miran’s open advocacy for deeper cuts,” analysts told CCN.

“Against this backdrop, the tone of Powell’s press conference and the updated dot plot will carry significant weight. Our economists expect the new dot plot to show three 25bp cuts in 2025, one in 2026, and one in 2027.”

History offers a mixed playbook: in seven past instances where the Fed resumed cutting after a long pause, four were followed by recession and equity drawdowns. At the same time, three coincided with continued expansion and higher markets.

“We remain in the no-recession camp, a view increasingly echoed by risk assets, with the MSCI World and S&P 500 both at all-time highs,” experts added.

Bumpy Ride On The Fed Roller Coaster

However, there are many moving parts to today’s meeting.

For ING’s analyst Chris Turner, “In the statement, beyond the 25bp cut, we’ll be looking for a phrase like ‘In considering additional adjustments to the target range’ which the Fed used last year to signal a succession of cuts.”

“The alternative: ‘In considering the extent and timing of additional adjustments’, would reflect hesitancy and lift short-dated rates and the dollar. The statement will also show the voting pattern, which could be something like eight for a 25bp cut, while three members – Waller, Bowman, and Miran – would vote for a 50bp cut and perhaps only Schmid would opt for unchanged rates,” Turner said.

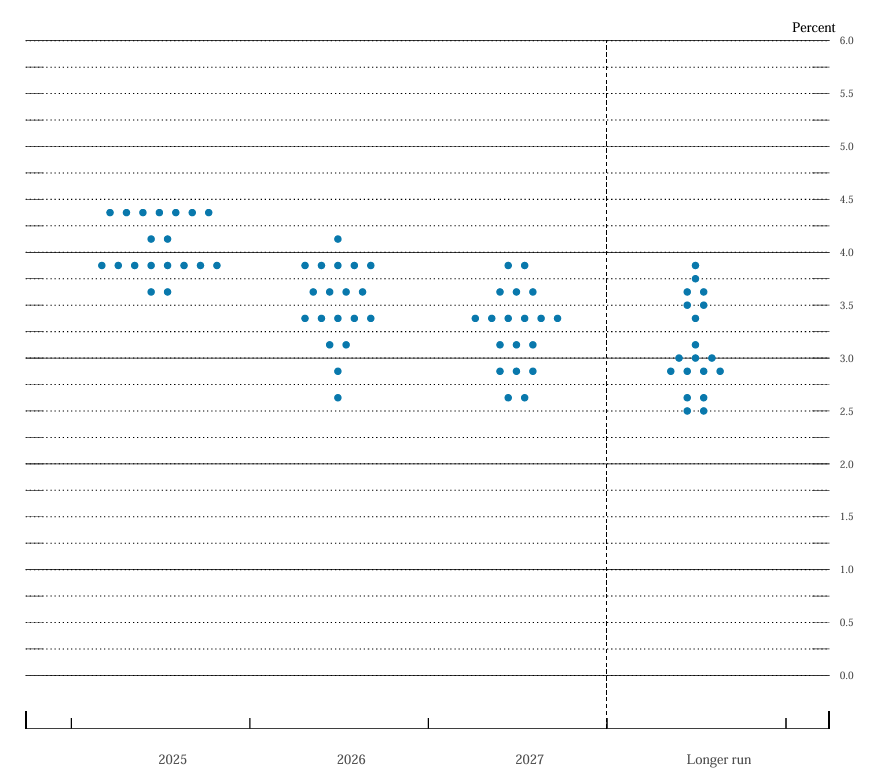

Federal Reserve’s dot plot. | Credit: Federal Reserve

“On the Dot Plots, the majority of economists think the median 2025 Dot Plot will continue to see just two cuts – i.e. policy ending the year in the 3.75-4.00% target range from 4.25-4.50% now. This could be a problem for the short end of the US curve, which prices 70bp of rate cuts,” he added.

Expectations are that the 2026 Dot will add one extra cut to the June projection, so it would shift to 3.25-3.50%, while the 2027 Dot would also shift by one cut to 3.00-3.25%.

“In short, the Dot Plot could show a slower trajectory of getting to 3.00-3.25% compared to current pricing of that zone being hit late next summer.”

Eyes On Accompanying Message

Linh Tran, Market Analyst at XS.com, told CCN that the market is currently focusing not only on whether the Fed will cut interest rates but also on the accompanying message.

“If the Fed takes a dovish stance and opens the door to a clear easing cycle, real yields will have room to decline, the USD will weaken, and gold will continue to find support. Conversely, a cautious or hawkish tone could trigger a short-term correction, even though the long-term trend may remain intact,” Tran said.

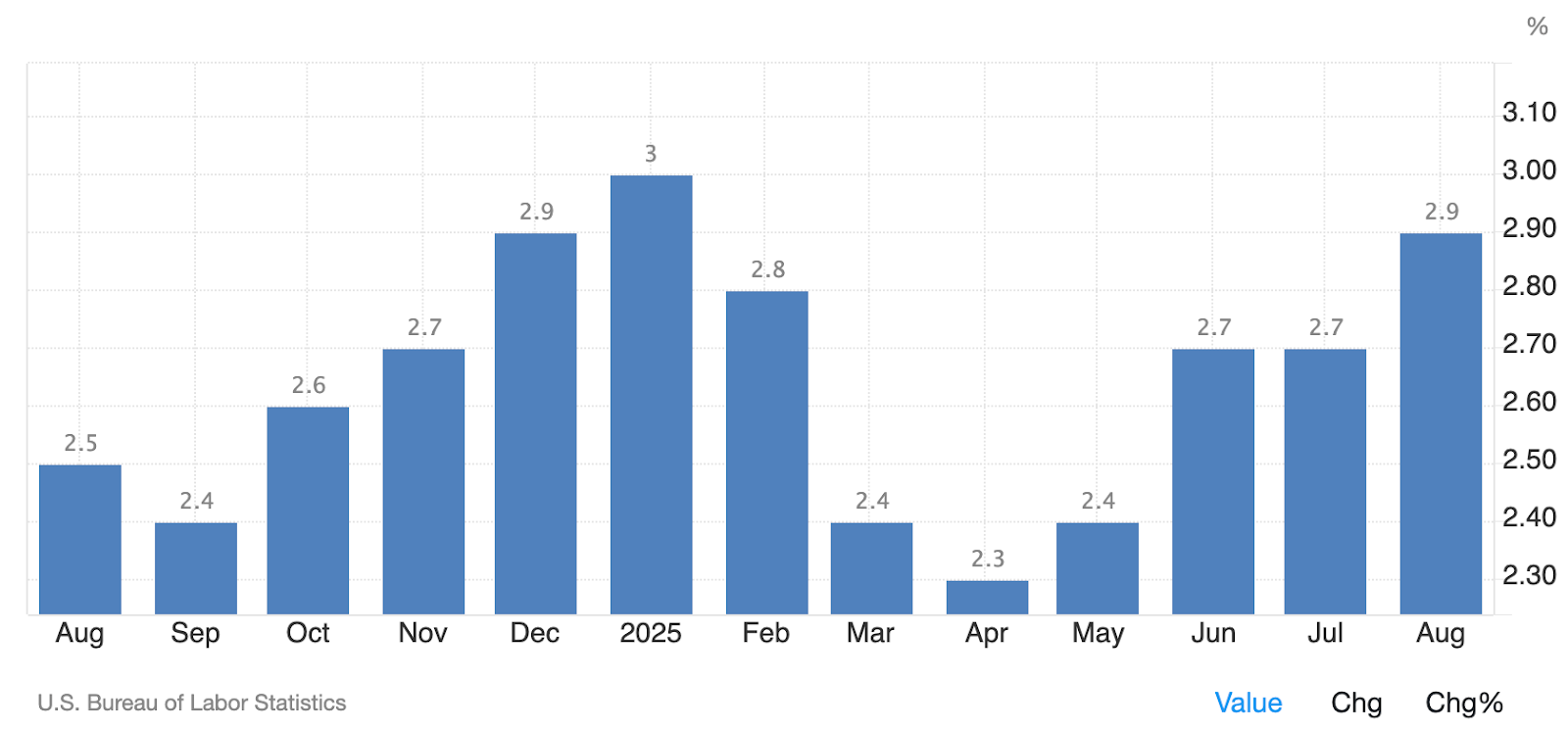

Recent U.S. economic data continue to show mixed signals. In August, CPI rose 0.4% m/m, pushing CPI y/y up to 2.9% from 2.7%, indicating that consumer inflation remains sticky.

U.S. inflation over the last year. | Credit: TradingEconomics-U.S. Bureau of Labor Statistics

On the other hand, PPI fell 0.1% m/m, reflecting that input price pressures have eased. In addition, the preliminary Michigan consumer sentiment index for September came in well below expectations, while jobless claims showed that the labor market remains resilient.

“This data set reinforces the likelihood of a 25 bps Fed cut but also highlights the risk of persistent inflation, making it difficult for the Fed to signal a rapid easing path,” the XS expert said.

In the short term, the outlook for gold remains temporarily positive. If the Fed cuts 25 bps with a dovish message, a weaker USD could help gold extend its rally toward higher target zones.

“Conversely, if the Fed surprises with a hawkish stance, a corrective phase could emerge. In this scenario, buying from global ETFs, central banks, and safe-haven demand driven by geopolitical risks will be the key factors determining the extent of the correction,” Tran added.

Impact on Traditional Markets

Equities

A rate cut typically boosts equities by lowering discount rates and signaling support for growth. Sectors most sensitive to credit conditions — small caps, real estate, and consumer discretionary — could benefit most.

Bonds

Treasury yields should drift lower, steepening the yield curve if long-term growth expectations hold steady. Investors who have stayed on the sidelines may find opportunities in duration.

Dollar and Commodities

The dollar may weaken modestly against other major currencies, providing relief to emerging markets and boosting commodities like gold and oil, which are priced in dollars.

Implications for Crypto Markets

A Return of Liquidity Tailwinds

Crypto has historically thrived when monetary conditions ease. The 2020–2021 bull run coincided with ultra-loose policy and stimulus checks. Conversely, the brutal bear market of 2022 followed aggressive tightening.

A rate cut, even a small one, signals that liquidity may start flowing back into riskier corners of the market.

Often touted as “digital gold,” Bitcoin tends to benefit from weaker dollars and falling real yields. If Treasuries rally and the greenback dips, Bitcoin could regain some of its macro hedge appeal.

Stablecoins Under Pressure

Higher interest rates have been a cash cow for stablecoin issuers, allowing them to earn hefty returns on reserve assets like Treasuries. A rate cut compresses those yields, potentially reducing revenue for firms like Circle and Tether. This could impact their profitability, ability to fund ecosystem grants, or willingness to absorb regulatory compliance costs.

Altcoins and DeFi

Lower rates encourage risk-taking further down the crypto risk curve. Altcoins, DeFi protocols, and NFT ecosystems may see renewed capital flows as investors search for yield outside of traditional fixed income. However, these markets remain fragile, and liquidity conditions will determine how far the rally extends.

Specific Considerations for Crypto in This Cycle

Crypto markets are still relatively new compared with equities or housing, but their response to Federal Reserve rate changes has become increasingly important.

Several factors shape how digital assets may react in the months following the Fed’s September 2025 rate cut:

Macro setup sets the tone: Headline CPI stood at 2.9% year-over-year in August 2025; core CPI was 3.1%. Unemployment is at 4.3%, with only +22k nonfarm jobs in August, underscoring a cooling labor market. These data points frame the Fed’s decision to ease.

Policy path expectations: Before the September FOMC, markets priced in a 25 bp cut and projected about 68 bps of additional easing through the end of 2025. Expectations matter for crypto because liquidity shifts are often priced before policy changes occur.

Crypto–equity linkage: Bitcoin’s 30-day correlation with the S&P 500 has ranged from about 0.45 in spring 2025 to nearly 0.9 by early May. When equities rise on Fed easing, crypto typically moves in the same direction, reflecting its risk-asset profile.

Institutional footprint: U.S. spot bitcoin ETFs attracted about $3.4 billion of net inflows in July 2025. Bitcoin futures open interest across exchanges hit record territory this summer, showing institutions are increasingly active and sensitive to monetary policy.

Derivatives depth: On the CME, Bitcoin futures open interest was about $16.7 billion notional on September 12, 2025, underscoring institutional positioning around Fed events.

Stablecoin liquidity link: The stablecoin market cap is approximately $255 billion. Research shows that a $3.5 billion inflow into stablecoins can lower 3-month Treasury yields by 2.5–5 basis points, while outflows push yields up by two to three times as much — evidence of stablecoin spillovers into traditional finance.

Valuation sensitivity: Lower policy rates reduce the discount rate applied to long-duration, narrative-driven assets like Bitcoin and Ethereum. With inflation moderating and labor softening, easier policy lowers the opportunity cost of holding non-yielding crypto relative to cash or short-term Treasuries.

Price context: By mid-August 2025, Bitcoin was up roughly 32% year-to-date, hitting fresh highs near $124,000. This means some optimism about Fed easing was already embedded in prices, raising “sell-the-news” risks around the cut.

Transmission via yields: If Fed easing drives down front-end rates but long yields remain sticky due to fiscal deficits or supply concerns, crypto can still benefit from looser financial conditions, though gains may be uneven.

Scenario asymmetry: A dovish trajectory with multiple cuts into 2026 would likely support crypto prices, while a stagflation scenario or inflation re-acceleration could force the Fed to pause or reverse, typically hitting crypto hardest, given its volatility.

Regulatory overlay: Beyond Fed policy, regulatory developments on asset classification, taxation, or investment product approvals will heavily influence crypto markets. Recent institutional adoption suggests these factors interact directly with liquidity conditions.

Fed Policy in 2025: Rate Cuts, FOMC Divisions, and Political Crosswinds

The year began with what JPMorgan analysts described as a “boring start to a tumultuous year for the Fed” at January’s FOMC meeting. Since then, Chair Jerome Powell has spent his final year at the helm managing the fallout from U.S. tariffs while resisting repeated pressure from President Trump to accelerate rate cuts.

Powell has also faced personal attacks, with Trump and his allies calling for his resignation. They cite everything from monetary policy disputes to the handling of the Federal Reserve’s headquarters renovation in Washington.

Policy divisions within the Fed itself have also grown sharper. Governors Christopher Waller and Michelle Bowman supported a 25bp reduction at the July meeting, arguing that tariffs would only temporarily push up inflation. Their dissent represented the sharpest split on the FOMC in over three decades.

Now, they may gain a new ally. On Monday, Stephen Miran, Trump’s former Council of Economic Advisers chair, was confirmed by the Senate to succeed Adriana Kugler, who resigned in August.

Bank of America analysts believe Miran is “likely” to back a half-point cut. They added: “We think it’s a close call as to whether Bowman and Waller would also dissent. Our base case is that Bowman would and Waller won’t.”

Meanwhile, Governor Lisa Cook – whom Trump has tried unsuccessfully to remove over allegations of mortgage fraud – will still participate in this week’s decision. A federal appeals court on Monday upheld an earlier ruling that prevented her dismissal, though the administration is expected to petition the Supreme Court for a fast-track review.

Despite Powell’s efforts to stress central bank independence and avoid being drawn into political debates, analysts warn that the pressure is increasingly shaping the Fed’s image. As SPI Asset Management’s Stephen Innes put it: the central bank “is no longer a fortress. It’s a weather vane, spun by political gusts rather than economic bearings.”

What Comes Next: Scenarios for 2025

Scenario 1: Gradual Easing Cycle

The Fed delivers another 0.25% cut in December and perhaps one more in early 2026, bringing the policy rate down by 75 basis points over six months. Inflation stays near target, growth stabilizes, and markets broadly rally. This is the Fed’s ideal “soft landing.”

Scenario 2: Stop-and-Go

Inflation proves stickier than expected in services or housing. After September’s cut, the Fed pauses for several meetings to reassess. Markets face volatility as traders bet on and off about the timing of further cuts.

Scenario 3: Aggressive Easing

Growth data deteriorates sharply. For example, unemployment spikes or credit markets seize. The Fed accelerates cuts, delivering 50bps or more in quick succession. Initially, this scenario would likely trigger a risk-off panic, but crypto could benefit once liquidity floods back in.

Here’s a plausible timeline of what could happen in the US over the next 6-18 months, and what indicators to watch.

Timeframe

Likely Developments

Key Indicators / Risks

0–3 months

Markets focus on Fed guidance; short-term rates ease slightly; equities/crypto may rally or “sell the news.”

Jobs data, CPI/PCE inflation, bond yields, housing starts, crypto flows.

The Fed’s 0.25% rate cut on September 17 is less about immediate economic relief and more about signaling a shift. For households, borrowing costs won’t suddenly plummet. For Wall Street, the message is clear: the era of relentless tightening is over.

The implications for crypto are twofold. On one hand, liquidity tailwinds are back, supporting Bitcoin, altcoins, and risk-on activity across DeFi. On the other hand, stablecoin issuers and RWA protocols face a profitability squeeze as yields decline.

Much will depend on whether this move is the first step in a gradual easing cycle or a one-off adjustment.

Either way, September’s meeting marks the return of balance to U.S. monetary policy — and the start of a new chapter in how traditional and digital markets interpret the Fed’s every word.

A 0.25% Fed rate cut lowers borrowing costs and often weakens the U.S. dollar, which can boost demand for Bitcoin as a hedge and a risk asset. Historically, Bitcoin tends to rally when liquidity conditions ease.

Will lower interest rates help altcoins and DeFi tokens?

Yes, easing monetary policy encourages risk-taking, which often flows into altcoins and DeFi projects. However, these assets remain more volatile than Bitcoin, so gains can be sharp but fragile.

Do stablecoins lose revenue when the Fed cuts rates?

Stablecoin issuers like Tether and Circle earn yield on their U.S. Treasury reserves. A Fed rate cut compresses that income, potentially reducing profits and limiting funds available for ecosystem incentives.

Is the Fed’s September 2025 rate cut bullish for crypto long term?

A single 0.25% cut is more symbolic than transformative, but if it signals a broader easing cycle into 2026, the crypto market could benefit from sustained liquidity inflows, higher risk appetite, and weaker real yields.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy