Johns Hopkins economist Steve Hanke calls Bitcoin ‘zero fundamental value,’ sparking debate on BTC price. | Credit: CCN.com

Share

Key Takeaways

Johns Hopkins economist Steve Hanke calls Bitcoin “zero fundamental value.”

For Hanke, price spikes and crashes reflect market sentiment rather than underlying economic fundamentals.

Traditional economists measure fundamental value through earnings or productive output.

The debate highlights the broader tension between traditional finance metrics and emerging digital assets.

In December 2025, Steve Hanke, a professor of applied economics at Johns Hopkins University, renewed his long-standing criticism of Bitcoin (BTC), declaring that the world’s largest cryptocurrency has “zero fundamental value.”

Hanke’s remarks reignited a debate over how Bitcoin should be evaluated, whether its price accurately reflects its real economic worth, and what this means for investors and the future of Bitcoin’s price action.

Understanding this controversy requires unpacking what economists mean by ‘fundamental value,’ where Bitcoin fits within traditional financial theory, and why supporters and critics arrive at such starkly different conclusions.

In financial theory, an asset’s fundamental value refers to the worth of that asset based on tangible economic factors, such as cash flows, earnings, dividends, or utility, and its ability to generate income or serve a basic economic function.

Stocks, for example, can be valued through discounted future earnings; bonds through interest payments and principal repayment. Commodities like oil or agricultural products have demand tied to concrete uses.

Currencies issued by governments derive value from legal status, macroeconomic frameworks, and the trust underlying a national monetary system.

Critics of Bitcoin argue that it lacks these traditional anchors:

No cash flows or earnings stream.

No central authority guarantees its use.

No inherent productive utility.

Above all, they maintain that Bitcoin’s price exists because people agree it has value, not because it produces or delivers something directly measurable in economic terms.

This is the foundation of Hanke’s position: Bitcoin is “a highly speculative asset with zero fundamental value.”

Hanke’s Critique: Bitcoin as Speculation, Not Value

Hanke’s latest comments reflect a skepticism that has been present for many years. In his view:

Bitcoin’s price volatility makes it unreliable as money or a stable store of value.

It fails the criteria of a “legitimate currency,” lacking the stability and widespread use necessary for transactional reliability.

Price spikes and crashes, in his framing, are symptoms of speculative behavior, not underlying economic utility.

These criticisms come at a time when Bitcoin’s price had recently experienced a downturn from earlier 2025 highs, a context that, in Hanke’s view, underscores the disconnect between speculative trading and durable value.

Steve Hanke claims BItcoin has no fundamental value. | Credit: Steve Hanke X profile

Hanke has also extended his critique beyond Bitcoin’s market price. He opposes policy proposals, such as a U.S. strategic Bitcoin reserve. He has warned that national experiments with Bitcoin as legal tender (such as in El Salvador) could destabilize economies and exacerbate inflation.

From Hanke’s standpoint, allocating investment capital, including corporate treasuries, into Bitcoin is figuratively akin to roulette rather than a prudent financial strategy.

Bitcoin’s Fundamental Value Debate Explained

It might seem counterintuitive that an asset with no fundamental value can trade at such elevated price levels. BTC has traded well above $80,000 in 2025, even after significant corrections.

Critics argue that this highlights the speculative nature of its valuation: the price is driven by supply and demand, rather than fundamental cash flows.

However, proponents of Bitcoin reject the notion that price alone defines value. They argue that:

Value need not derive from earnings or cash flows: Some assets are valuable because people ascribe value to them; this applies to fiat currencies, precious metals like gold, and even certain collectibles.

Store of value and scarcity matter: Bitcoin’s fixed supply cap of 21 million coins introduces scarcity, which supporters argue can lend it store-of-value characteristics similar to gold, despite lacking physical substance.

Utility beyond price:Bitcoin offers decentralized settlement, censorship resistance, and borderless transferability, functional traits that proponents see as real economic utility, even if difficult to quantify in traditional financial models.

One academic criticism of the zero-value framing is that price behavior alone isn’t enough to assert worthlessness.

Econometric research, for example, suggests that marginal cost of production models (linking price to mining costs) can offer bounds on value, implying that prices gravitate toward levels not entirely unmoored from economic principles.

Although this academic work isn’t universally accepted as definitive, it stands as an example of how researchers try to apply quantitative frameworks to a new asset class.

Critics Push Back: Bitcoin’s Price History Tells a Different Story

Critics of the critics have been vocal on social platforms and in financial circles, arguing that proclamations of Bitcoin’s imminent collapse have proven inaccurate in the past.

A notable example comes from a tweet referenced by Director of Bitcoin Strategy at Semler Scientific Joe Burnett: “Steve, are you okay? Bitcoin is up 22,795% since you suggested that the ‘Bitcoin bubble will pop’ over 10 years ago.”

Joe Burnett criticized Hanke. | Credit: Joe Burnett X profile

This quote highlights how some skepticism, even from well-known economists, failed to predict the extraordinarily long-term price appreciation Bitcoin has experienced over more than a decade.

Another iconoclastic critic, Steve Hanke himself, has been mocked for his frequent bearish calls, including the infamous bubble pop tweets from 2015.

Supporters of Bitcoin argue that such comments, while technically accurate in identifying volatility or speculative trading, miss the broader narrative of long-term adoption and price resilience.

Indeed, Bitcoin critics often note that history tends to favor markets responding to demand and adoption, even in the absence of traditional fundamentals, a phenomenon not unique to Bitcoin but familiar in other speculative assets.

Why Bitcoin’s Fundamental Value Debate Matters for Investors

For individual and institutional investors, the question of fundamental value isn’t just academic. It influences:

Risk assessment: If an asset truly lacks fundamental value, its price could be more sensitive to changes in market sentiment, macroeconomic conditions, and regulatory developments. That could increase volatility and risk.

Valuation models: Traditional valuation models, like discounted cash flow (DCF) analysis, aren’t easily applicable to Bitcoin. Investors must turn instead to non-traditional indicators, such as network activity, adoption rates, or on-chain metrics.

Portfolio strategy: Some investors treat Bitcoin like a high-beta speculative asset, allocating only a small percentage to it. Others treat it as digital gold, a non-correlated buffer or inflation hedge. These strategies reflect differing views on whether Bitcoin’s price is based on real economic value or evolving speculative consensus.

Regulatory impacts: Statements like Hanke’s can shape how regulators, institutions, and pension funds perceive Bitcoin. Critics argue that a lack of fundamental backing may discourage traditional investment flows; supporters counter that evolving infrastructure and adoption mitigate these concerns.

Reconciling Two Perspectives and Debate Over Bitcoin’s Fundamental Value

There is a middle ground between saying Bitcoin has no fundamental value and assuming it can grow indefinitely with no constraints. Economists and analysts frame Bitcoin’s value based on:

Network effects: Like social platforms, the value of Bitcoin’s network may grow with increased participation.

Utility as settlement infrastructure: Even without cash flows, Bitcoin enables peer-to-peer settlement without the need for intermediaries.

Store of value narratives: While debated, many investors view Bitcoin as a hedge against monetary debasement.

Critics, such as Hanke, focus on the lack of intrinsic, quantifiable economic value, while proponents argue that value is subjective and context-dependent in financial markets.

This philosophical divide is central to understanding why Bitcoin elicits such polarized opinions.

So What Does This Mean for BTC Price?

Because fundamental value is subjective in the case of Bitcoin, predicting price based on intrinsic economic factors becomes challenging. Here’s what different interpretations imply:

Market sentiment, institutional entry, and macro trends could support higher price levels over time.

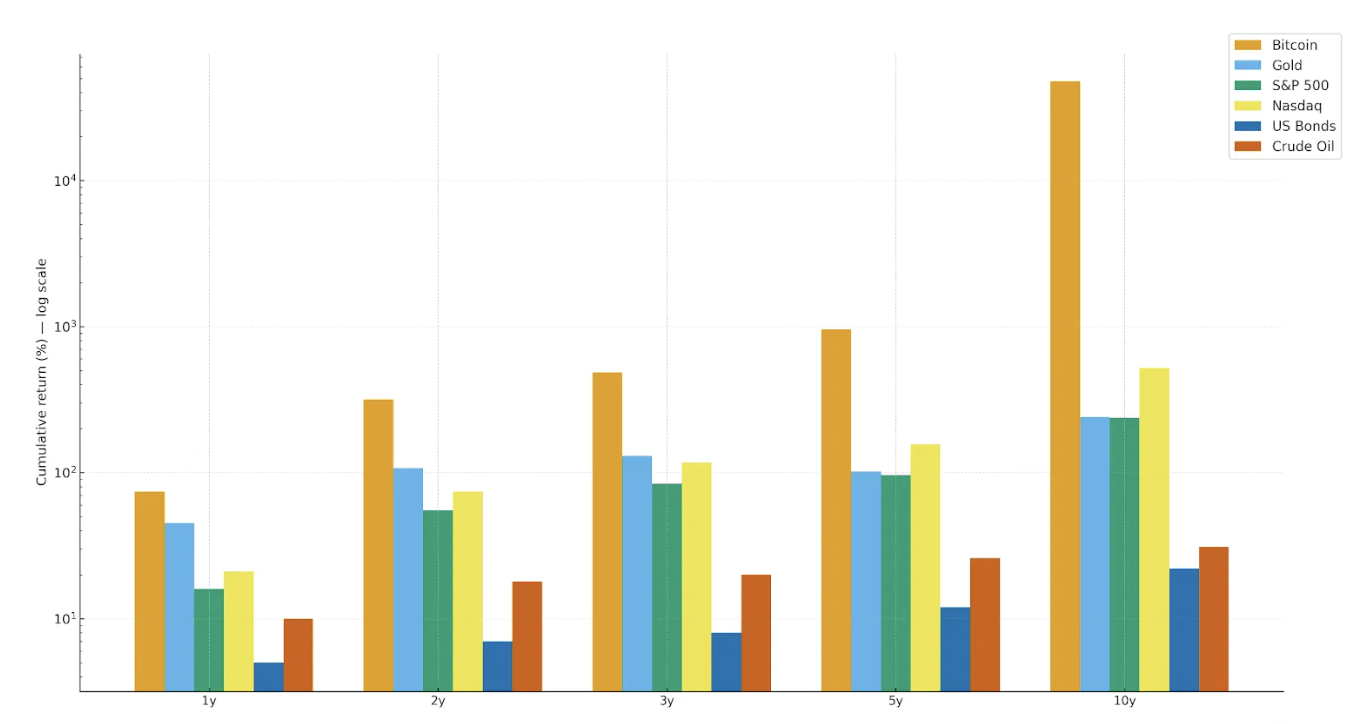

Bitcoin vs. other assets. | Credit: Breez

Value is More Than Fundamentals

Steve Hanke’s assertion that “Bitcoin has zero fundamental value” echoes a long tradition of skepticism among traditional economists reluctant to classify Bitcoin as money, a productive asset, or a reliable store of value.

However, Bitcoin’s market history, marked by dramatic price appreciation and growing adoption, illustrates that value in financial markets is not determined solely by traditional fundamental metrics. While Bitcoin may lack intrinsic economic outputs, such as cash flows, its utility, network effects, and role as a digital asset contribute to price formation driven by demand.

For investors, the key takeaway isn’t whether Bitcoin is fundamentally valuable in a textbook sense, but whether they understand what drives its price, the risks involved, and how it fits into broader financial goals.

Different theoretical frameworks lead to varying price expectations, which is why debates like this matter.

The future price of Bitcoin will not only reflect technical adoption and macroeconomic forces, but also how markets continue to reconcile belief, utility, and value in the emerging digital asset class.

What does “Bitcoin has no fundamental value” mean?

It means Bitcoin does not generate cash flows, earnings, or dividends like stocks or bonds, nor does it have state backing like fiat currencies. Critics argue its price is based on speculation rather than intrinsic economic value.

Who made this claim and why does it matter?

Steve Hanke, a Johns Hopkins economist, has repeatedly stated that Bitcoin has zero fundamental value. His views matter because they reflect mainstream economic skepticism and influence institutional, regulatory, and policy discussions around crypto.

If Bitcoin has no fundamental value, why does it have a high price?

Bitcoin’s price is driven by supply and demand, scarcity (a fixed 21 million supply), network adoption, and investor belief. Many assets, including gold and fiat currencies, derive their value largely from collective trust rather than cash flows.

Can Bitcoin be valued using traditional models?

Traditional valuation models like discounted cash flow don’t work well for Bitcoin. Analysts instead use alternative metrics such as network activity, adoption rates, mining costs, and on-chain data to estimate value ranges.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy