US Treasury yields are rising as bonds sell off. Could this trigger a sharp drop in Bitcoin, Ethereum and XRP prices? | Credit: CCN.com

Share

Key Takeaways

The U.S. Treasury will settle nearly $300B in new debt tomorrow, creating one of the largest single-day liquidity drains in years.

This cash is deposited into the Treasury General Account (TGA), withdrawing liquidity from the markets until it is later spent back into the economy.

Risk assets, such as stocks, bonds, and Bitcoin, may wobble in the short term as liquidity tightens across markets.

Bitcoin stands to benefit in the long term, as, historically, every major liquidity pivot by the Fed has fueled Bitcoin’s strongest bull cycles.

Most people have no idea what is about to hit the financial system. Still, November 18th (tomorrow’s) U.S. Treasury settlement could trigger one of the largest single-day liquidity drains in recent history.

The U.S. Treasury is set to settle $285 billion to $325 billion in new debt tomorrow. That is not a typo: nearly $300 billion will be sucked out of the banking system in a matter of hours.

If you’re wondering why this matters for Bitcoin, here’s the full breakdown.

The Treasury’s $300 Billion Liquidity Drain Explained — Why It Matters for Bitcoin and Markets

When the Treasury issues new debt (Treasury bills, notes, bonds), investors buy those securities. But the real liquidity impact occurs on settlement day, when the money actually moves.

How the Treasury market liquidity evolved recently. | Credit: Federal Reserve Bank of New York

That means:

Banks, funds, and institutions must wire roughly $300 billion to the Treasury.

That money leaves the private financial system.

It is deposited into the Treasury General Account (TGA), essentially the government’s checking account at the Federal Reserve.

This creates an instant drain of liquidity because the money is not circulating in markets. It is effectively “parked” at the Fed.

When money enters the TGA, it is removed from the broader economy until the government spends it.

Kralow summarized it simply: “When this debt settles, banks must wire $300 billion into the Treasury’s account. That cash leaves the system. Bank reserves fall sharply.”

This is the first key pressure point.

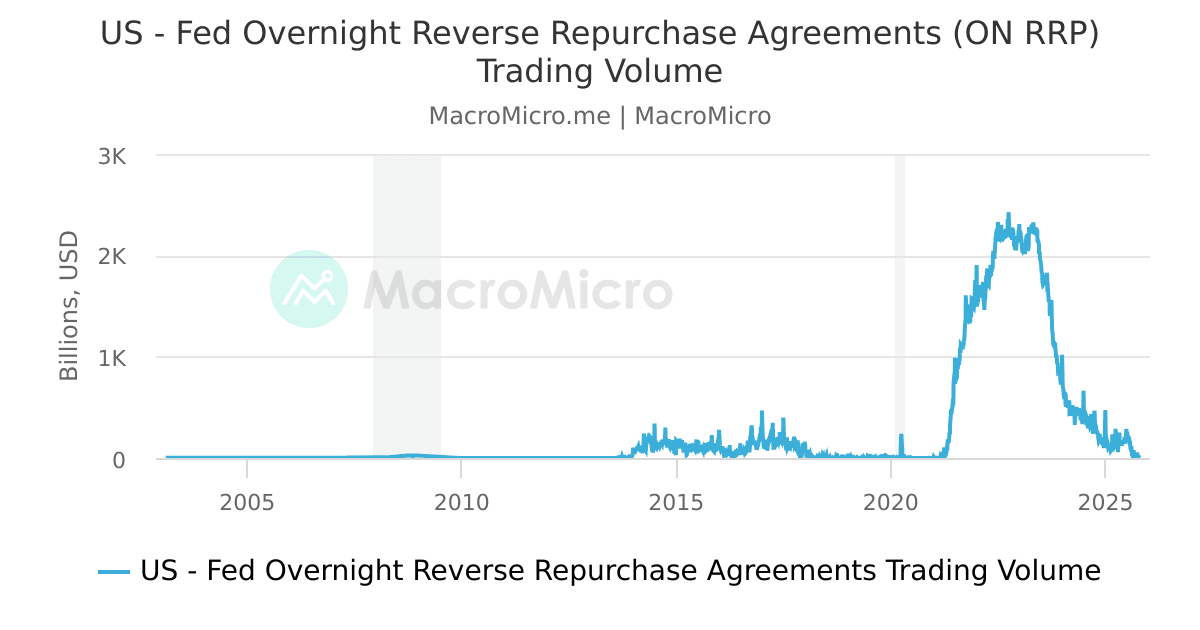

Why the Liquidity Drain Is Dangerous: ON RRP Is Empty and Buffers Are Gone

Typically, large Treasury settlements are mitigated by liquidity buffers, the most significant of which is the ON RRP facility (Overnight Reverse Repo Program). This has been a central shock absorber for money-market funds and banks over the last two years.

Federal Reserve’s ON RRP trading volume. | Credit: MacroMicro

But now?

ON RRP is nearly empty, with less than $100B remaining.

Bank reserves are near $3.2 trillion, above stress thresholds, but not by much.

The system has virtually no cushion for a sudden liquidity shock.

Kralow puts it bluntly: “We’re operating with no buffer.”

In simple terms, think of reserves and the ON RRP as “emergency fuel tanks.” They used to be full. Now the tanks are empty, and the system is running on fumes. This is why a $300 billion liquidity drain is so dangerous.

Repo Market Stress Signals a Liquidity Crunch Before the Treasury Drain Hits

The repo market, the core plumbing of the financial system, is where banks and funds borrow cash using Treasuries as collateral. If repo rates rise, it signals a liquidity shortage.

Stress is appearing even before the $300 billion drain hits.

This is the canary in the coal mine.

Kralow warned: “Expect tight funding, elevated repo rates, and stress in short-term markets.”

If repo markets crack, everything else shakes: stocks, bonds, credit markets, and leveraged hedge funds.

Why Hedge Funds Are at Risk of Forced Selling as Liquidity Tightens

One of the biggest liquidity-sensitive trades in the world today is the Treasury basis trade, used heavily by hedge funds. It relies on:

Cheap repo funding.

Massive leverage.

Small arbitrage profits.

If repo funding becomes expensive or unavailable, the trade becomes unprofitable, fast.

What happens next? Forced deleveraging. Hedge funds may be forced to delever, which means block selling in equities or bonds.

When hedge funds unwind trades rapidly, they sell large amounts of assets. This pushes prices down across the board. This is why liquidity drain has the potential to shock markets.

How a Liquidity Shock Could Hit Risk Assets — Including Bitcoin

When liquidity dries up, risk assets usually fall. Traders, institutions, and funds tend to sell:

Stocks.

Bonds.

High-yield credit.

Crypto.

Bitcoin, despite its long-term narrative, does react to liquidity cycles in the short term. Risk assets and the almighty Bitcoin may take a hit. When $300 billion is drained in a single day, liquidity-sensitive assets tend to wobble until the cash recirculates.

This is not bearish in the long term; it’s simply how liquidity mechanics work. Money moves out, then prices wobble, then money comes back in, and, in the end, markets stabilize.

This Liquidity Event Is Not Quantitative Easing (QE) — It’s the Exact Opposite

A flood of new Treasury issuance is not quantitative easing. Kralow makes that clear: “Not QE. This is the opposite. A temporary liquidity vacuum created by heavy Treasury issuance.”

QE adds liquidity. Treasury issuance subtracts liquidity until the government spends it back into the system.

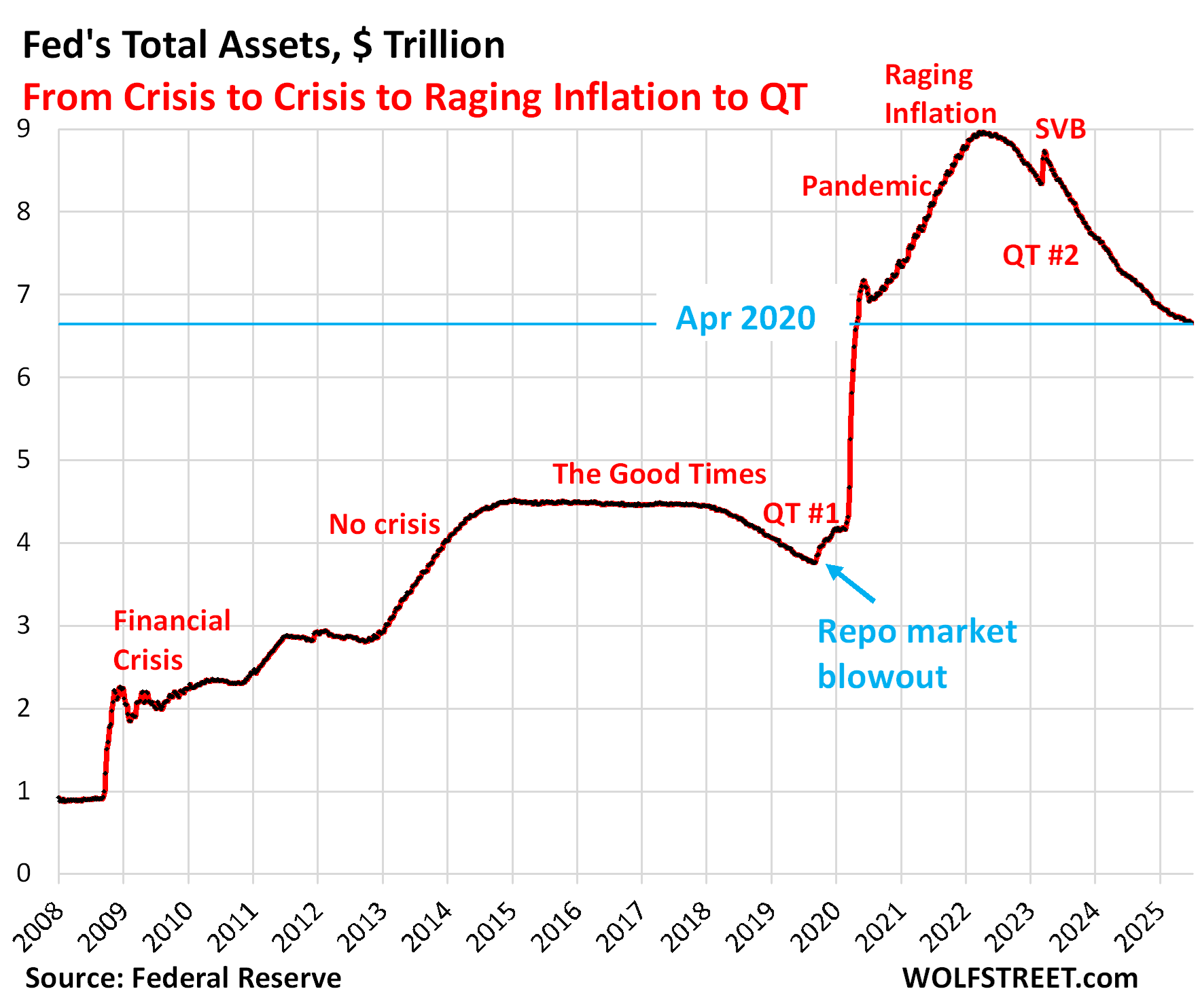

Fed’s total assets in $ trillion. | Credit: Wolfstreet.com

But here’s the key: if these liquidity shocks keep repeating while ON RRP is empty, the Fed eventually gets cornered.

How? Because markets cannot withstand repeated liquidity drains without something breaking.

This is where Bitcoin comes into play.

How a Liquidity Crisis Could Become Bitcoin’s Next Major Bullish Catalyst

If the financial system experiences repeated liquidity stress, the Fed faces two choices:

Option 1: Let Markets Break

Not politically acceptable.

Not economically acceptable.

Would trigger massive instability.

Option 2: Step In With QE or QE-like Liquidity Support

The more likely outcome.

Especially as election season approaches.

Kralow summarized it perfectly: “More cracks = pain… then money printer BRRRRRR. As a result: Bitcoin Valhalla.”

In the short term, liquidity shocks hurt risk assets. In the long term, liquidity shocks force central banks to inject liquidity. And Bitcoin thrives during liquidity injections.

This pattern has repeated in 2013, 2017, 2020, and 2021. Bitcoin’s strongest moves occur after major liquidity pivots. We may be approaching another.

Why Bitcoin Historically Surges When the Fed Is Forced to Add Liquidity

Bitcoin is built on hard-coded scarcity. It cannot be printed. It cannot be diluted. And it does not rely on repo markets or liquidity facilities.

When central banks eventually respond to market stress with:

QE.

Liquidity injections.

Rate cuts.

Balance-sheet expansions.

Bitcoin has historically become one of the strongest beneficiaries. Because in a world where money supply expands, the hardest asset with the strictest supply cap tends to outperform.

What Happens Next: The Most Likely Market Chain Reaction

Here’s how this liquidity shock is expected to play out:

Immediate impact: Treasury settlement instantly drains up to $300 billion from the banking system. Reserves drop, and cash becomes scarce.

Funding stress hits as repo markets tighten: With less cash available, repo rates spike. Short-term funding gets tight, and stress indicators rise across money markets.

Risk assets react: Equities, bonds, and Bitcoin may experience short-term pullbacks as markets adjust to the sudden liquidity squeeze.

Liquidity flows back: As the Treasury begins spending the newly raised funds, cash slowly returns to the financial system, easing some of the pressure.

Repeated shocks strain the system: If large Treasury issuances continue while buffers remain empty, the strain builds. At some point, the Fed cannot allow systemic liquidity cracks to widen.

The Fed’s hand is forced: Not immediately, but inevitably. Extended stress pushes the Fed toward QE-style interventions or other liquidity injections.

Bitcoin emerges as the long-term winner: History shows that when central banks are pushed back toward easing, hard assets like Bitcoin benefit the most. What feels like short-term pain today may set the stage for Bitcoin’s next major upside cycle.

Treasury settlement is one of the biggest liquidity shocks of the year. Few are paying attention, but the impact may be felt across repo markets, hedge funds, equities, bonds, and Bitcoin.

In the short term, Bitcoin may feel the pressure.

However, in the long term, these liquidity crunches accelerate the timeline toward the next major Federal Reserve liquidity pivot; historically, the most potent catalyst for Bitcoin’s biggest bull markets.

Why does a $300 billion Treasury settlement matter for markets?

Because when the U.S. Treasury settles new debt, banks and institutions must send money to the Treasury’s account at the Federal Reserve. That cash leaves the financial system temporarily, creating a sudden liquidity drain. Less liquidity results in tighter funding markets and increased volatility across assets.

How does this liquidity drain affect Bitcoin?

Bitcoin is highly sensitive to liquidity conditions. When liquidity is pulled out of the system, risk assets (including Bitcoin) often dip. However, historically, when the Federal Reserve tightens, it eventually provides more liquidity, and Bitcoin tends to rally strongly after those pivots.

What is the Treasury General Account (TGA)?

The TGA is the U.S. government’s “bank account” at the Federal Reserve. When money enters the TGA, it is removed from the broader economy until the government spends it. Significant TGA inflows temporarily tighten liquidity.

Will Bitcoin crash because of this liquidity shock?

In the short term, Bitcoin may dip alongside other risk assets. But long term, repeated liquidity stress increases the odds that the Federal Reserve must step in with QE-like support. Historically, Bitcoin has performed exceptionally well after those liquidity pivots.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy