Can gold, the yuan, Bitcoin, or the euro replace the U.S. dollar? ChatGPT, Gemini, and Claude reveal why the future of global money may be multipolar. | Credit: CCN.com

Share

Key Takeaways

Despite growing debates about de-dollarization, no single currency or asset currently matches the dollar’s liquidity, stability, and global trust.

It is the world’s second-largest reserve currency, but fragmented fiscal policy and limited safe debt markets constrain its ability to rival the dollar.

While China’s economic size and trade influence are significant, capital controls and political risk limit the yuan’s international adoption.

For AI, structural advantages like deep US financial markets and global network effects make the dollar extremely difficult to displace.

For more than eight decades, the U.S. dollar has been the backbone of the global financial system. It dominates international trade, underpins central bank reserves, and serves as the primary safe-haven asset during economic crises. From commodities like oil to sovereign debt markets, the dollar remains the currency the world trusts most.

Yet the dollar’s dominance is increasingly debated. Rising U.S. government debt, geopolitical tensions, and shifts in global power have prompted investors and policymakers to ask an increasingly common question:

What could replace the US dollar as the world’s reserve currency?

An analysis by The Economist clearly frames the issue. The dollar’s role is built not only on the size of the American economy but also on deep financial markets, strong institutions, and decades of global trust.

However, the publication notes that:

U.S. government debt has grown significantly.

American economic policy has become less predictable in recent years.

Investors are increasingly hedging their exposure to the dollar.

These dynamics raise the possibility that the world could gradually diversify away from dollar dominance.

To better understand how this debate is evolving, it is also useful to examine how artificial intelligence systems interpret the same question. When asked what could replace the dollar, leading AI models, including ChatGPT, Gemini, and Claude, produced responses that closely mirror mainstream economic thinking while also highlighting emerging digital and geopolitical trends.

Together, these responses reveal two key conclusions:

No single replacement currently exists.

The future monetary system may become multipolar rather than dollar-centric.

Why the US Dollar Dominates the Global Financial System

Before exploring potential replacements, it is important to understand why the dollar became dominant in the first place.

After World War II, the U.S. emerged as the world’s largest and most stable economy. The Bretton Woods system placed the dollar at the center of international finance, and even after that system ended in the 1970s, the dollar retained its global role.

https://www.youtube.com/shorts/8aweZjj8Hbo

Today, the dollar’s strength rests on several structural advantages.

Key reasons the dollar remains dominant

Deep financial markets: The U.S. Treasury market is the largest and most liquid government bond market in the world.

Institutional trust: Investors rely on the stability of American legal and financial institutions.

Network effects: Because most global trade already uses dollars, it remains the easiest currency to transact in.

Safe-haven status: During crises, investors still flock to dollar-denominated assets.

Claude’s AI response summarized this dynamic succinctly, describing the dollar’s “structural moat” as a combination of liquidity, legal credibility, and global network effects.

These advantages make replacing the dollar extraordinarily difficult.

Could the Euro Replace the US Dollar?

Among traditional currencies, the euro is widely considered the most realistic alternative to the dollar.

Introduced in 1999, the euro is now used by 21 European countries and backed by the European Central Bank, whose independence is guaranteed by treaty.

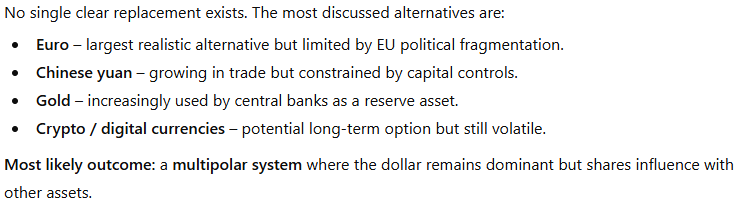

ChatGPT response on what could replace the U.S. dollar. | Credit: ChatGPT

The currency offers several characteristics that appeal to global investors.

China’s economic rise has transformed global trade. The country now has the world’s second-largest economy and is the largest trading partner for many nations.

Beijing has also made clear that it wants the yuan to play a larger international role.

AI systems consistently highlight the yuan as a potential challenger.

China is leading this effort with the digital yuan (e-CNY), one of the most advanced CBDC projects in the world.

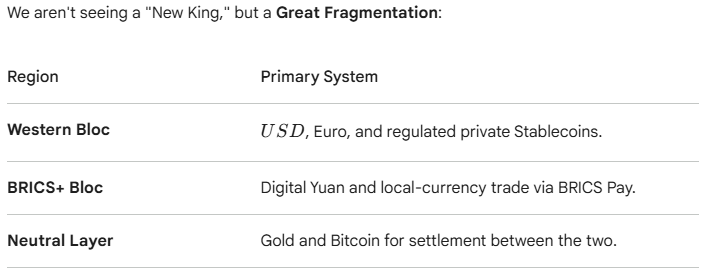

Gemini doesn’t see a “new king”. | Credit: Gemini

Gemini’s response emphasizes that China’s strategy may not be about replacing the dollar directly but about building alternative financial infrastructure.

Examples include:

mBridge, a platform allowing central banks to exchange digital currencies instantly.

Cross-border payment systems designed to reduce reliance on Western banking networks.

These innovations could reshape how international payments work, even if they do not immediately change which currency dominates reserves.

Could a BRICS Currency Replace the Dollar?

Another frequently discussed proposal is the creation of a shared BRICS currency.

The BRICS group, now expanded beyond its original five members, has repeatedly explored ways to reduce reliance on the dollar.

Claude’s response highlights the idea but also stresses the difficulties.

Instead of launching a single currency, many BRICS initiatives focus on facilitating trade in local currencies.

Gemini describes this approach as “bridges, not bucks.”

In other words, the goal may be to create financial networks that allow countries to bypass the dollar in certain transactions rather than replacing it entirely.

Most Likely Scenario: A Multipolar Currency System

Across all three AI responses, ChatGPT, Gemini, and Claude, one conclusion consistently appears: The dollar is unlikely to be replaced by a single rival currency.

Topic

ChatGPT

Gemini

Claude

Agreement

Euro as alternative

Largest realistic alternative but limited by EU politics

Part of Western financial bloc with the dollar

#2 reserve currency but limited by eurozone fragmentation

All agree

Chinese yuan

Growing role but limited by capital controls

Digital yuan expanding cross-border trade infrastructure

Most discussed challenger but trust and capital controls limit adoption

All agree

Gold

Increasingly used by central banks

Neutral reserve asset used to hedge sanctions

Historically proposed but impractical as main reserve

Partial agreement

Bitcoin / crypto

Long-term possibility but volatile

“Digital gold” neutral reserve asset

Bitcoin discussed as stateless reserve but uncertain

Partial agreement

CBDCs

Mentioned indirectly through digital currencies

Digital yuan and mBridge important for payments

CBDCs like digital yuan advancing but still national currencies

Partial agreement

BRICS currency

Not emphasized

BRICS focusing on payments system instead of new currency

BRICS currency proposed but politically difficult

Partial agreement

Why the dollar remains dominant

Liquidity, institutions, network effects

“Trinity of Trust”: liquidity, stability, legal system

Deep Treasury markets, legal credibility, network effects

Strong agreement

Single replacement for the dollar

No clear replacement

No single rival replacing it

There’s no single replacement likely

All agree

Future system

Multipolar system with several currencies/assets

Fragmented “two-speed world” financial system

Multipolar reserve structure

All agree

Global Financial System May Evolve Into a Multipolar Structure

ChatGPT describes this outcome clearly: the dollar remains dominant, but shares influence with other assets.

Claude similarly predicts a gradual erosion of dollar dominance over the coming decades, rather than a sudden shift.

Gemini presents perhaps the most vivid scenario, depicting a “two-speed world” in which different financial systems coexist.

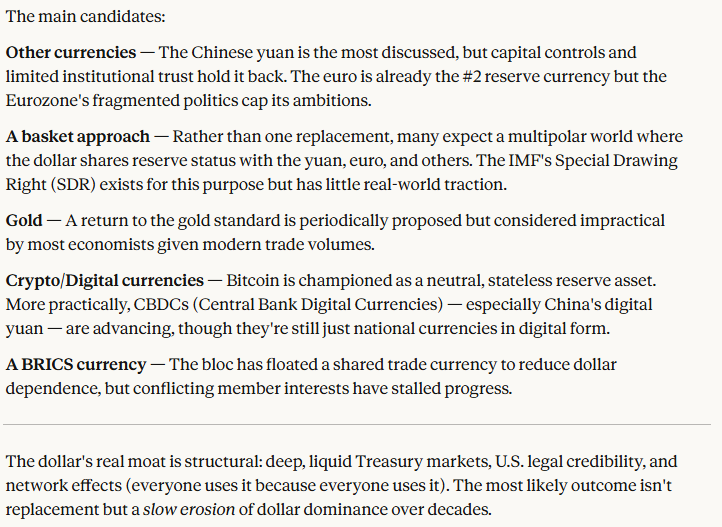

Claude lists the main candidates to replace the U.S. dollar. | Credit: Claude

Possible structure of a multipolar system:

Western bloc: Dollar, euro, and regulated stablecoins.

Emerging markets: Greater use of the yuan and local currencies.

Neutral reserves: Gold and possibly Bitcoin for settlement between systems.

Such a system would represent a major transformation of the global monetary order.

What the Future of the Global Reserve Currency Could Look Like

For decades, the stability of the global financial system has depended heavily on the U.S. dollar’s dominance.

The currency’s liquidity, institutional backing, and network effects make it extraordinarily difficult to replace.

Yet global finance is evolving.

Several trends suggest that the dollar’s share of global reserves could gradually decline:

Rising geopolitical tensions.

Increased financial sanctions.

Growing economic influence of emerging markets.

Rapid innovation in digital payment systems.

However, as both economic analysis and AI responses make clear, no single alternative currently matches the dollar’s structural advantages.

Instead of a new monetary hegemon, the future may bring something more complex: a fragmented global financial system where multiple currencies, assets, and payment networks coexist.

If that happens, the shift will likely occur slowly over decades rather than overnight.

But for a financial system built around the stability of the greenback, even gradual change could represent one of the most significant transformations in modern economic history.

A global reserve currency is a currency widely held by central banks and used in international trade, global finance, and as a foreign-exchange reserve. The U.S. dollar is currently the world’s primary reserve currency, accounting for the majority of international transactions and central bank reserves.

Could the euro replace the US dollar?

The euro is the second-most-important reserve currency, but it faces structural challenges that limit its global dominance.

What is a multipolar currency system?

A multipolar currency system is one in which multiple currencies share global reserve status rather than a single dominant currency.

Is the U.S. dollar losing its global dominance?

The dollar still dominates global finance, but its share of reserves has gradually declined as countries diversify their holdings.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy