Home / Education / Crypto / Investing / Peter Schiff Warns of 2026 US Economic Crisis Worse Than 2008 as Weak Dollar Triggers Consumer and Crypto Stress

Peter Schiff warns the US could face a major economic crisis in 2026 driven by a weak dollar, rising debt, and higher costs, with gold outperforming Bitcoin. | Credit: CCN.com

Share

Key Takeaways

Peter Schiff warns the U.S. could face a major economic crisis in 2026, potentially worse than 2008, driven by a weak dollar, rising debt, and higher borrowing costs.

Gold and silver’s sharp rally is seen as an early warning signal, with Schiff calling their performance a “harbinger” of mounting financial stress.

The U.S. dollar had its worst year in nearly a decade in 2025, while national debt surpassed $38 trillion, pushing interest costs above defense spending.

Some analysts dispute the severity of the warning, viewing recent dollar weakness as temporary volatility rather than a structural collapse.

Veteran economist and long-time gold advocate Peter Schiff is sounding one of his starkest warnings yet: the U.S. may be heading toward an economic crisis in 2026 that could rival, or even exceed, the 2008 financial meltdown.

Unlike the last crisis, which was rooted in housing leverage and banking fragility, Schiff argues the next shock will be driven by a collapsing dollar, unsustainable public debt, and rising borrowing costs that directly hit U.S. consumers.

In recent interviews, Schiff has pointed to the divergent performance of gold, silver, Bitcoin, and the U.S. dollar as an early warning signal. While precious metals surged sharply in 2025, the dollar suffered its worst year in nearly a decade.

To Schiff, this pattern resembles the early stages of the subprime crisis in 2007, visible to those watching the right indicators, but largely dismissed by mainstream markets.

Gold and Silver as a “Harbinger” of Financial Stress

Schiff believes the rally in precious metals is not speculative, but structural. Speaking on the Randi Hipper Show, he described the surge in gold and silver prices as a “harbinger” of a brewing financial storm.

Peter Schiff warns of a new financial crisis. | Credit: Peter Schiff X profile

In 2025:

Spot gold surged more than 60%.

Bitcoin fell roughly 7%.

The U.S. Dollar Index (DXY) dropped by over 10%.

To Schiff, this divergence mirrors 2007, when subprime mortgage stress surfaced before the broader financial system unraveled. Then, as now, warning signs appeared first in niche markets rather than headline indices.

Why Schiff Thinks Bitcoin Will Struggle, Not Benefit

A core element of Schiff’s thesis is his rejection of Bitcoin as a crisis hedge. While crypto advocates often argue that a weakening dollar benefits Bitcoin, Schiff believes a severe currency crisis would instead favor tangible stores of value.

In that environment, consumers and investors are likely to prioritize stability over volatility. “Out of everything that’s going to survive,” Schiff said, “gold and silver are going just to skyrocket.”

Rather than decoupling, Schiff expects Bitcoin to behave more like a risk asset, declining alongside equities if liquidity tightens and financial stress intensifies.

Dollar, Debt and a Consumer-Driven Economic Crisis in the US

Schiff’s warning centers on the U.S. consumer, whom he sees as uniquely exposed to currency weakness. U.S. national debt now exceeds $38 trillion, with interest costs alone surpassing annual defense spending.

A weaker dollar, Schiff argues, directly impacts households by making essentials more expensive. Unlike 2008, when policy stimulus buffered consumers, today’s environment offers fewer escape valves:

This combination, Schiff warns, increases the risk of a prolonged and socially visible downturn.

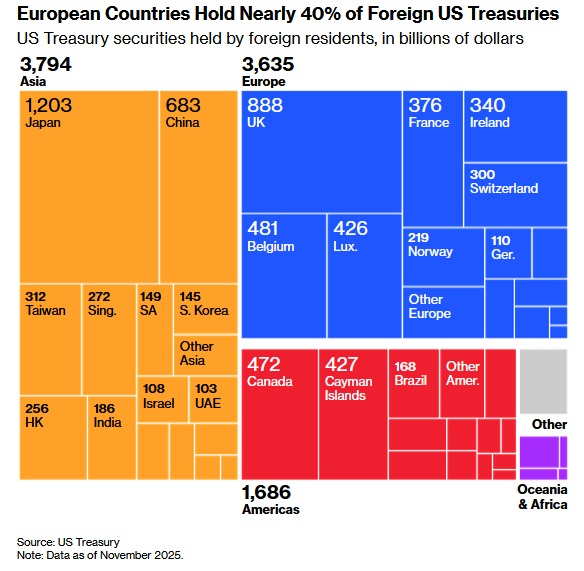

Are Treasuries the Next Pressure Point?

Concerns are also growing around the stability of U.S. Treasuries. Foreign investors hold about $3.6 trillion in U.S. government debt, roughly 40% of total foreign holdings.

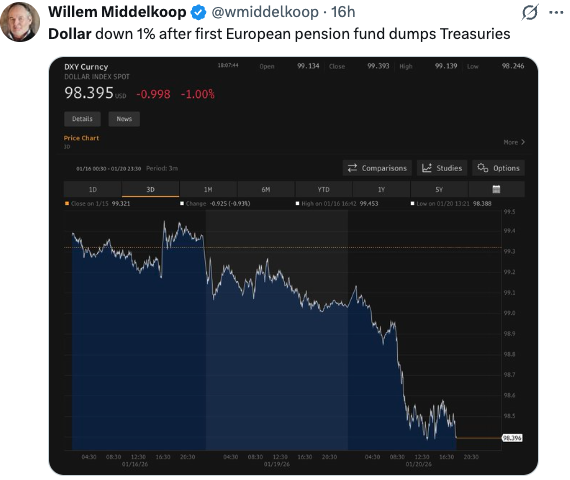

Recent developments have raised eyebrows, including a Danish pension fund announcing plans to exit Treasuries due to rising credit risk and fiscal concerns. While isolated, such moves highlight broader unease.

U.S. Treasuries largest holders. | Credit: U.S. Treasury

Schiff sees this as a potential catalyst for broader financial stress.

Is the Dollar Sell-Off Structural or Temporary?

Not all analysts agree with Schiff’s outlook. Some argue the recent dollar weakness reflects short-term volatility rather than structural decay.

ING analysts attribute part of the sell-off to spillovers from Japanese bond volatility, while Stephen Innes of SPI Asset Management described the move as a “scare trade” rather than a regime shift. Importantly, Federal Reserve rate-cut expectations remain largely unchanged, suggesting markets still trust U.S. monetary policy.

“We are taking the view that the dollar has some room to recover today. Japanese bonds have rebounded, and U.S. Treasuries and equities are on track to follow higher later today”, ING’s Francesco Pesole said.

“And with Trump headed to Davos, we see some scope for de-escalation on the Greenland risk and fears of European dumping of U.S. assets. EUR/USD can return below 1.1700 in this environment.”

“Our view is, however, that this is not a sell-off worth chasing in USD. Long-dated Japanese bonds rebounded sharply overnight, lifting one source of USD downside risk for today’s European-US session,” Pesole added.

Dollar is falling after a Danish pension fund announced it will sell all its U.S. Treasuries. | Credit: Willem Middelkoop X profile

Stephen Innes added: “The dollar was treated yesterday like a cracked hull in a storm, but the market has a habit of mistaking noise for structural damage. We are not chasing this sell-off. If anything, the tape reads more like a temporary air pocket than the start of a lasting descent.”

“The catalyst was imported volatility rather than homegrown weakness. Japanese government bonds detonated first, exporting yield shockwaves across global fixed income. That spillover rattled nerves and triggered a reflexive liquidation of U.S. assets.”

“When long-end yields jump abruptly, currencies tethered to fiscal credibility tend to wobble first. That is why the dollar, sterling, and yen were the three worst performers on the day. This was not a classic risk-off script. It was a balance sheet anxiety trade,” Innes said.

Despite signs of stabilization, Schiff believes the underlying imbalances remain unresolved. In his view, repeated short-term fixes only delay the reckoning.

Unlike 2008, when the crisis was sector-specific, Schiff warns the next downturn could be currency-driven and economy-wide, making it harder to contain.

What This Means for Investors and Consumers

Schiff’s warning is less about predicting an exact timeline and more about recognizing structural risk. Gold’s strong performance, scrutiny of U.S. fiscal sustainability, and renewed focus on currency dynamics suggest investors are reassessing long-held assumptions.

For consumers, a weaker dollar could mean sustained pressure on purchasing power. For investors, it raises questions about diversification, hedging, and the role of traditional safe havens.

Whether Schiff’s most dire predictions materialize or not, his message is clear: the signals are already visible. As in 2007, the early warnings may be easy to dismiss, until they are not.

Why does Peter Schiff believe a major U.S. economic crisis could hit in 2026?

Schiff argues that rising public debt, a weakening U.S. dollar, and growing borrowing costs are converging into a structural problem. He believes these pressures could directly impact U.S. consumers and trigger a broader crisis similar to, or worse than, the 2008 financial meltdown.

How is this potential crisis different from 2008?

The 2008 crisis was driven largely by housing leverage and banking system failures. Schiff warns that the next crisis would be currency- and debt-driven, meaning its effects could spread more evenly across the economy rather than being concentrated in one sector.

Why does Schiff see gold and silver as warning signals?

Schiff views the strong performance of gold and silver as early indicators of stress in the financial system. He compares their recent surge to the rise in subprime mortgage stress in 2007, which preceded the broader collapse in 2008.

What role does U.S. debt play in Schiff’s warning?

U.S. national debt has exceeded $38 trillion, and interest payments are rising rapidly. Schiff believes this limits the government’s ability to respond to economic stress and increases the risk of a loss of confidence in U.S. financial stability.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy