What S&P’s ‘B–’ Rating Means for Strategy and the Future of Bitcoin-Backed Credit

Share

Key Takeaways

Strategy raised $2.521 billion through Stretch (STRC), a new perpetual preferred instrument backed by Bitcoin launched on July 21, 2025 (announcement of IPO).

Stretch offers a 9% target yield, monthly dividends and built-in price control mechanisms to maintain stability around $100.

Stretch sits above Stride, Strike, and MSTR equity, but below Strife and senior debt in the capital stack.

While engineered for low volatility, Stretch still carries risks tied to Bitcoin price, structural complexity and market trust.

Record-breaking earnings. A pioneering capital stack and now, a new financial instrument pushing the boundaries of Bitcoin-backed credit.

In Strategy’s most recent quarter, Strategy reported record earnings, outlined its capital structure, and introduced a new Bitcoin-backed credit instrument.

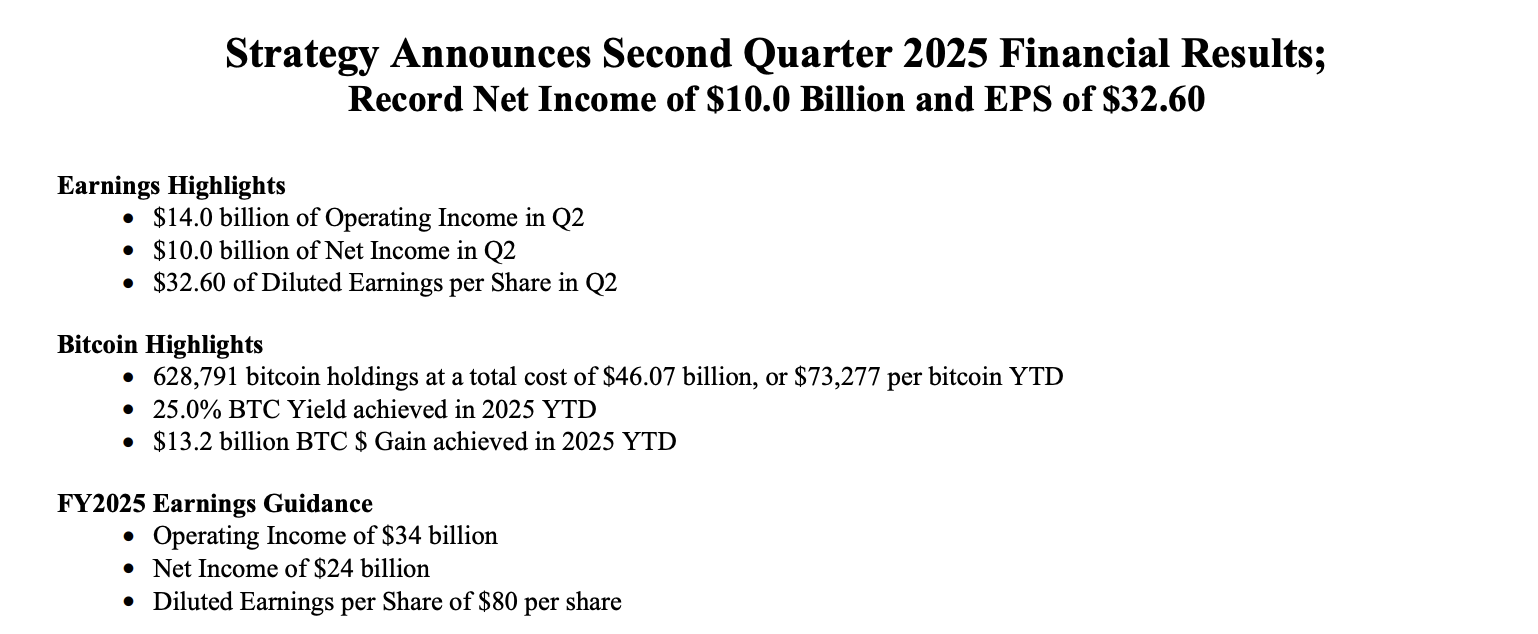

In Q2 2025, Strategy didn’t just disclose $14 billion in operating income and $10 billion in net income, it reasserted its dominance in the digital asset ecosystem by closing a $2.521 billion raise through its newly launched perpetual preferred security, Stretch (STRC), part of a $2.8 billion offering.

Under the leadership of Executive Chairman Michael Saylor and CEO and President Phong Le, Strategy’s latest offering goes beyond a typical funding mechanism. Stretch reflects a broader shift in corporate crypto-finance, toward structured instruments, managed risk exposure and tiered capital strategies backed by Bitcoin reserves.

This article unpacks what Stretch is, where STRC sits, why STRC matters and the mechanics behind one of the most important Bitcoin-backed instruments ever issued. The company describes Stretch as the least volatile Bitcoin-backed credit instrument it has issued to date, aiming to offer steadier returns within a market known for sharp swings.

Financial Results Strategy Second Quarter 2025| Source Strategy

Stretch Explained: A New Kind of Preferred Equity for a New Class of Investor

Stretch is a structured preferred equity instrument positioned at a specific level within Strategy‘s capital stack, intended to serve a different segment of credit-focused investors.

Here’s what defines Stretch:

Perpetual structure: Stretch has no maturity date, aligning with Strategy’s vision of long-term capital flexibility.

Monthly dividend: Unlike previous issuances, Stretch pays dividends every month, offering smoother cash flow for short-duration credit investors.

9% dividend: Stretch launched with a targeted 9% annual dividend, with the effective yield increasing to as much as 10% when issued at a discount.

Variable dividend model: The dividend can adjust monthly to keep share price anchored near $100, reducing secondary market volatility.

Target audience: Designed for short-duration, yield-seeking investors, an alternative to money market funds and short-term treasuries.

Stretch is designed to offer greater price stability than Strategy’s previous preferred instruments, while incorporating a more actively managed, variable dividend structure to influence market pricing.

Stretch Preferred Stock | Source: Strategy

Mechanisms for Stability: How Stretch Keeps Price Near $100

Stretch is engineered not only for yield, but also price stability. The team revealed three key levers Strategy will use to keep the instrument anchored close to its par value of $100.

Monthly dividend adjustment: By raising or lowering the dividend monthly, Strategy keeps the share price near par rather than letting it drift with market forces.

ATM (at-the-market) issuance program: Strategy uses the ATM program to respond to market pricing by selling more when prices are strong and holding back when prices are weak, in order to help keep Stretch trading near $100.

Embedded call option: If the share price exceeds its upper band, Strategy reserves the right to call the security, resetting the price mechanically.

Stretch Design | Source: Strategy

Stacked Strategically: Where Stretch Fits in Strategy’s Capital Pyramid

Stretch enters Strategy’s balance sheet as the fourth perpetual preferred instrument but the exact placement is key to understanding its risk.

Above common equity and subordinate preferreds: Stretch sits senior to Strike, Stride and all common stock, providing relative security in a downturn.

Below strife and convertible debt: It remains junior to the firm’s fixed-income obligations and top-tier preferred.

BTC rating of 7: Strategy assigns Stretch a proprietary overcollateralization score of 7x covered by the company’s BTC holdings at launch.

Engineered for low volatility: Saylor explicitly stated that this is Strategy’s proposed least volatile credit product, contrasting with the high-beta nature of MSTR equity. Strategy (MSTR) is considered high-beta because:

MSTR moves much more than the general market

MSTR is heavily tied to Bitcoin’s price, which is itself highly volatile

MSTR often swings double-digit percentages on Bitcoin news or movements

Analysts and traders often treat MSTR as a proxy for leveraged Bitcoin exposure, with the stock engineered to behave like Bitcoin on steroids.

Capital reinforcement through junior layers: Issuing additional junior instruments like Stride strengthens the perceived creditworthiness of Stretch by layering subordinate capital beneath it, improving STRC standing in the capital structure and increasing its appeal to credit-focused investors.

With these placements and interdependencies, Stretch is a middle-layer instrument built to be dependable but still exposed to underlying BTC volatility.

Strategy Capital Structure | Source: Strategy

The Bitcoin Collateral Behind Stretch (STRC)

In general, no credit instrument is worth more than its collateral. In Strategy’s case, the backbone is 628,791 Bitcoin, the world’s largest corporate BTC reserve.

Some information on the BTC collateral supporting the credit include:

$73 Billion in Bitcoin Holdings: As of August 7, 2025, Strategy’s BTC stack forms the core asset base backing all securities.

14× asset coverage ratio: Strategy reported that its assets, primarily Bitcoin, cover outstanding debt by a factor of 14, signaling a substantial collateral buffer for creditors.

180 Years of preferred dividend coverage: Current reserves could pay dividends for almost two centuries without new income.

Downside resilience: Even with a 75% BTC drawdown, Strategy says it could continue to fund 26 years of preferred dividends.

Interactive BTC Rating Model: Investors can calculate risk using Strategy’s public model, adjusting BTC price, volatility and time horizon.

This level of transparency, combined with collateral scale, is what separates Strategy from imitators.

Bitcoin Coverage | Source: Strategy

The Investor Profile: Who Stretch Is Designed For

Stretch was designed to appeal to conservative credit investors seeking stable, yield-generating exposure, rather than speculative retail buyers or equity-focused holders.

Money market alternative: With $7 trillion parked in money markets, Stretch offers an appealing substitute at nearly 10% yield.

Short-duration investors: Unlike long-term bonds or equities, Stretch is engineered for short-term holders who want price stability.

Monthly payout cadence: Designed to mimic familiar fixed-income products with frequent income.

Lower volatility profile: Unlike MSTR stock, Stretch appeals to investors allergic to daily price swings.

BTC enthusiasts seeking credit exposure: For those bullish on Bitcoin but wary of holding spot assets, Stretch provides collateralized exposure.

This positioning opens Strategy’s instruments to entirely new pools of capital and potentially new levels of liquidity

Capital Structure Under the Microscope

While Strategy’s multi-layered capital stack has been praised for its ingenuity, some analysts and investors see potential drawbacks. Concerns generally focus on transparency, dependence on Bitcoin’s price and the structural complexity that comes with overlapping instruments.

Complex for non-specialists: The layered structure can make it harder for inexperienced BTC investors to assess true risk.

BTC dependence: While Strategy appears confident in its Bitcoin-backed approach, some investors may question stability during price swings.

Aggressive issuance: Frequent capital raises spark questions about timing and necessity.

These points don’t diminish the innovation in Strategy’s approach but highlight potential pressure areas, especially if Bitcoin’s four-year cycle pattern changes or fails to repeat.

Why is the four-year cycle dead?

1) The forces that have created prior four-year cycles are weaker:

i) The halving is half as important every four years;

ii) The interest rate cycle is positive for crypto, not negative (as it was in 2018 and 2022);

Michael Saylor outlined a broader strategy for evolving BTC-backed capital markets not just launching Stretch, but laying the groundwork for long-term structural refinement.

Reducing convertible debt reliance

Strategy appears to be pursuing a gradual shift away from senior convertible debt by incrementally replacing it with equity-like instruments as opportunities arise.

While there’s no set timeline, the approach suggests a longer-term aim to streamline the capital structure and reduce leverage over time.

Perpetual capital strategy

Saylor reinforced that all preferred instruments remain perpetual, without redemption or maturity designed for ongoing recapitalization rather than traditional refinancing.

Ongoing ATM issuances across the stack

Stratregy confirmed that the company will continue issuing instruments across the preferred tiers to fund operations, purchase more Bitcoin, and support dividend obligations demonstrating a self-reinforcing stacking mechanism.

Overview of Strategy Preferred Stock | Source: Strategy

Stretch’s Boundaries: Where Challenges Could Arise

Despite the design precision, Stretch, like any financial product, carries real risks. Investors must weigh these before jumping in.

Bitcoin price risk: A sharp decline in BTC, beyond 80–95%, could erode asset coverage across the capital stack, potentially disrupting dividend payments.

Structural complexity risk: The layered and interconnected design of Strategy’s capital instruments could magnify financial stress during periods of extreme market volatility, making outcomes harder to predict or manage.

Dividend adjustment risk: Income-seeking investors may dislike monthly changes to dividend rates.

Trust-based stability risk: The effectiveness of price stabilization mechanisms depends on market confidence. If investors lose faith in Strategy’s ability to manage the system, pricing could disconnect from intended targets.

These aren’t dealbreakers, but they highlight that Stretch, while elegantly constructed, carries layers of complexity that demand close attention.

Conclusion

Stretch is another capital raise and a sophisticated financial instrument designed to stabilize yield, minimize volatility and offer deep BTC-collateralized exposure for institutional credit buyers.

Michael Saylor and Strategy have moved beyond holding Bitcoin. Strategy is now building an entire yield curve around it. Whether Stretch becomes the benchmark for BTC-backed credit or a precarious middle layer in an over-structured pyramid, will depend on Bitcoin’s long-term trajectory, investor confidence, and market liquidity.

For now, Stretch stands as both a powerful tool for capital and a test case in the evolution of decentralized corporate finance. However, investors should always proceed with caution.

What makes Stretch different from Strategy’s previous preferred instruments?

Stretch introduces a variable monthly dividend, embedded price control mechanisms, and targets short-duration, yield-focused investors — unlike prior fixed-dividend offerings like Stride or Strike.

How does Strategy plan to manage the price of Stretch (STRC) near $100?

Strategy adjusts the dividend monthly, uses an ATM issuance program to manage supply and has an embedded call option to reset pricing if it trades too far above par.

Is Stretch a safer investment than MSTR stock or Bitcoin itself?

Stretch is structured to be less volatile than MSTR equity and offers defined yield backed by BTC. However, it’s still exposed to Bitcoin price fluctuations and the complexity of Strategy’s layered capital model.

Why is Strategy using a perpetual capital model instead of traditional debt?

Perpetual instruments like Stretch allow Strategy to recycle capital continuously without redemptions, reducing refinancing pressure and aligning with long-term Bitcoin accumulation goals.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Andrew Kamsky is a chart analyst and writer with a background in economics and ACCA certification. He has held roles at a Big Four firm, a fintech bank, and a listed bank specializing in currency hedging. His work explores Bitcoin, macro trends, and market structure. Outside finance, he's passionate about music, travel, and neon design.

Easy

Easy