The Senate Banking Committee’s Jan 15 markup could grant XRP, SOL, and DOGE "Bitcoin-like" status. Is this the green light for more Altcoin ETFs? | Credit: CCN.com

Share

Key Takeaways

The Senate Banking Committee’s draft framework allows decentralized “network tokens” to be regulated as digital commodities, not securities.

Tokens tied to networks no longer under “common control” gain strong presumptions against securities classification, even if a founding entity initially issued them.

The bill clearly separates primary issuance from secondary trading, reducing regulatory risk for exchanges, market makers, and ETF issuers.

Passive investment vehicles and exchange-traded products receive tailored exemptions, signaling legislative intent to accommodate ETFs.

The U.S. Senate Banking Committee’s draft version of the Digital Asset Market Clarity Act could mark a turning point for how major cryptocurrencies are regulated in the U.S.

While Bitcoin has long enjoyed regulatory clarity as a commodity, the bill outlines a framework that may extend similar treatment to other large-cap tokens such as XRP, Solana (SOL), Hedera (HBAR), Chainlink (LINK), and Dogecoin (DOGE). This shift could meaningfully reshape the outlook for spot altcoin ETFs.

At the core of the proposal is a clear legal distinction between digital commodities and securities, paired with a presumption that sufficiently decentralized network tokens should not be regulated as investment contracts.

This approach directly addresses years of regulatory uncertainty that have held back institutional adoption and product development.

Why XRP, Solana, HBAR, LINK and DOGE Could Qualify for Bitcoin-Like Treatment

The draft legislation introduces a formal definition of a “network token.”

Section 4B(a)(6) defines a network token as a digital commodity intrinsically linked to a distributed ledger system and states that such tokens are treated as non-securities under federal securities laws. This mirrors Bitcoin’s long-standing treatment as a commodity rather than a security.

Crucially, network tokens are explicitly treated as non-securities for purposes of federal securities laws, provided they do not grant holders traditional financial rights such as equity, debt claims, dividends, or liquidation preferences.

This definition closely aligns with how regulators currently perceive Bitcoin. Bitcoin derives its value from network usage, security, and adoption, rather than from the managerial efforts of a centralized issuer. Under the bill, tokens that operate similarly can fall outside the SEC’s securities regime, even if a founding entity initially distributed them.

This framework is asset-agnostic. If XRP, SOL, HBAR, LINK, or DOGE meet the decentralization and functional criteria, they qualify for the same non-security status Bitcoin enjoys.

For assets such as XRP, SOL, HBAR, LINK, and DOGE, this represents a critical shift. Each powers a live blockchain network with broad participation, transaction utility, and decentralized governance elements. The bill acknowledges that value appreciation driven by network activity or decentralized governance does not, by itself, make a token a security.

Decentralization Rules in the CLARITY Act and What They Mean for Crypto Regulation

One of the most significant aspects of the draft bill is its approach to decentralization and “common control.”

Section 4B(b)(2) provides that secondary market sales of network tokens do not constitute securities transactions, so long as they are not part of an investment contract tied to an issuer’s ongoing efforts. This is critical: it removes the legal overhang that has historically blocked spot ETF approvals for many altcoins. Bitcoin already benefits from this clarity; this section extends it to qualifying network tokens broadly.

The legislation directs the SEC to establish criteria and safe harbors for determining when a distributed ledger system is no longer under the common control of related persons.

What CLARITY Act does. | Credit: PM Capital Group X profile

Once a network is certified as not subject to common control, its associated token benefits from strong legal presumptions:

Ongoing disclosures tied to an issuing entity can terminate.

This framework is particularly relevant for XRP and Solana, both of which have faced scrutiny over whether early development teams retained excessive influence.

The bill establishes a formal, transparent pathway for regulators to recognize when networks mature beyond issuer dependence, a feature that has been largely absent from prior enforcement-driven approaches.

ETP Inclusion May Grant Certain Crypto Tokens Non-Ancillary Status

A newly highlighted section of proposed digital asset legislation introduces a meaningful regulatory classification for certain crypto tokens, designating them as “non-ancillary assets” based on their inclusion in exchange-traded products (ETPs) as of Jan. 1, 2026.

Under the provision, a token will not be required to file the additional disclosures imposed on other digital assets if it meets a specific criterion: it must be the primary underlying asset of an ETF or ETP listed on a national securities exchange and registered under Section 6 of the Securities Exchange Act as of the cutoff date.

A passage of the CLARITY Act. | Credit: CLARITY Act draft

What the Provision Does

Treats ETP inclusion as a proxy for regulatory maturity and market legitimacy.

Exempts qualifying tokens from ancillary-asset disclosure requirements.

Aligns specific large-cap tokens with Bitcoin and Ethereum from the outset.

As drafted, the rule would classify some tokens as non-ancillary assets from day one. For example:

Bitcoin (BTC)

Ethereum (ETH)

XRP (XRP)

Solana (SOL)

Litecoin (LTC)

Hedera (HBAR)

Dogecoin (DOGE)

Chainlink (LINK)

🚨NEW: Here’s an interesting section giving some tokens classification as non-ancillary assets based on their inclusion in exchange-traded products as of January 1, 2026.

Regulatory clarity: These tokens would avoid duplicative issuer-level disclosures, reducing compliance uncertainty.

Institutional signal: ETP inclusion is effectively recognized as a form of regulatory vetting.

Market impact: Assets already supported by major exchanges and asset managers gain a formal advantage.

Broader implications:

Establishes a two-tier regulatory framework, separating institutionally embedded assets from newer or smaller tokens.

Reinforces the role of ETFs and ETPs as gatekeepers in the regulation of cryptocurrencies.

Shifts oversight focus from token issuers to market infrastructure and product sponsors.

Overall, the provision reflects a pragmatic approach by lawmakers: rather than re-examining the status of widely traded, exchange-listed crypto assets, it treats ETP inclusion as sufficient evidence of non-ancillary status, effectively expanding Bitcoin- and Ethereum-like treatment to a broader set of tokens under U.S. securities law.

Altcoin ETF Implications: How the Bill Lowers Barriers to SEC Approval

ETF issuers have consistently pointed to regulatory ambiguity as the primary barrier to launching spot products tied to non-Bitcoin cryptocurrencies. The Clarity Act directly addresses that issue by providing statutory recognition that many widely traded tokens are digital commodities, not securities.

For the SEC, this distinction is foundational. Spot Bitcoin ETFs were approved only after regulators accepted that Bitcoin markets fall under a commodity framework with oversight by the CFTC. By extending similar treatment to other decentralized network tokens, the bill lays the legal groundwork for:

More precise jurisdictional boundaries between the SEC and CFTC.

Reduced litigation risk for ETF sponsors.

Greater confidence in custody, disclosure, and market surveillance standards.

Notably, the bill also includes explicit exemptions and waivers for exchange-traded products and passive investment vehicles, allowing them to operate without triggering insider resale restrictions that apply to token insiders.

This provision appears tailored to accommodate ETFs and similar institutional products.

Secondary Market Protections That Strengthen the Case for Crypto ETFs

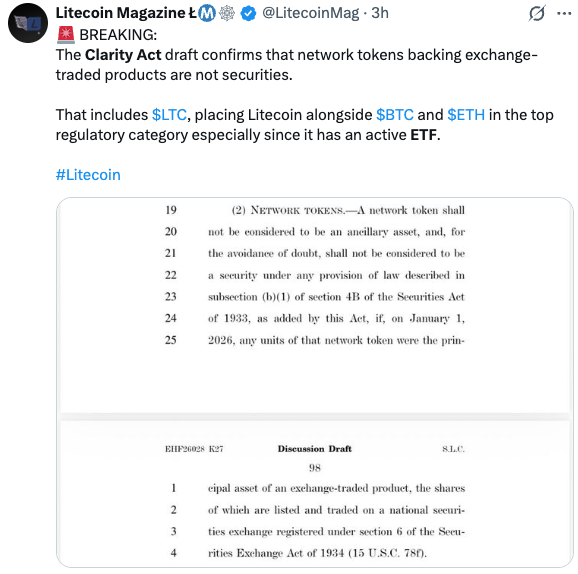

Another significant implication for ETF viability is the bill’s treatment of secondary market transactions. Under the draft, the law explicitly doesn’t consider the resale of a network token by non-originators a securities transaction. This even if the token arrived initially through an investment contract.

This is a direct response to concerns raised in past enforcement actions, where regulators blurred the line between primary issuance and secondary trading.

Network tokens backing ETPs are not securities. | Credit: Litecoin Magazine X profile

By separating the two, the legislation provides a clearer legal basis for exchanges, market makers, and ETF issuers to support liquidity without inheriting issuer-level regulatory risk.

For large-cap altcoins with deep global markets, this clarity could accelerate institutional participation and deepen U.S.-based liquidity, key prerequisites for ETF approval.

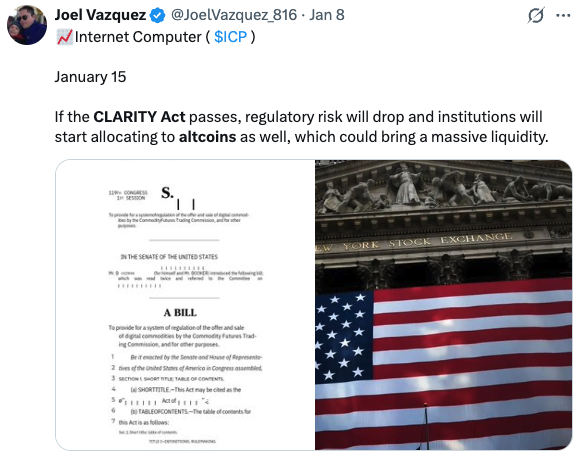

Is the Clarity Act Bullish for Altcoins and Institutional Adoption?

While the bill does not guarantee ETF approvals, it materially improves the odds. Regulatory clarity tends to reduce risk premiums, attract institutional capital, and support product innovation.

Users believe that if CLARITY Act passes, regulatory risks will drop. | Credit:Joel Vazquez X profile

Encourage asset managers to revisit stalled ETF proposals.

Push regulators toward consistency rather than case-by-case enforcement.

That said, implementation details will matter. The SEC retains authority to define decentralization thresholds, enforce anti-fraud rules, and oversee disclosure during transitional periods.

Markets should not expect immediate approvals, but the structural barriers are clearly going to be lower.

What Crypto Market Structure Bill Signals for the Future of US Digital Asset Regulation

More broadly, the Senate Banking Committee’s draft signals a philosophical shift away from regulating crypto primarily through enforcement actions. Instead, it adopts a rules-based, technology-neutral framework that acknowledges how decentralized networks actually operate.

By placing XRP, SOL, HBAR, LINK, DOGE, and similar assets on a regulatory footing closer to Bitcoin, the bill acknowledges that the crypto market has evolved beyond a binary “security vs. non-security” debate. For investors, developers, and ETF issuers alike, that shift could prove transformative.

Still, as the moment U.S. policy finally caught up with the realities of modern blockchain networks, it opened the door to the next generation of crypto investment products.

What is the Senate Banking Committee’s draft crypto bill?

It is a draft version of the Digital Asset Market Clarity Act, which aims to establish a comprehensive regulatory framework for digital assets by clearly distinguishing securities from digital commodities.

Which cryptocurrencies could benefit from the bill?

Large-cap tokens such as XRP, Solana (SOL), Hedera (HBAR), Chainlink (LINK), and Dogecoin (DOGE) could benefit if they qualify as decentralized “network tokens” under the bill’s definitions.

Does the bill classify XRP and other altcoins as commodities?

The bill does not explicitly name specific tokens. Still, it creates a legal category for decentralized network tokens that would be treated as digital commodities rather than securities, similar to Bitcoin.

What does this mean for altcoin ETFs?

Greater regulatory clarity around commodity status could lower legal and compliance barriers for spot altcoin ETFs, making approvals more likely, though not guaranteed.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy