Is Strategy (MSTR) a Ponzi scheme? | Credit: CCN.com

Share

Key Takeaways

Strategy Inc. holds around 650,000 BTC as of December 2025, over 3% of total Bitcoin supply.

Bitcoin accumulation has been funded primarily through equity and high-yield perpetual preferred issuances.

Critics, including Peter Schiff and Scott McClintic, argue the model resembles a leveraged pyramid or Ponzi-like structure.

Critics view Strategy as a pioneering digital-asset treasury, providing leveraged exposure to Bitcoin.

Strategy Inc. has become synonymous with one thing: ultra-leveraged Bitcoin accumulation. What began in 2020 as a treasury hedge under the leadership of Executive Chairman Michael Saylor has evolved into one of the most aggressive Bitcoin-backed financial structures globally.

As of December 2025, Strategy holds 650,000 BTC, representing more than 3% of the entire Bitcoin supply, acquired through a steady stream of equity and debt sales.

But a quiet shift in late November has sparked a wave of market anxiety. For the first time, Strategy’s leadership acknowledged a scenario where the company might sell Bitcoin to meet its obligations. For a company whose identity is built around “never selling,” the admission was seismic.

With critics calling the company a “leveraged pyramid” and supporters praising it as a visionary digital-asset treasury, the question now hangs over markets: Is Strategy a revolutionary Bitcoin corporation—or a debt-fueled Ponzi waiting to collapse?

This educational deep dive breaks down the mechanics behind Strategy’s model, the controversy over its sustainability, and the significance of its new willingness to sell BTC.

Inside Strategy’s Business Model: The Mechanics Behind Its Massive Bitcoin Purchases

Since 2020, Strategy has employed a primary lever to build its massive Bitcoin war chest: raising capital to purchase Bitcoin, issuing additional securities, and acquiring more Bitcoin.

In 2025 alone, Strategy raised approximately $20 billion through the issuance of newly issued common stock and a series of high-yield perpetual preferred shares. The company describes its strategy as “strategically accumulating Bitcoin using equity and debt financings.”

Strategy holds 650,000 Bitcoin as of Dec. 1, 2025. | Credit: Strategy

As of Dec. 1, 2025, Strategy held 650,000 BTC with a cost basis of roughly $50 billion. The company’s enterprise value hovers around $66 billion, backed by approximately $71 billion in Bitcoin collateral. In effect, Strategy operates like:

A Bitcoin investment trust.

Leveraged through equity dilution.

Supporting a suite of high-yield securities relying on continued liquidity.

As long as the stock trades above the value of its Bitcoin holdings, Strategy can issue shares at a premium and use the proceeds to buy more BTC. This is why a metric called mNAV (Market Net Asset Value) has become central to Strategy’s survival.

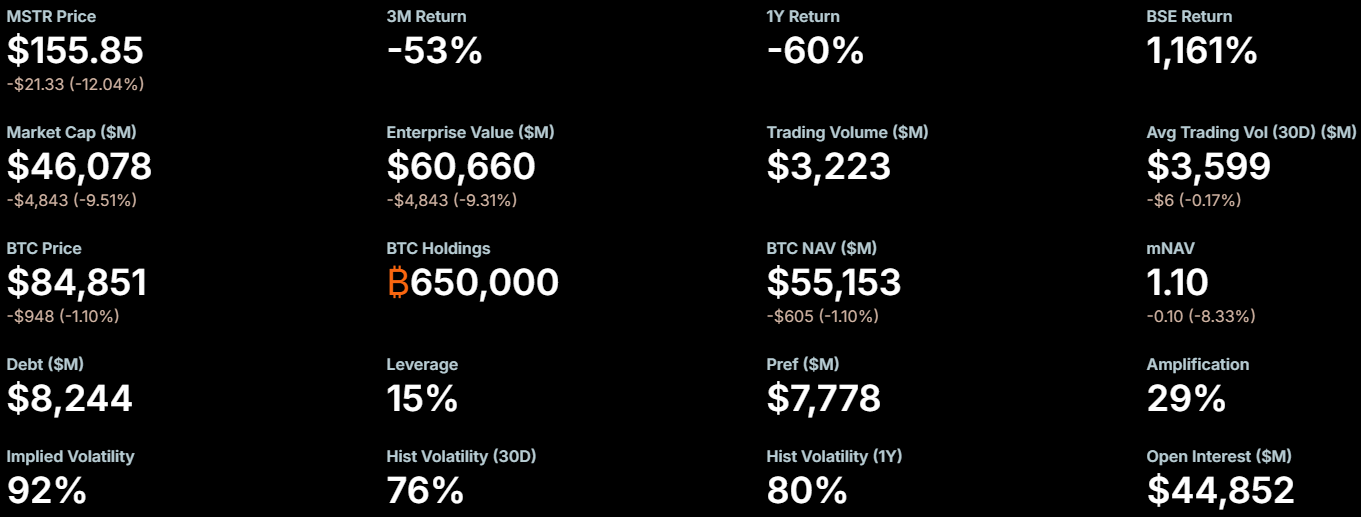

Strategy’s Current Situation

The financial newsletter The Kobeissi Letter noted that Strategy now holds approximately $55 billion worth of Bitcoin, offset by $8 billion in debt and roughly $1.4 billion in cash reserves. Despite those impressive figures, the company’s market capitalization stands at just $45 billion, implying that investors are pricing in a substantial level of risk.

Strategy’s Current Situation (as of Dec. 1, 2025) | Source: @KobeissiLetter on X.

In effect, the market is valuing MicroStrategy at less than the net worth of its Bitcoin holdings — a striking signal of skepticism toward the company’s highly leveraged crypto strategy.

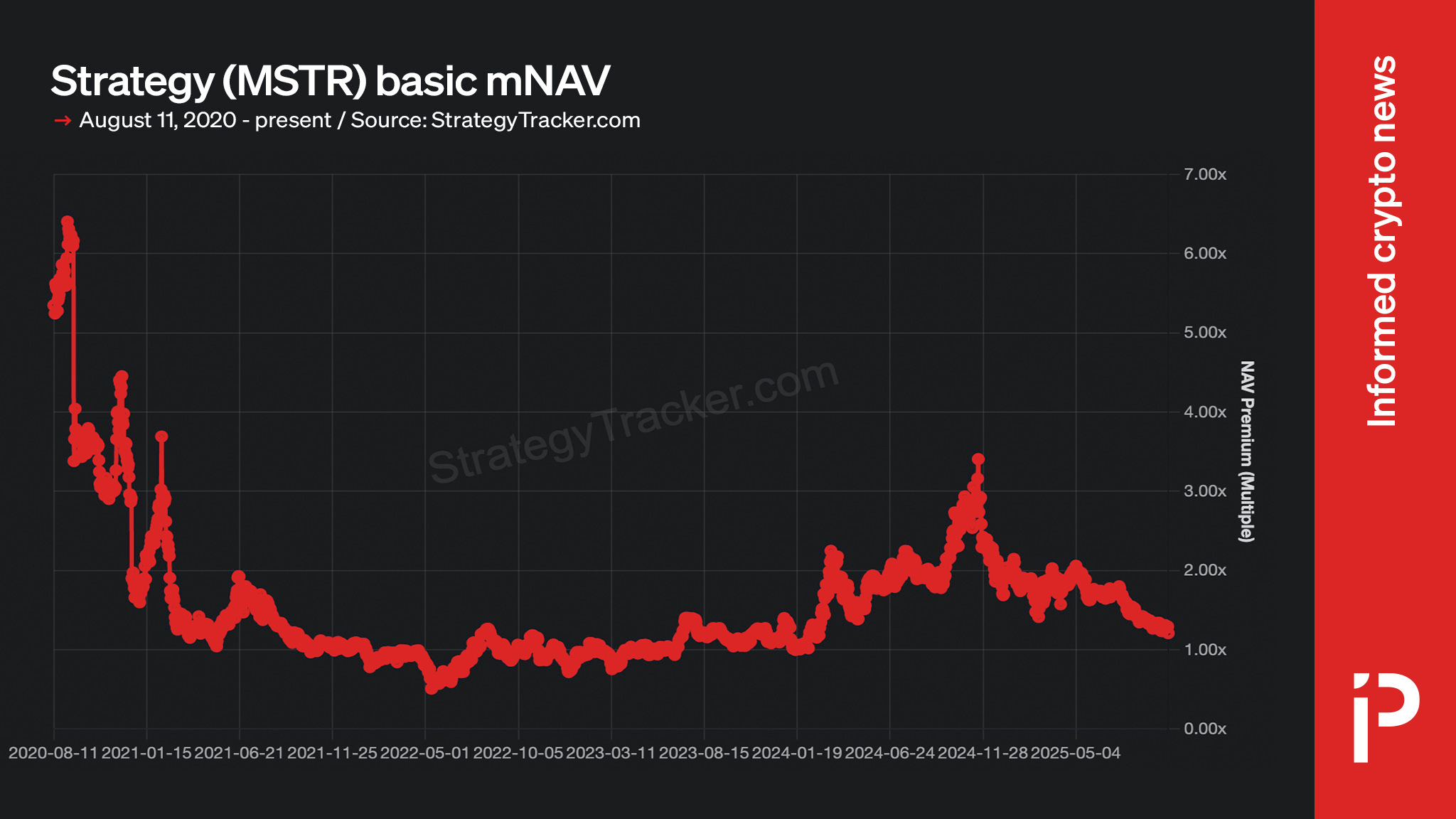

Understanding mNAV: The Key Metric Driving Strategy’s Risk and Value

Before diving into the controversy surrounding Strategy’s liquidity risks, it’s essential to understand the metric at the center of the debate: mNAV, or market Net Asset Value. This single number determines whether Strategy can continue its aggressive Bitcoin-acquisition model, or whether the company may eventually be forced to sell the very asset it built its identity around

As volatility rises and investor confidence wavers, mNAV has become the pressure gauge everyone is watching.

Strategy (MSTR) basic mNAV. | Credit: Protos

mNAV = Strategy’s market cap ÷ value of its Bitcoin holdings

mNAV > 1 = The market values Strategy above the worth of its Bitcoin.

mNAV < 1 = Strategy trades below the value of its Bitcoin treasury.

This ratio is the lifeblood of Strategy’s business model. When mNAV is high, the company can easily raise new capital through stock or preferred issuances to buy more Bitcoin. But when mNAV falls toward 1, or worse, below it, the entire engine breaks down.

As of December 2025, Strategy’s mNAV has slipped to 0.9-1.0, meaning:

The market now values the entire company at or below its Bitcoin holdings.

Raising fresh capital becomes far more difficult.

Continued Bitcoin accumulation risks severe dilution to shareholders.

A sustained discount could undermine Strategy’s ability to meet its fixed obligations.

Analysts warn that mNAV “nearly vanished” in late 2025 for the first time in almost two years. If it drops further, some believe it could activate what they’re calling “the kill-switch scenario,” where Bitcoin sales become mathematically unavoidable.

Strategy Confirms Bitcoin Sale Option as Liquidity Risks Rise

For years, Saylor’s mantra was absolute: “We will never sell our Bitcoin.”

But on Nov. 29, 2025, CEO Phong Le quietly introduced a new possibility during an interview: if Strategy’s market cap falls below its Bitcoin value and the company cannot raise capital, it may sell high-basis Bitcoin to fund preferred dividends.

The company reinforced this message with a Dec. 1 announcement of a $1.44 billion USD reserve, created from stock sales, to cover 21 months of preferred dividends.

Preferred shareholders depend on yields that “will never be paid long-term.”

The system relies entirely on new inflows—classic Ponzi dynamics.

If liquidity dries up, a “death spiral” could begin as investors dump securities.

Additionally, in Schiff’s view, the firm’s decision to sell stock not to buy more Bitcoin, but to raise U.S. dollars to cover interest and dividend payments, signals the collapse of its narrative. He argues that Strategy’s entire model, using equity and debt financing to maintain its Bitcoin position, has finally buckled under its own weight.

Peter Schiff on MSTR and Michael Saylor. | Source: @PeterSchiff on X.

“This is the beginning of the end,” Schiff has said, contending that the stock is broken, the business model unsustainable, and Michael Saylor’s strategy a form of financial sleight of hand. To Schiff, this isn’t innovation but illusion: a company propped up by hype and leverage, now forced to turn back to the fiat system it once scorned.

Scott McClintic, Crypto Analyst

McClintic warned Strategy is: “A financial pyramid that feeds on itself.”

He said lenders are “asking to fail” because the model only works if Bitcoin continues to rise.

The company behaves like a leveraged Bitcoin ETF with a software company attached.

For critics, the admission that BTC might be sold is not a prudent backup plan; it’s validation that the model is unstable.

Is Strategy (MSTR) the Next LUNA or the Ultimate Bitcoin Stress Test?

That disconnect has fueled speculation about what might happen if Bitcoin’s price were to stumble again.

“It’s hard not to see echoes of the past here,” said Sandeep Nailwal, co-founder and CEO of Polygon, who compared MicroStrategy’s position to the LUNA collapse of 2022. “If things turn, we could see another public, Wall Street–retail–entangled death spiral. Let’s hope Saylor can pull some magic out of his hat.”

Sandeep Nailwal on Saylor’s Bitcoin bet. | Source: @sandeepnailwal on X

Nailwal’s concern isn’t isolated. Critics have long warned that Strategy’s heavy leverage, combined with its near-total dependence on Bitcoin’s performance, creates systemic risk, particularly given its status as a publicly traded company.

Among the more vocal skeptics is market commentator Jacob King, who argues that CEO Michael Saylor has built a fragile narrative around Bitcoin as a corporate reserve asset. King accuses Saylor of hypocrisy, noting that after years of dismissing fiat currency, Strategy is now increasing its U.S. dollar reserves in response to Bitcoin’s volatility.

“The same people who called fiat worthless are now relying on it to survive,” King said. “It’s the ultimate contradiction.”

Strategy’s strategy has undeniably elevated Saylor into one of the most visible figures in corporate crypto adoption. But it has also tied the company’s fate tightly to Bitcoin’s fortunes, a bet that looks brilliant in bull markets and terrifying in downturns.

Michael Saylor, as I’ve been saying for years, is the biggest fraudster to crawl out of the Bitcoin hype machine.

After years of him and the Bitcoin maxis trashing fiat, he’s now launched a fund that buys USD as its reserve asset because Bitcoin is sliding to new lows and…

As the crypto market once again swings between optimism and uncertainty, the question remains: is Strategy a visionary pioneer proving the long-term case for Bitcoin, or is it a ticking time bomb whose unraveling could ripple across both Wall Street and Main Street?

Why Supporters Say Strategy (MSTR) Is a Visionary Bitcoin Play

On the other side are analysts, crypto maximalists, and institutional investors who see Strategy as a pioneering digital-asset treasury.

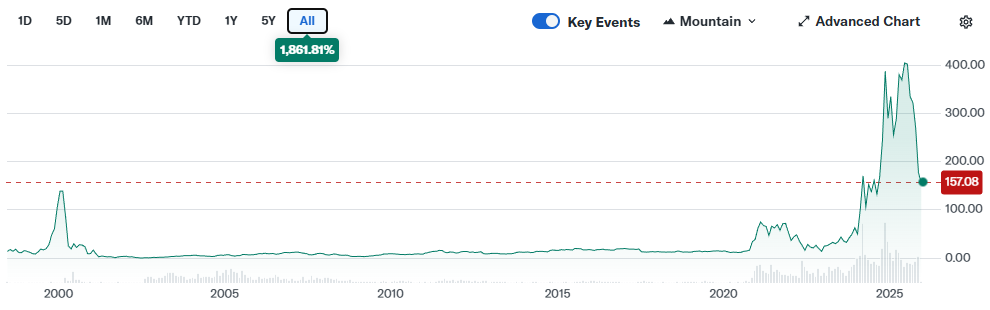

2024-early 2025 bull markets pushed MSTR to near $550 (all-time highs).

By November 2025, the stock dropped to $180-200, down by 70% from highs.

Bitcoin, by comparison, dropped only by 10-15% in 2025.

MSTR stock price performance since its debut in New York. | Credit: Yahoo! Finance

Strategy (MSTR) Stock Performance — 2025 Timeline

Here’s a rough 2025 timeline of Strategy (ticker MSTR), summarizing major stock-price moves from January through November (with December’s early info), and key events.

Month (2025)

Approx. Closing Price (USD)

Notes

January

334.79

Strong start to the year; optimism around Bitcoin accumulation.

February

255.43

Sharp dip from January; volatility increases as crypto market softens.

March

288.27

Partial rebound as investor sentiment stabilizes.

April

380.11

Strong rally driven by renewed optimism and Bitcoin price strength.

May

369.06

Minor pullback but stock remains elevated.

June

404.23

Year-to-date high; market bullish on MicroStrategy’s Bitcoin holdings.

July

401.86

Stability near peak levels; confidence in strategy continues.

August

334.41

Noticeable correction as broader crypto sentiment turns cautious.

Steep drop; pressure builds from macro factors and Bitcoin weakness.

November

175–177

Significant sell-off; investors price in heightened risk.

December (early)

52-week range shows a low near $166.01 and high near $457.22 (though peak was early 2024)

Shares near yearly lows; market remains wary of leverage and volatility.

This divergence highlights the mNAV collapse. When the premium is gone, the stock behaves like: Bitcoin × leverage × investor fear.

Preferred shares tell a similar story: yields spiked to 10-15% while prices slid to multi-year lows, showing investor uncertainty about the sustainability of payouts.

Is Strategy (MSTR) Really a Ponzi Scheme? A Look at the Business Model

It does not promise fixed returns to stockholders or guarantees of the Bitcoin price.

It fully discloses its financing mechanisms.

Its assets (Bitcoin) are real, liquid, and independently valued.

A more accurate label is: A hyper-leveraged Bitcoin holding company with ETF-like characteristics.

So Strategy’s model is risky, but not necessarily fraudulent.

Why Strategy (MSTR) Is Unique

Strategy stands out as a publicly traded company functioning like a leveraged Bitcoin ETF, yet retaining the flexibility of a traditional corporation. Unlike typical software firms, its balance sheet is dominated by Bitcoin, which it actively accumulates using a mix of debt issuance and equity sales. This hybrid model makes MSTR a bridge between Wall Street’s capital markets and the crypto ecosystem.

While critics compare its structure to a Ponzi scheme, but rather than fraud, the risk lies in market exposure and leverage: if Bitcoin prices fall sharply or liquidity dries up, MSTR’s model strains under its own weight.

Still, its approach is a rare experiment, a corporate entity using traditional finance tools to create a high-beta proxy for Bitcoin, blurring the line between a tech stock and a crypto asset vehicle.

Can Strategy (MSTR) Withstand a Bitcoin Price Decline?

The company now faces its most vulnerable moment since 2021:

Strategy Inc. is a publicly traded company that has made Bitcoin its primary treasury asset. Since 2020, it has raised capital through stock and high-yield preferred shares to purchase Bitcoin, effectively giving investors exposure to BTC via a regulated corporate structure.

What is mNAV and why is it important?

mNAV, or market Net Asset Value, is the ratio of Strategy’s market capitalization to the value of its Bitcoin holdings. An mNAV above 1 indicates the company trades at a premium to its Bitcoin, allowing it to raise capital to buy more BTC. An mNAV below 1 signals risk, as the market values the company less than its crypto holdings, potentially forcing BTC sales to meet obligations.

Why did Strategy announce a possible Bitcoin sale for the first time?

In November 2025, CEO Phong Le said that if Strategy’s market cap falls below its Bitcoin value and the company cannot raise new capital, it may sell high-basis Bitcoin to cover preferred dividends. This marks a shift from Michael Saylor’s long-standing “never sell” policy and reflects a focus on liquidity and risk management.

Is Strategy a Ponzi scheme or fraudulent?

Critics have called it “Ponzi-like” because it relies on new capital inflows to fund Bitcoin purchases and preferred dividends. However, Strategy fully discloses its financing methods and holds real Bitcoin assets, so it does not meet the legal definition of a Ponzi scheme. It is better described as a hyper-leveraged Bitcoin holding company.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy