Will the digital euro change the Europe idea of money? | Credit: ccn.com

Share

Key Takeaways

The digital euro project is accelerating, with the ECB having completed its preparatory phase.

If the timeline holds, the EU is expected to finalize legislation in 2026, launch pilots in 2027, and introduce the digital euro by 2029.

The digital euro is not a stablecoin or a cryptocurrency, but a central bank-issued digital currency.

The ECB views the CBDC as necessary to counter the rise of U.S. payment giants, the emergence of private stablecoins, and the decline of cash.

Europe is getting closer to launching one of its most ambitious financial experiments ever: the digital euro, a central bank digital currency (CBDC) designed for everyday use. What started as a cautious research project is now moving toward real-world testing.

The European Central Bank (ECB) has wrapped up its two-year preparation phase and is now building the infrastructure, tech stack, and regulatory foundation for what could become the first major CBDC in the Western world.

And if that happens, Europe won’t just be changing payments; it’ll be changing how its citizens think about privacy, trust, banking, and monetary sovereignty in the digital age.

What Is the Digital Euro and How Will It Work?

At its core, the digital euro is essentially central-bank money, similar to physical cash, but in digital form.

Issued by: The Eurosystem (ECB and the national central banks).

Used for: Everyday payments, online, in stores, and peer-to-peer.

Not a stablecoin: It’s not issued by a private company and not backed by Treasuries.

Not a crypto asset: It doesn’t fluctuate in price; it’s a 1:1 euro.

Exists next to cash: It does not replace banknotes, but complements them.

What the digital euro will work for. | Credit: European Central Bank

For crypto audiences, the most straightforward comparison is this: a digital euro is like a permissioned, state-run stablecoin with strict privacy rules and banking-grade backing.

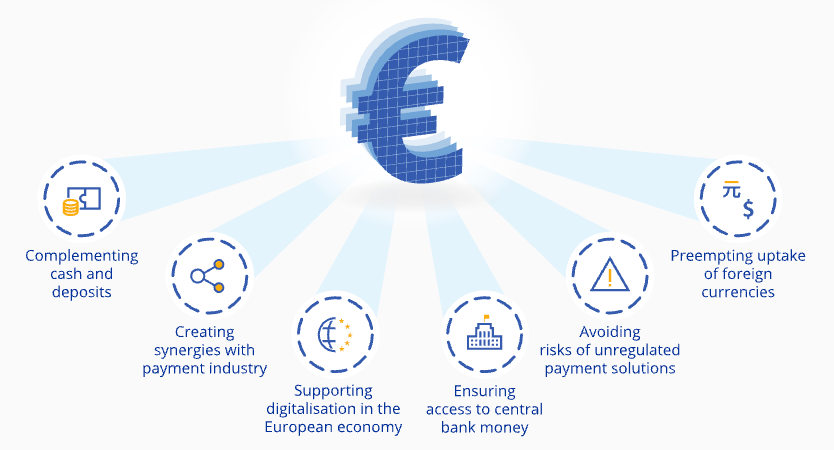

Why the ECB Says the Digital Euro Is Necessary for Europe’s Future

The ECB isn’t shy about why it’s pushing for a CBDC. It sees three threats:

Cash usage is declining, which weakens public access to central-bank money.

A digital euro is Europe’s attempt to stay relevant, competitive, and sovereign in a financial world increasingly shaped by stablecoins, digital platforms, and tokenized assets.

Digital Euro Rollout Timeline: Key Dates From 2026 to 2029

In 2026, EU lawmakers are expected to vote on the legal framework for the digital euro.

In mid-2027, the pilot phase could begin for a limited number of users, with controlled tests.

In 2029, the first possible issuance is expected, provided everything proceeds smoothly.

This would make Europe one of the first major economies to launch a retail CBDC, ahead of the U.S., and on par with China’s more advanced digital yuan rollout.

Political Fight Over the Digital Euro: Banks vs. Lawmakers vs. the ECB

Crypto isn’t the only sector full of drama. The digital euro debate has created rare public tension between big banks, EU lawmakers, and the ECB.

Major European banks are worried. A group of 14 banks recently argued that the digital euro could:

Drain deposits.

Duplicate private payment solutions.

Disrupt lending models.

Banks fear that customers may transfer money from bank accounts to digital euro wallets, thereby reducing the available capital for loans.

How the digital euro will work. | Credit: European Central Bank

ECB policymakers pushed back, saying they’ll add strict holding limits and liquidity tools to prevent significant outflows.

Lawmakers can’t agree. There are two camps in Parliament:

Privacy-first lawmakers want offline, quasi-anonymous payments, also known as digital cash.

Security-first lawmakers want traceability to fight fraud and crime.

The ECB itself opposed parts of a recent legislative proposal that mandated a fully offline model, arguing it could increase fraud risks. This political tension will define the final shape of the product.

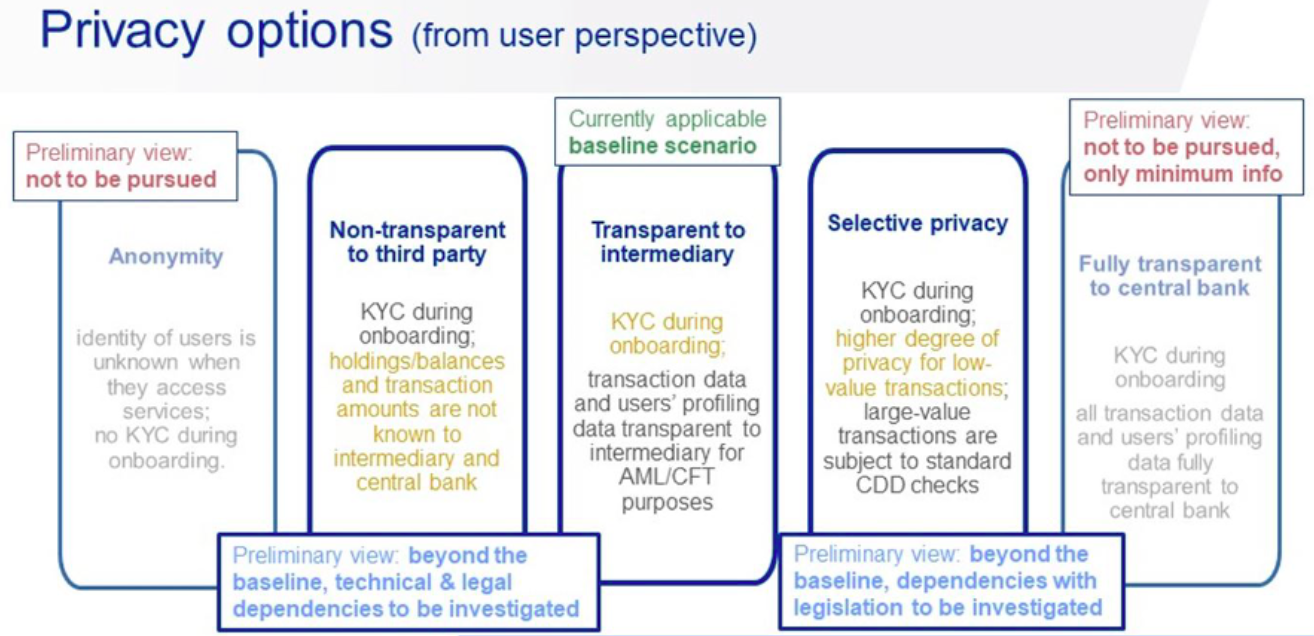

Digital Euro Privacy Concerns: What Users Need to Know

No topic has caused more confusion and fear than privacy. The ECB insists it doesn’t want access to user data. EU officials say the digital euro is being designed with more privacy than commercial digital payments, not less.

Still, crypto users are right to ask hard questions: Who sees what? How much? Under what conditions?

Until technical standards and legal rules are published, privacy remains the digital euro’s biggest trust barrier.

The Digital Euro Technology Stack: How Europe Plans to Build It

The ECB is now contracting authentic vendors, and AI fraud-detection firm Feedzai won a contract to monitor the digital euro network.

This shows:

The ECB is preparing for the introduction of large-scale digital payments.

AI and automated fraud detection will play a significant role.

The digital euro will require heavy infrastructure to function safely.

Unlike decentralized crypto, the digital euro will rely on:

Permissioned ledgers.

Regulated intermediaries.

Strict identity rules.

Government-set privacy parameters.

Centralized monitoring tools.

Crypto-native? No. Secure, programmable, and regulated? That’s the goal.

How the Digital Euro Could Change Everyday Payments in Europe

If you live in Europe, the digital euro could eventually let you pay instantly, even when banks are closed, and send money offline from one phone to another.

It also allows you to hold a small balance directly with the central bank, rather than a commercial bank.

Privacy options of the digital euro. | Credit: European Central Bank

Everyday tasks, such as recurring payments, could become programmable, working automatically in the background without needing extra apps or intermediaries. You can avoid some of the fees associated with card networks today.

For crypto users, though, the most intriguing aspect is the system’s built-in programmability, which brings the digital euro closer to the smart-contract world they are already familiar with.

Impact on Crypto: What a Digital Euro Means for Stablecoins, DeFi and Tokenization

Here’s the nuance most headlines miss: the digital euro is not a competitor to Bitcoin or Ethereum. It is a competitor to stablecoins, banks, and payment giants.

Crypto markets will likely feel the impact in several ways:

Stablecoins in Europe will face tougher competition: Even if the digital euro is permissioned, it will pressure private stablecoin issuers to improve transparency and compliance.

Tokenized assets will finally get native settlement: Institutional DeFi, RWA, and on-chain securities need a trusted on-chain cash leg. A digital euro could provide that.

CBDCs globalize the idea of programmable money: Central banks adopting programmable features indirectly validate concepts that crypto introduced.

Privacy debates will shape CBDC and crypto regulations: If Europe leans toward stronger privacy protections, it could set global standards, including for crypto.

Dutch Central Bank Chief Warns of Rising Stablecoin Risks

Dutch central bank governor Olaf Sleijpen has warned that the rapid growth of stablecoins could pose new risks to financial stability and complicate monetary policy in Europe. Speaking in an interview with the Financial Times, Sleijpen said that if the expansion of U.S. dollar–backed stablecoins continues at its current pace, they could soon become systemically important.

He cautioned that large redemptions might trigger forced sales of assets such as U.S. Treasuries, potentially unsettling bond markets and undermining central banks’ ability to manage interest rates and inflation. Sleijpen noted that privately issued stablecoins, often operating outside full regulatory oversight, may also weaken monetary sovereignty within the euro area.

His remarks underline growing concern among European policymakers that the stablecoin market’s size and structure could transform it from a niche crypto product into a macro-financial vulnerability, prompting closer scrutiny and possible regulatory tightening ahead.

Will Europeans Trust a Digital Euro? The Adoption Challenge Ahead

The digital euro’s success will hinge on two things:

Privacy: If people believe the ECB or governments can monitor small transactions, adoption will stall.

Practical usefulness: It must be easier, cheaper, or safer than what Europeans already use, which is no small task.

Today, cards, online banking, SEPA transfers, and Apple Pay cover most needs.

A digital euro needs clear advantages, or it risks becoming a political project without real demand.

Digital Euro Development: What to Watch in the Next 24 Months

Crypto world should keep an eye on:

The final legal text (2026).

ECB’s detailed privacy standards.

Pilot rollout details: how many users, which banks?

These details will determine whether the digital euro becomes a powerful public payment rail or a bureaucratic experiment few people use.

Digital Euro: Europe’s Bold Experiment in Redesigning Money

Whether you’re crypto-native or simply curious, the digital euro matters because it forces Europe to answer deep questions:

What does privacy mean in the digital age?

Should governments or companies control digital payments?

How much programmability should money have?

Who gets to verify and settle transactions?

What role do banks have when central-bank accounts are one tap away?

The digital euro won’t replace crypto, but it will redefine digital payments, challenge stablecoins, and influence regulators globally.

If done right, it could become the most crucial monetary infrastructure Europe builds this decade.

If done wrong, it will spark a new wave of skepticism and push more people toward decentralized alternatives.

Either way, it marks a historic moment: Europe is redesigning money for the digital world, and the outcome will have far-reaching implications that extend far beyond the eurozone.

The digital euro is a proposed central bank digital currency (CBDC) issued by the European Central Bank (ECB). It’s essentially digital cash, designed for everyday payments and always worth exactly one euro. It won’t replace physical cash but will exist alongside it.

When will the digital euro launch?

The timeline currently looks like this: in 2026, EU lawmakers will vote on the legal framework; in mid-2027, a pilot program with limited users will be launched; and in 2029, the earliest possible public issuance is anticipated. These dates may shift depending on political negotiations and technical progress.

Is the digital euro a cryptocurrency?

No. It is not a cryptocurrency and is not decentralized. It’s more akin to a state-run stablecoin operating on a permissioned infrastructure with strict rules, regulated intermediaries, and identity verification requirements.

Will it replace stablecoins like USDT or USDC in Europe?

It may compete with them, especially in the payment sector. The digital euro isn’t meant to replace crypto assets like Bitcoin, but it will compete directly with private stablecoins and payment platforms.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy