Home / Education / Crypto / Blockchain / SWIFT Completes Multi-Bank Tokenized Bond Settlement Trial Using Stablecoins and ISO 20022 — What Does This Mean for XRP and XLM?

SWIFT Completes Multi-Bank Tokenized Bond Settlement Trial Using Stablecoins and ISO 20022 — What Does This Mean for XRP and XLM?

Share

Key Takeaways

SWIFT successfully coordinated full tokenized bond lifecycles across blockchain and traditional systems.

Stablecoins and ISO 20022 messaging were used within existing institutional workflows.

SWIFT is building tools that connect multiple networks while preserving compliance and operational controls.

A blockchain-based SWIFT ledger is planned to add coordinated execution, not just messaging.

SWIFT, the global financial messaging network used by more than 11,000 institutions, has completed a landmark digital asset interoperability trial with BNP Paribas Securities Services, Intesa Sanpaolo, and Société Générale–FORGE, demonstrating the settlement of tokenized bonds using both fiat and stablecoins across blockchain and traditional systems.

Stablecoins and tokenized deposits can both be used to move money on blockchain networks, but they represent different financial instruments with distinct regulatory and operational implications.

Stablecoins are typically issued by regulated entities and backed by reserves such as bank deposits or government securities. Examples include euro-denominated stablecoins like EURCV or dollar-pegged stablecoins used in crypto markets. When banks use stablecoins for settlement, they are transferring a digital representation of fiat currency issued by a third party.

Tokenized deposits, by contrast, are digital representations of actual bank deposits recorded on a blockchain. They remain direct liabilities of the issuing bank and are fully integrated into the bank’s balance sheet and regulatory capital framework. This can make them more compatible with existing banking regulations but also requires deeper changes to core banking systems.

The future of digital finance is interoperable – and we’re helping make it real.

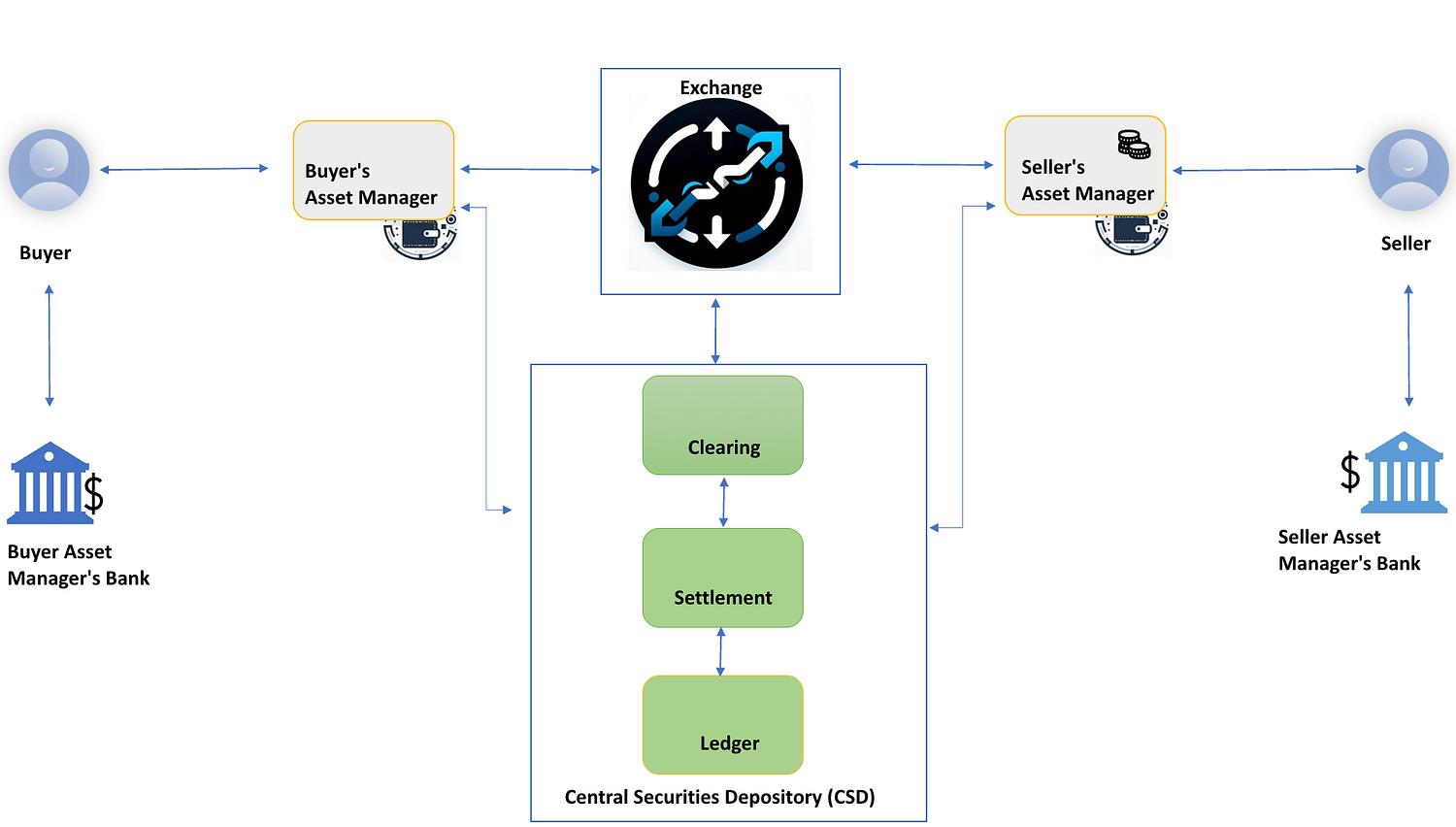

The trial marks the first time SWIFT has orchestrated end-to-end tokenized asset transactions as a single coordinated workflow, covering delivery-versus-payment (DvP), interest payments, and bond redemption, while integrating the roles of paying agent, custodian, and registrar within existing banking infrastructure.

DvP) is a settlement method that ensures an asset is delivered only if the corresponding payment is made at the same time. On blockchain, it ensures that a tokenized asset and its payment are exchanged at the same time through smart contracts that link both transfers into one coordinated action.

Instead of relying on multiple intermediaries and delayed reconciliation, the blockchain system verifies that both the security and the settlement funds are available before executing the transaction, reducing counterparty risk and operational delays.

In institutional setups, custodians, paying agents, and compliance controls remain part of the process, with standardized messaging such as ISO 20022 used to synchronize on-chain settlement with traditional banking systems, allowing regulated markets to adopt blockchain-based DvP without redesigning existing post-trade workflows.

This article outlines how SWIFT is connecting blockchain settlement with traditional banking systems through its interoperability trials.

How SWIFT Enables Stablecoin and Fiat Settlement for Tokenized Bonds

The pilot used EURCV, Société Générale–FORGE’s euro-denominated stablecoin, to support on-chain settlement alongside traditional fiat payments. This allowed banks to execute DvP settlement, meaning asset transfer and payment occurred simultaneously, a critical requirement for institutional securities markets.

BNP Paribas Securities Services and Intesa Sanpaolo acted as paying agents and custodians during the trial. All settlement instructions were processed through SWIFT, showing that tokenized securities can operate using existing institutional workflows, without requiring banks to directly manage blockchain infrastructure.

SWIFT also confirmed the trial integrated ISO 20022 messaging standards with blockchain platforms, enabling compliance, reporting, and reconciliation using the same data formats already used across global payments and securities systems.

According to SWIFT’s Digital Assets Product Lead Thomas Dugauquier, the organization is building infrastructure that will let its members adopt digital assets and currencies confidently and at scale.

SWIFT Interoperability Tests Connecting Banks to Multiple Blockchain Networks

This latest test follows several digital asset and currency experiments SWIFT has conducted over the past two years, focused on bridging blockchain systems with traditional finance.

Previous trials include:

Tokenized asset connectivity with UBS Asset Management and Chainlink, where SWIFT messaging was used to trigger on-chain settlement events across multiple blockchains.

Fiat-to-digital currency settlement tests with Citi, exploring how banks can move funds between traditional accounts and blockchain-based assets.

Digital asset settlement via commercial bank accounts with Northern Trust and the Reserve Bank of Australia.

ISO 20022 blockchain interoperability pilots with HSBC and Ant International, connecting payment messaging to blockchain transaction execution.

Tokenization is an $867 trillion opportunity.

Only one platform has been adopted by Swift, Euroclear, UBS, Mastercard, and other leaders to power tokenization use cases—all in the past 12 months. pic.twitter.com/1uD9mVJfaw

Together, these initiatives aim to address one of the main challenges facing tokenization: fragmentation across blockchains, proprietary systems, and settlement networks.

Why Interoperability Is More Important Than Speed for Banks

While blockchain networks often compete on transaction speed and cost, banks face a different set of priorities when adopting digital asset infrastructure. Financial institutions operate across multiple systems that must work together, including custody platforms, compliance tools, payment rails, securities settlement systems, and regulatory reporting frameworks.

Even if a blockchain can process transactions quickly, it does not solve the broader challenge of coordinating actions across these separate systems. For example, a securities trade must still align payment, asset delivery, custody updates, and regulatory reporting. If these systems are not synchronized, faster transaction speeds alone do not reduce operational risk or post-trade complexity.

Interoperability focuses on ensuring that different platforms, networks, and institutions can communicate and settle transactions in a coordinated way. This is why SWIFT’s trials emphasize standardized messaging, shared execution logic, and cross-platform coordination, rather than selecting a single blockchain as a universal settlement layer.

In this context, SWIFT interoperability means SWIFT is building systems that allow banks to move money and assets across different blockchains and traditional financial networks using the same standardized messaging and operational processes they already use today.

For banks, the ability to integrate digital assets into existing workflows and regulatory structures is often more important than raw transaction throughput.

SWIFT as a Neutral Orchestration Layer Across Blockchain Networks

SWIFT’s strategy is to act as a neutral orchestration layer, allowing institutions to transact across networks while continuing to use standardized messaging, compliance checks, and operational controls.

According to SWIFT, this approach allows banks to scale tokenized markets without abandoning existing regulatory and operational frameworks.

Role of Chainlink in SWIFT’s Interoperability Strategy

Chainlink has played a key role in SWIFT’s broader efforts to connect traditional financial infrastructure with blockchain-based settlement systems.

In earlier trials, SWIFT worked with Chainlink and UBS Asset Management to demonstrate how tokenized fund transactions could be triggered and settled across multiple blockchains using standard SWIFT messaging.

In that setup, SWIFT messages initiated smart contract activity, while Chainlink’s infrastructure securely transmitted instructions and data between off-chain banking systems and on-chain environments.

Chainlink has worked with Swift since 2016. | Source: @ChainLinkGod on X.

Chainlink’s Cross-Chain Interoperability Protocol (CCIP) was used to enable communication between different blockchain networks, allowing tokenized assets and payment instructions to move across chains without requiring each institution to integrate directly with multiple blockchain protocols.

This approach allows financial institutions to continue using ISO-standard messaging, compliance processes, and operational controls, while Chainlink handles the technical connectivity between:

Private and public blockchains

Tokenized asset platforms

Settlement smart contracts

SWIFT has stated that this model reduces integration complexity for banks, since they do not need to build or maintain direct blockchain connections themselves. Instead, they interact through existing SWIFT infrastructure while Chainlink provides the secure middleware layer for blockchain execution.

While Chainlink does not act as a payment network or settlement currency, its role in these trials has been focused on data delivery, transaction triggering, and cross-chain coordination, which are critical components for multi-platform tokenized asset settlement.

As SWIFT moves toward adding a blockchain-based shared ledger, Chainlink’s interoperability tooling remains relevant for scenarios where assets, liquidity, or settlement still occur across external blockchain networks.

Blockchain-Based SWIFT Ledger Planned

Following the completion of these trials, SWIFT has confirmed plans to introduce a blockchain-based shared ledger into its infrastructure.

The initial focus of this ledger will be:

24/7 real-time cross-border payments

Coordinated settlement across institutions

Shared execution logic rather than only message delivery

The project is being developed with more than 30 global banks, and is intended to complement SWIFT’s current messaging and API services, adding an execution layer that can synchronize actions between multiple parties in a transaction.

This represents a shift from SWIFT’s traditional role as a secure messenger toward providing transaction coordination and settlement orchestration in digital asset environments.

SWIFT’s Linea Blockchain Pilots and Their Role in Shared Ledger Development

As part of its shift toward a blockchain-enabled shared ledger, SWIFT has already tested real-world blockchain infrastructure in collaboration with Linea, an Ethereum layer-2 network developed by ConsenSys.

In late 2025, SWIFT launched a pilot project using Linea’s zk-EVM network to explore how interbank messaging and settlement might operate on a public blockchain environment, involving more than a dozen global banks including BNP Paribas and BNY Mellon.

Unlike its traditional role as a messaging system, this pilot looked at on-chain messaging and settlement flows, with test scenarios that included a stablecoin-like settlement token and interbank token transfers on Linea. The initiative aimed to evaluate whether blockchain could help integrate payment instructions with settlement in a unified process while meeting regulatory and privacy requirements.

Linea was chosen for several reasons in these tests:

It is a zk-rollup on Ethereum, providing scalability and cost efficiency while retaining full EVM compatibility.

The network’s zero-knowledge architecture supports privacy-focused cryptography, which is important for bank-level data protection.

Using an Ethereum-based layer-2 lets SWIFT evaluate blockchain settlement without building new protocols from scratch.

These experiments did not replace SWIFT’s core messaging functions, but informed the design of its blockchain-based shared ledger, which is now being developed with feedback from more than 30 global banks.

That shared ledger, first announced in 2025 and intended to record, sequence, and validate regulated tokenized transactions in real time, is meant to complement SWIFT’s messaging and ISO 20022 standards and ensure interoperability with both existing rails and emerging networks.

Stellar (XLM) has emphasized low-cost cross-border transfers and stablecoin issuance, including partnerships with money service businesses and fintech platforms.

However, SWIFT’s recent trials show that large banks are increasingly exploring stablecoins and tokenized deposits as settlement instruments, rather than public bridge assets. The use of fiat-backed stablecoins allows banks to retain currency exposure and compliance alignment while still gaining blockchain settlement benefits.

That said, XRP and XLM continue to operate in parallel ecosystems, particularly in retail payments, remittances, and fintech-driven corridors, while SWIFT remains focused on institutional capital markets, securities settlement, and interbank coordination.

For instance, according to network data, the XRP Ledger has processed around 1.8 million transactions per day in 2025, with monthly totals exceeding 70 million, finalizing payments in 3–5 seconds and supporting a theoretical capacity of over 129 million transactions per day based on its consensus performance. Active addresses and new account creation have also grown, reflecting broader usage beyond simple value transfer.

Recent data also shows that public blockchains like Stellar are seeing growing real-world financial activity, particularly around stablecoins and tokenized assets. According to Messari, U.S. Bank is piloting its own stablecoin on Stellar, while PayPal’s PYUSD and USDC helped drive stablecoin supply on the network up 53% year over year.

The network has also been used for government and social programs, including the Marshall Islands running the world’s first on-chain universal basic income (UBI) pilot on Stellar. In addition, more than $890 million in tokenized U.S. Treasuries, real estate, and government debt is now live on the network, with DeFi protocols such as Templar Protocol working on compliant yield products backed by real-world assets.

Stellar is becoming the financial backbone for onchain finance. | Source: LinkedIn

Rather than direct competition, the developments highlight different layers of financial infrastructure:

SWIFT focusing on institutional interoperability and regulated securities workflows.

Public blockchains like XRPL and Stellar focusing on open payment networks and token issuance.

SWIFT’s Market Practice Guidelines for Tokenized Securities Settlement

To support safe adoption of digital assets, SWIFT has submitted proposed market practice guidelines to the Securities Market Practice Group (SMPG). These guidelines aim to standardize:

Operational workflows

Settlement procedures

Messaging structures for tokenized securities

The goal is to reduce onboarding friction and ensure that tokenized assets can integrate into existing post-trade and custody systems used by global financial institutions.

Interoperability as the Focus of SWIFT’s Digital Asset Strategy

SWIFT’s trials suggest that tokenized assets are moving beyond experimentation toward operational testing within real banking environments, using:

Stablecoins

Standardized financial messaging

Existing custody and settlement roles

Rather than replacing current infrastructure, the strategy centers on connecting traditional systems with blockchain platforms, allowing institutions to adopt digital assets without redesigning their core processes.

As tokenization expands into more asset classes, interoperability, not just blockchain scalability, is becoming a central requirement for institutional adoption.

With its planned shared ledger and growing number of bank-led pilots, SWIFT is positioning itself as a key coordination layer between traditional finance and blockchain-based markets.

Did SWIFT use public blockchains in this tokenized bond trial?

The bond settlement trial primarily focused on interoperability between institutional systems and blockchain platforms, using controlled environments. However, in separate pilots, SWIFT has tested public blockchain infrastructure, including Ethereum layer-2 networks like Linea, to evaluate scalability and privacy for institutional use cases.

Why did the trial use stablecoins instead of cryptocurrencies like XRP or XLM?

Stablecoins such as EURCV are pegged to fiat currency and fit more easily within existing regulatory, accounting, and risk frameworks used by banks. This makes them suitable for securities settlement, where currency certainty and compliance requirements are critical.

Does SWIFT’s blockchain strategy replace payment networks like XRPL or Stellar?

No. SWIFT is focused on institutional securities and interbank coordination, while networks like XRPL and Stellar continue to support open payment networks, remittances, and fintech applications. They operate at different layers of the financial system.

What is the main problem SWIFT is trying to solve with interoperability?

Tokenized assets currently exist across many blockchains and settlement platforms that do not easily communicate with each other. SWIFT’s approach is designed to coordinate transactions across these systems using standardized messaging and shared execution logic.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy