Where do we expect the US Interest rates to be in five years?

Share

Key Takeaways

The Federal Reserve cut its interest rates in September for the first time since December 2024.

The Fed aims to bring inflation down to 2%, now at 2.9%.

In the meantime, pressure mounts on Jerome Powell to resign as Fed Chair.

The next Federal Open Market Committee meeting will be on Oct. 29.

The Federal Reserve kept interest rates unchanged at its June policy meeting, but markets focused less on the decision itself and more on what policymakers signaled about the path ahead.

In his first Federal Open Market Committee (FOMC) meeting as Fed Chair, Kevin Warsh oversaw a decision to maintain the benchmark federal funds rate at 3.5%–3.75%, extending the central bank’s pause for a fourth consecutive meeting.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

While the rate decision was widely anticipated, the Fed’s updated economic projections and policy guidance revealed growing concern about persistent inflation pressures, even as economic growth shows signs of slowing.

The result was a broad market reaction that reflected expectations for higher rates over a longer period, underscoring the difficult balancing act facing the central bank.

Fed Holds Rates, but Dot Plot Turns More Hawkish

Financial markets entered the June meeting expecting no change in interest rates, with investors largely pricing in a continued pause. However, the Fed’s updated Summary of Economic Projections provided a more hawkish message than many anticipated.

According to the latest dot plot, nine of the eighteen policymakers now expect at least one rate increase before the end of 2026. Five officials project an additional 50 basis points of tightening, three anticipate 25 basis points, and one sees rates rising by as much as 75 basis points. Only one policymaker expects a rate cut during the same period.

The shift suggests that inflation remains the committee’s primary concern despite signs that economic momentum is beginning to moderate.

Recent consumer price data showed inflation accelerating to its highest level in three years, driven largely by energy costs, prompting policymakers to remain cautious about declaring victory over price pressures.

The meeting also marked a notable transition in Federal Reserve leadership. Warsh, who succeeded Jerome Powell earlier this year, entered the meeting facing intense scrutiny from investors attempting to gauge whether his approach would differ from that of his predecessor.

While some market participants expected a more dovish tone, the committee’s projections reinforced the view that policymakers remain reluctant to ease policy prematurely.

Slower Growth Complicates the Inflation Fight

The Fed’s challenge is becoming increasingly complex as inflation risks persist while economic growth slows. Traditionally, central banks can focus on either cooling an overheating economy or supporting weakening demand. The current environment presents elements of both.

The revised policy statement acknowledged ongoing uncertainty surrounding the economic outlook and highlighted the need for continued vigilance against inflation.

At the same time, policymakers appear increasingly aware that prolonged restrictive monetary policy could place additional pressure on growth.

This tension has become a defining feature of the current economic cycle. Elevated borrowing costs have helped moderate demand and cool some inflationary pressures, but they have also contributed to slower investment activity and softer growth expectations.

For the Fed, the question is whether inflation will retreat sufficiently without requiring further tightening. If price pressures remain stubbornly high, policymakers may feel compelled to raise rates despite concerns about weakening economic activity.

Energy Prices and Inflation Outlook Remain Key Variables

A major driver behind the Fed’s hawkish outlook is the recent resurgence in energy-driven inflation. Rising oil prices have pushed headline inflation higher, complicating the central bank’s efforts to guide inflation back toward its long-term target.

However, the inflation outlook remains highly dependent on developments in global energy markets.

Recent diplomatic efforts aimed at stabilizing supply conditions in the Middle East could ease pressure on oil prices in the coming months, potentially reducing one of the most significant contributors to recent inflation gains.

If energy costs begin to normalize, policymakers may gain greater confidence that inflation is moving back toward target levels, reducing the need for additional rate hikes. Conversely, any renewed supply disruptions or commodity price spikes could reinforce the Fed’s higher-for-longer stance.

For now, the June meeting reinforced a clear message: while interest rates remain unchanged, the Federal Reserve is not yet ready to pivot toward easing.

Under Kevin Warsh’s leadership, policymakers appear determined to maintain flexibility while closely monitoring inflation risks, even as concerns about slower economic growth continue to mount.

The coming months will determine whether inflation moderates enough to justify a softer policy stance or whether the Fed’s increasingly hawkish projections become reality. Either way, the June meeting highlighted that the battle against inflation remains far from over.

Interest Rates Impact on Financial Markets

Projections and decisions regarding interest rates hold immense sway over the broader economy. They affect various financial markets, including equities, bonds, and commodities.

The Fed’s key tool in this regard is the Federal Funds Rate (FFR). This is the base interest rate that influences banks, bond markets, and the economy. The Fed makes these rate decisions during its FOMC meetings, held eight times yearly. The rate adjustments in 2022 brought about several hikes, with more in store for 2023.

The increase in FFR, in turn, leads to a rise in the prime rate, the fundamental interest rate charged by banks to creditworthy customers. If the FFR goes up, so does the cost of loans and mortgages. This uptick in the cost of servicing loans translates to reduced discretionary income for consumers and businesses. This, in turn, can dampen overall demand and mitigate inflationary pressures.

Federal Reserve’s fund rates decreased during weak economic periods.

The implications for stocks are twofold: consumer-dependent sectors like retail and hospitality may face headwinds due to reduced consumer spending. Growth stocks that rely on capital and borrowing could also suffer. This is as investors shift their focus toward more stable, value-oriented investments in response to market volatility and potential downturns.

Pressure On Bonds

From a mechanical perspective, rising interest rates put downward pressure on bond values. As rates climb, the bond yield becomes less attractive than the prevailing base rate, leading to a sell-off in bonds.

This effect is particularly pronounced in the case of long-term bonds. In this case, the discrepancy between their yield and the base rate grows over time.

As a result, fixed-income securities also lose value as the opportunity cost of not owning interest-rate-tracking assets increases. Thus, predicting interest rates over the next five years becomes a critical indicator of market trends.

Historical Perspective on Interest Rate Policy

The U.S. has experienced periods of both high and low interest rate volatility in its history. In the postwar era of the 1950s, the FFR remained below 2%, bolstered by postwar stimulus and income growth. Over the next two decades, the rate fluctuated between 3% and 10% during the 1960s and 1970s, soaring to a record high of 19.1% in 1980 amid rampant inflation.

As the U.S. economy stabilized and inflation was controlled, the FFR hovered around 5% throughout the 1990s. However, recessions in 2001 and 2008 forced rates down to historically low levels, where they remained until 2016.

The COVID-19 pandemic necessitated another significant rate cut, nearly to zero. In 2022, the Fed increased rates seven times, followed by three hikes in 2023. The central bank brought the rate to its current range between 5.25% and 5.50%, the highest level in 16 years.

Factors Influencing Future Interest Rates

The Fed now faces the challenge of navigating uncertain economic conditions. These are marked by rising prices and an economic slowdown compounded by supply chain disruptions. Inflation, as well as the potential for a recession, is a top concern.

High Inflation

Inflation has been a focal point for central bank action. In 2022 and 2023, inflation accelerated due to a mix of demand and supply factors, sometimes interconnected. The Fed’s more hawkish stance appeared to have contributed to moderate price increases.

The rhetoric shifted in July. Official data from the U.S. Labor Department revealed that the inflation rate had reached 3.2% year over year. Costs of housing, car insurance, and food drove this increase.

This marked an uptick from June, which had seen the lowest rate over two years, at 3%. Analysts had anticipated this rise in the headline rate, considering the relatively weak price inflation observed in the previous July.

U.S. consumer price inflation peaks and lows

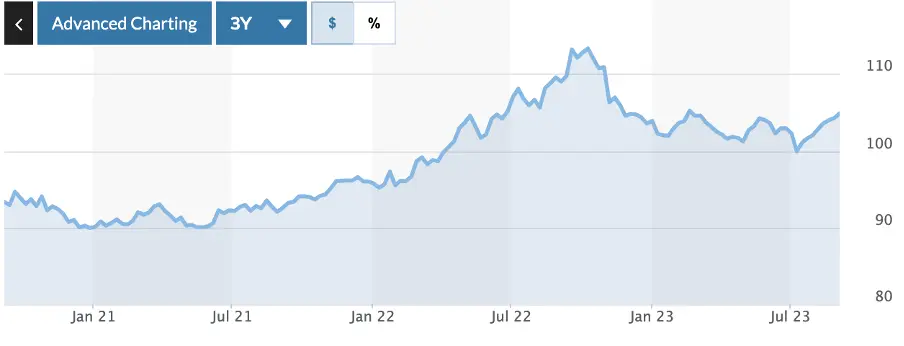

US Dollar Resilience

Despite economic turbulence, the U.S. dollar has remained remarkably resilient. Its status as a safe-haven currency, coupled with increased investor appeal due to the Fed’s hawkish monetary policy, has bolstered its performance. However, as the Fed’s monetary tightening slows and potentially pauses, the strength of the U.S. dollar appears to be waning.

USD performance.

Projected Interest Rates in the Next Five Years

The Federal Reserve’s latest projections offer a glimpse into how U.S. interest rates may evolve through the end of the decade. While policymakers left rates unchanged at 3.5%-3.75% during the June 2026 Federal Open Market Committee (FOMC) meeting, updated forecasts suggest that the era of ultra-low borrowing costs remains firmly in the past.

The central bank’s outlook reflects a delicate balancing act between controlling inflation, supporting economic growth, and maintaining financial stability. Although future rate decisions remain data-dependent, current projections indicate that rates are likely to remain elevated relative to the pre-pandemic period, even if inflation gradually returns toward the Fed’s long-term target.

The Near-Term Outlook: Rates Likely to Stay Higher for Longer

The most immediate takeaway from the Fed’s latest projections is that policymakers are not yet ready to pivot toward aggressive rate cuts. According to the June 2026 Summary of Economic Projections, nine of eighteen policymakers expect at least one rate increase before the end of the year, while only one official anticipates a rate cut.

This reflects ongoing concerns about inflation, which remains above the Federal Reserve’s 2% target. Energy prices, wage growth, and resilient consumer spending continue to create upside risks for inflation, prompting officials to maintain a cautious stance.

As a result, most economists expect the federal funds rate to remain near current levels through much of 2026, with any policy easing likely to be gradual rather than dramatic.

Rates May Gradually Decline Through 2027-2029

Beyond the next year, many forecasts anticipate a slow normalization process. Historically, once inflation is under control, the Fed tends to lower rates toward a so-called “neutral rate”—the level that neither stimulates nor restricts economic activity.

Federal Reserve estimates currently place the long-run neutral federal funds rate around 3%, significantly higher than the near-zero levels that prevailed throughout much of the 2010s. This suggests that even if inflation moderates and economic growth slows, rates may settle in a range between 2.75% and 3.25% rather than returning to the extraordinarily accommodative policies seen after the Global Financial Crisis.

Several structural factors support this higher-rate environment. Persistent government deficits, increased infrastructure spending, deglobalization trends, and aging demographics may all contribute to higher baseline inflation pressures than policymakers faced in previous decades.

Consequently, investors and businesses are increasingly adjusting to the possibility that borrowing costs over the next five years will remain materially higher than those experienced during the 2010-2021 period.

How Do Interest Rates Affect Crypto?

Bitcoin and other digital assets have demonstrated resilience in a rising interest rate environment. For instance, Bitcoin experienced remarkable growth of 2,000% in 2015 and 2016, during a period marked by rising interest rates.

Nevertheless, some experts argue that persistently high inflation, gas prices, and energy costs resulting from elevated interest rates may dampen risk appetite, potentially posing headwinds for cryptocurrencies.

Central Banks and Connection With Cryptocurrencies

Central banks wield significant influence, directly affecting money circulation and financial market stability. They have the power to modify interest rates, which, in turn, affects the borrowing rates for financial and banking institutions. Recently, central banks in major developed economies, such as the Fed, ECB, and BoE, have increased interest rates in response to widespread inflation.

Notably, cryptocurrencies are increasingly intertwined with these macroeconomic and monetary shifts. In particular, the decisions to raise interest rates, especially by the Fed, directly affect the cryptocurrency markets.

In simpler terms, the Fed’s more assertive stance has cast a shadow over cryptocurrencies, impacting market sentiment as tighter monetary policies loom.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.