Bitcoin doesn’t trade on 20M coins, but just on 3M available on exchanges. Here’s how marginal supply and spot demand really drive BTC price. | Credit: CCN.com

Share

Key Takeaways

Bitcoin’s price is determined by the marginal inventory, not by the total mined supply.

Out of 19.99 million mined coins, about 13.48 million are considered illiquid and rarely move.

Markets move based on the small portion of supply actively being bought and sold, not long-term holders sitting in cold storage.

Futures and leverage can temporarily push quotes around, but sustained trends require real spot buying.

When people talk about Bitcoin, they often say something like: “There are almost 20 million coins in circulation.”

As of Feb. 25, 2026, that’s technically true. Roughly 19.99 million BTC have been mined.

But here’s the part most people miss: Bitcoin does not trade on 20 million coins. It trades on something much smaller, something far more fragile. It trades on the marginal inventory. And that number is closer to 3 million coins.

Understanding this changes how you think about Bitcoin price, volatility, supply shocks, ETF flows, short squeezes, and even long-term valuation.

Let’s break it down from first principles.

Bitcoin Circulating Supply vs Tradable Supply: Why 20 Million BTC Is Misleading

Here’s the current breakdown:

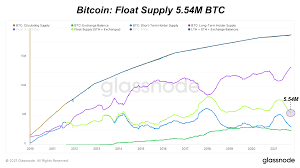

Total mined supply: 19.99 million BTC

Illiquid supply (rarely moves): 13.48 million BTC

Bitcoin sitting on exchanges: 3.02 million BTC

That 3.02 million BTC sitting on exchanges is the inventory pile. That’s what’s actually available for immediate buying and selling.

The other 13.48 million coins? They’re largely held by long-term holders, cold storage wallets, institutions, people with lost keys, and those who simply aren’t selling.

Bitcoin float supply. | Credit: Glassnode

They exist, but they are not part of the daily float.

This is the difference between headline supply and adequate supply. Markets move on effective supply.

What Is Marginal Inventory in Bitcoin and Why It Moves the Price?

In any market, price is set at the margin.

That means the price you see on your screen isn’t determined by all holders: it’s defined by the small group actively willing to transact at that moment.

If only 3.02 million BTC are sitting on exchanges, that’s the inventory from which:

Bitcoin doesn’t need 20 million coins to move the price. It only needs pressure on the tradable float. And that float is thin.

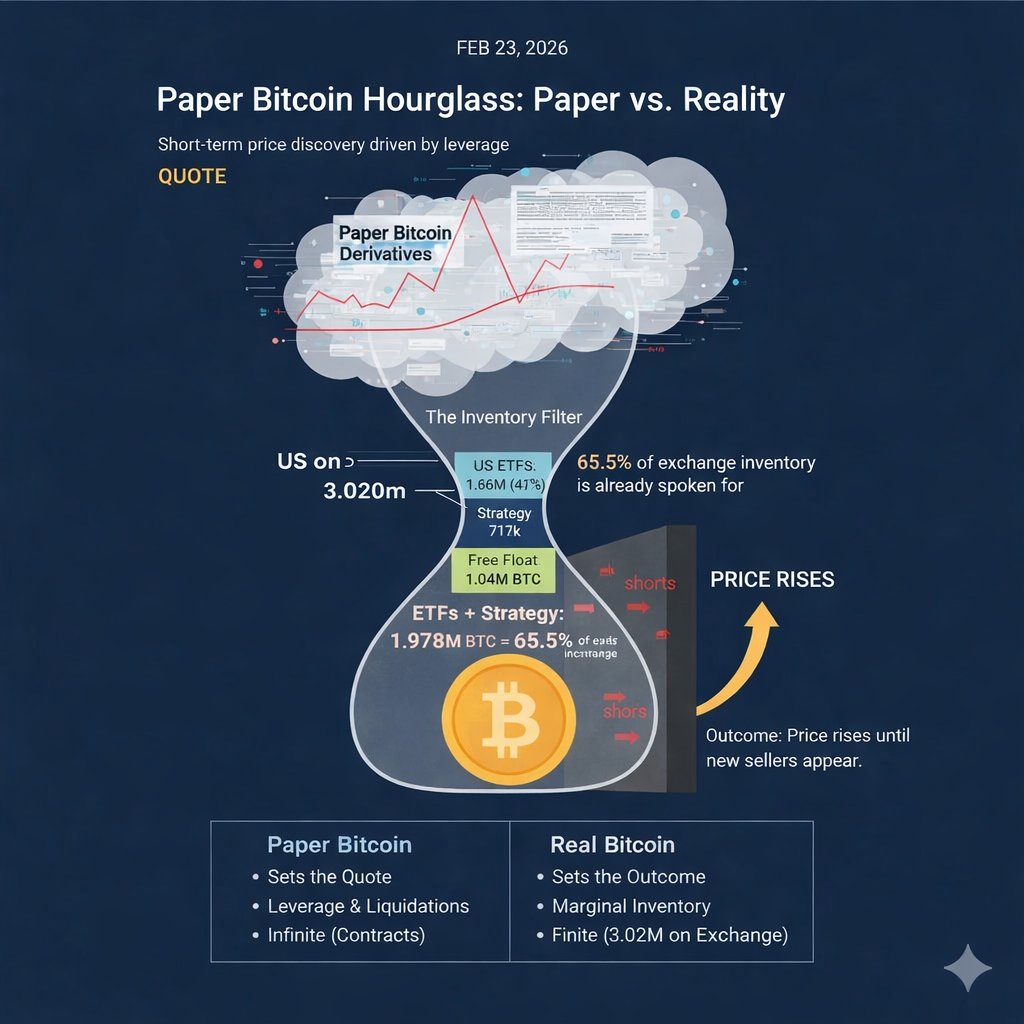

Bitcoin ETFs, Strategy (MSTR), and Exchange Liquidity: Who Controls the Available BTC Supply?

Now here’s where it gets interesting.

U.S. spot Bitcoin ETFs collectively hold approximately 1.26 million BTC. Michael Saylor’s Strategy holds 713,502 BTC. Combined, that’s about 1.97 million BTC. Compare that to the 3.02 million BTC sitting on exchanges.

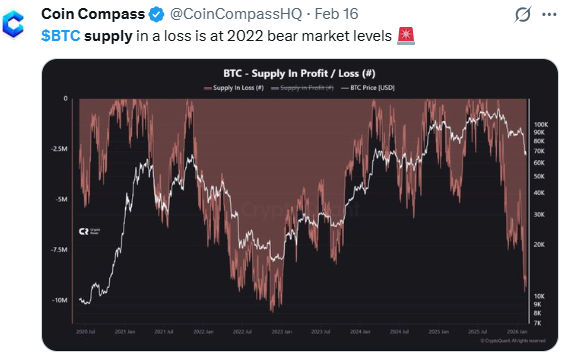

BTC supply in a loss is at 2022 bear market levels. | Credit: Coin Compass X profile

That means: ETFs + Strategy equal roughly 65% of all exchange inventory.

Let that sink in.

Two categories of buyers, i.e., passive ETF demand and one aggressive corporate accumulator, account for nearly two-thirds of the tradable supply sitting on exchanges.

That’s not the total supply. That’s the available liquidity pile. This concentration matters because price doesn’t care about dormant coins.

It cares about available ones.

Paper Bitcoin vs Real Bitcoin: How Derivatives Impact BTC Price Action

Here’s where derivatives come in.

Bitcoin futures, perpetual swaps, and options allow traders to speculate on price without owning actual BTC.

Paper Bitcoin hourglass: paper vs. reality. | Credit: David Eng X profile

But derivatives do not create real supply. They make synthetic exposure. If someone shorts Bitcoin using futures, they haven’t borrowed actual BTC from cold storage. They’ve entered a contract. And every short position represents something important: A future buyer.

Eventually, shorts must close. Closing a short means buying back. And where do those coins come from? That same 3.02 million BTC exchange pile.

Paper can influence the quote. But real Bitcoin sets the outcome.

Short-term price swings are often driven by leverage. Liquidations cascade. Funding rates flip. Open interest expands and contracts.

But sustained trends require something different. They require net spot demand.

Spot demand means real buyers purchasing actual Bitcoin and removing it from exchange liquidity.

If ETFs absorb coins, those coins leave exchanges. If corporations accumulate, those coins leave exchanges. And if long-term holders withdraw to cold storage, that shrinks the sellable float.

That 3.02 million BTC is not evenly distributed either. Some belongs to market makers. Some sits in inactive accounts. And some is resting liquidity far above current price.

Which means the true immediate sellable float is even thinner than the headline exchange number.

When demand surges, price must rise until new sellers are incentivized to appear.

This is how upside squeezes happen. A thin float meets aggressive bids. Price moves violently.

Why Every Bitcoin Short Position Eventually Becomes a Market Buy Order

This concept is simple but powerful. If a trader shorts Bitcoin, he’s promising to buy it back later. Even if that’s via a derivative, the net effect on price depends on spot flows over time.

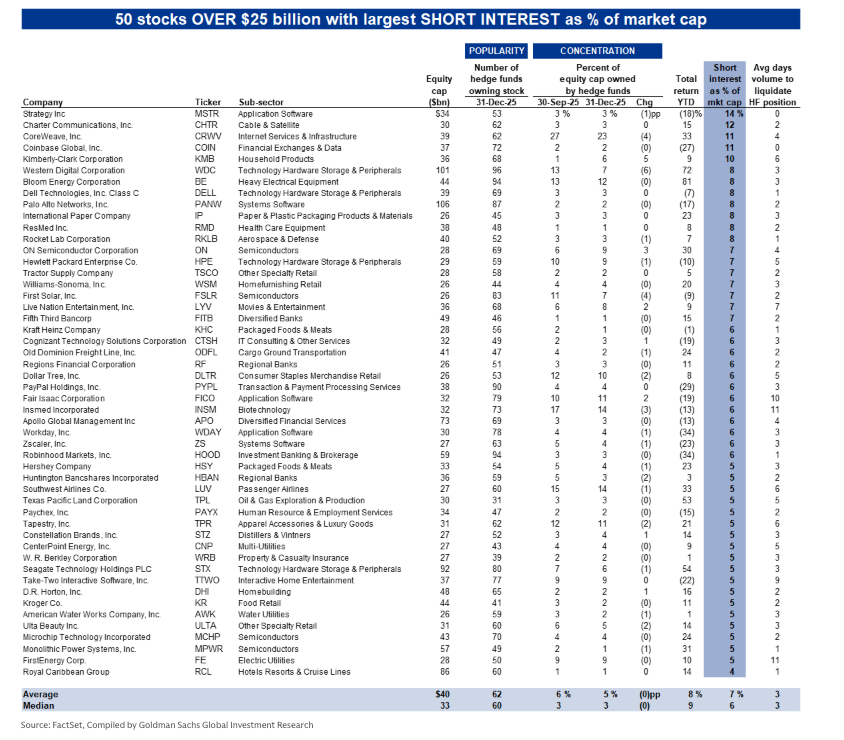

Most shorted stocks. | Credit: FactSet

If leverage washes out and net spot demand flips positive, shorts get trapped. And when they close, they must buy. But they’re buying from a limited pool. This is why heavy short positioning combined with tight exchange supply creates explosive setups.

Short sellers need liquidity.

If liquidity is scarce, prices gaps upward.

Bitcoin Bull Case: Supply Shock, Spot ETF Inflows, and a Potential Short Squeeze

Markets are margin-based systems. Price is set where the next buyer meets the next seller. Not where all holders agree.

Bitcoin Liquidity Risk: How Thin Exchange Balances Amplify Both Upside and Downside Moves

Thin float works both directions.

If panic selling begins and ETF flows reverse, that same limited exchange pile can be overwhelmed.

The price would fall until strong buyers absorbed the supply. Thin liquidity amplifies moves. It doesn’t guarantee upside. It guarantees volatility. That’s an important distinction.

Bitcoin Is a Liquidity Game

Bitcoin price is not a function of total supply. It is a function of available supply at the margin.

Paper Bitcoin can temporarily push the quote. But real Bitcoin, actual spot coins, determines long-term outcomes. When leverage is washed out, and net spot demand turns positive, the price must rise until new sellers emerge. That’s how supply squeezes happen.

That’s how upside breakouts accelerate.

And that’s why understanding marginal inventory is more important than repeating the “20 million coins” headline.

Bitcoin doesn’t trade on its total supply. It trades on what’s available. And what’s available is thin.

Yes. Bitcoin’s maximum supply is capped at 21 million, and about 19.99 million BTC have already been mined. But total supply is not the same as tradable supply.

What is the “real number” Bitcoin trades on?

Bitcoin effectively trades on the marginal inventory, the coins actively available on exchanges. As of Feb. 25, 2026, that’s about 3.02 million BTC, not 20 million.

What does “illiquid supply” mean?

Illiquid supply refers to Bitcoin that rarely moves or is held long-term in cold storage. Around 13.48 million BTC fall into this category, meaning they are unlikely to be sold anytime soon.

Why does exchange inventory matter so much?

Because price is set at the margin. The BTC sitting on exchanges is the pool from which buyers purchase, and sellers sell. If that pool shrinks,the price becomes more sensitive to demand changes.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy