Crypto’s next growth phase appears less driven by speculation and more defined by systems that connect digital assets with the real economy.| Credit: Hameem Sarwar /CCN

Share

Key Takeaways

Crypto infrastructure captured $2.5B in Q1 2026 as capital shifted toward stablecoin rails, custody, compliance, and tokenized assets.

Larger checks and fewer deals signal stronger investor conviction in scalable infrastructure platforms.

Stablecoin payment networks and regulated custody providers led funding activity.

Real-world asset tokenization expanded into private credit, commodities, and enterprise-grade financial products.

By mid-February 2026, crypto venture capital is telling a different story than in prior cycles.

Memecoins still trend on social media, and token launches continue, but large checks increasingly target infrastructure that institutions and enterprises can actually use: stablecoin payment rails, institutional custody, tokenized real-world assets, and compliance tooling.

Silicon Valley Bank’s 2026 outlook captured the same shift, pointing to faster enterprise adoption, a rebound in larger venture checks, and stablecoins moving deeper into mainstream payments and settlement.

The numbers support that pivot. 11 crypto companies raised $2.5B across 128 rounds in January 2026. A meaningful share came from private investment in public equity (PIPEs), debt, initial public offerings (IPOs), or post-IPO equity, so totals can vary depending on methodology.

Even so, the biggest disclosed round of the month fit the new pattern: stablecoin payments infrastructure firm Rain raised $250M at a $1.95B valuation, with ICONIQ Capital leading the round.

This article examines the top 10 crypto infrastructure companies that raised $20M or more in Q1 2026, ranked by disclosed funding size.

It explains how stablecoin payments, custody, tokenized real-world assets (RWA), and compliance platforms are driving the shift toward enterprise-grade blockchain infrastructure and institutional crypto adoption.

1. Rain’s $250M Series C Signals Enterprise Shift Toward Stablecoin Payment Infrastructure

Stablecoin rails led Q1 funding activity, with Rain topping the list as investor appetite for payment infrastructure accelerated.

Led by ICONIQ Capital (known for backing Adyen and Snowflake), according to the company’s release.

What it Builds

Branded card issuance.

Digital dollar accounts.

Global on- and off-ramps through a single API.

Rain reports roughly $3B in annualized transaction volume, positioning the firm among the largest enterprise-focused stablecoin infrastructure providers.

The rise reflects growing conviction that stablecoins are evolving from trading tools into payment and settlement infrastructure for global businesses.

As payment rails expand, institutional adoption still depends on secure custody, compliance controls, liquidity management, and regulatory clarity.

2. BitGo Raises $212.8 M in IPO as Institutional Custody Demand Accelerates

BitGo ranked among the largest funding events of Q1, underscoring continued institutional demand for regulated crypto infrastructure.

Public listing reflects transition from private infrastructure provider to publicly traded custody platform.

What it Builds

Institutional custody.

Wallet infrastructure.

Staking services.

Support for exchange-traded funds (ETFs) and exchange-traded products (ETPs).

BitGo manages more than $104 billion in digital assets across 9.3M wallets, according to the company.

JUST IN: BitGo, "the #1 custodian and staking provider, with over $104B in platform assets, and over 9.3M wallets created," integrates $USDA. "Institutions on BitGo can now deposit and withdraw USDA directly from BitGo wallets, a major milestone for Anzens and #Cardano$ADA." pic.twitter.com/d9kp9gMQjH

The IPO signals investor confidence in regulated custody platforms that serve asset managers, funds, and institutional clients as digital assets integrate further into traditional finance.

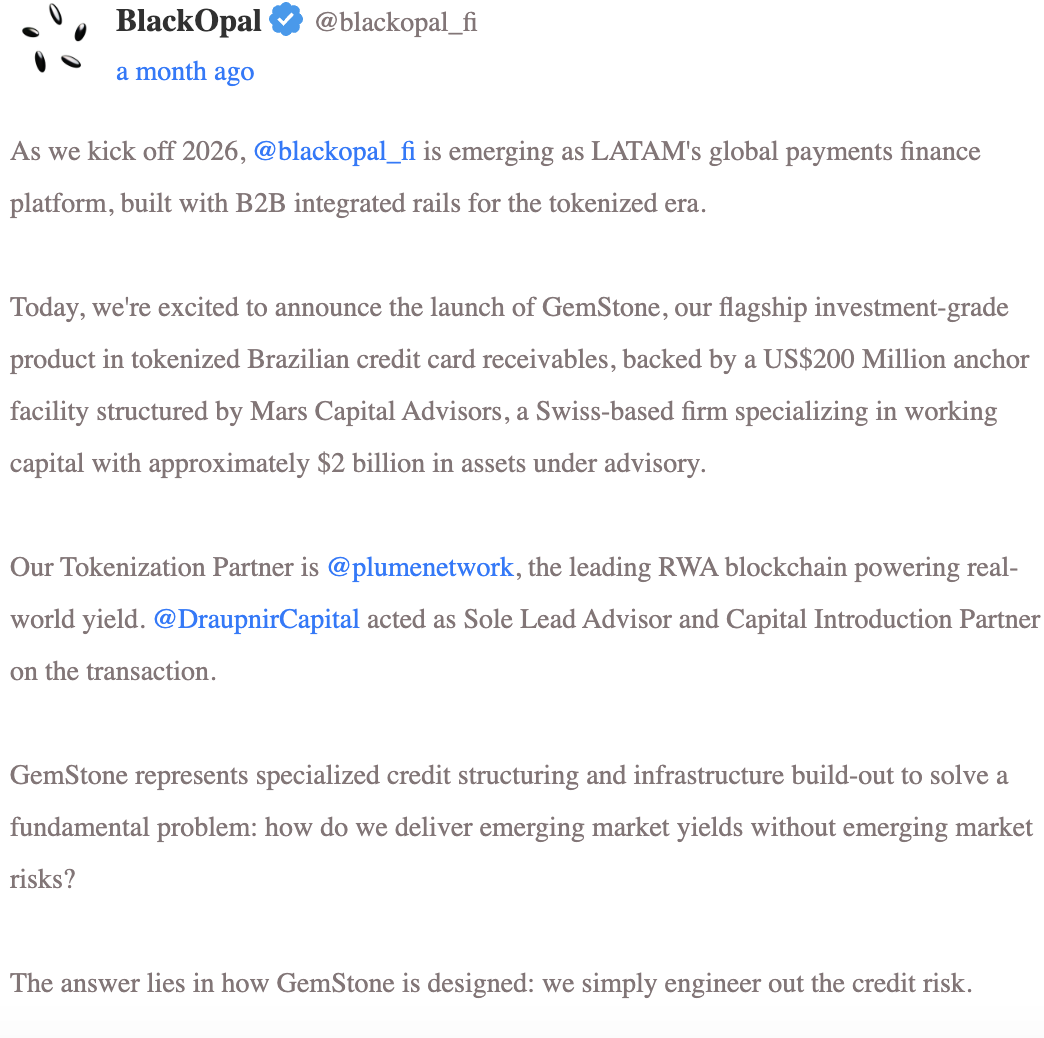

3. BlackOpal Secures $200M Facility to Expand Tokenized Receivables in Latin America

BlackOpal ranked among Q1’s largest alternative financing rounds, reinforcing investor interest in real-world asset tokenization across emerging credit markets.

Round Details

$200 million structured facility.

Arranged by Mars Capital Advisors.

What it Builds

Tokenized receivables financing.

BlackOpal focuses on tokenizing credit card receivables and invoices across Latin America, targeting Brazil’s $750 billion credit card market, according to the company.

BlackOpal | Source: twstalker

The raise highlights how real-world asset (RWA) tokenization is expanding into private credit markets, connecting blockchain infrastructure with traditional receivables financing.

4. Alpaca Raises $150M to Scale Embedded Brokerage and Trading APIs

Alpaca emerged as one of Q1’s largest infrastructure raises, reflecting continued demand for API-driven brokerage technology across fintech platforms.

Alpaca’s APIs allow fintech companies to embed trading for stocks, options, and crypto, alongside real-time market data, according to the company.

The funding underscores investor conviction that API infrastructure can power multiple financial products across platforms, generating diversified revenue streams beyond single consumer-facing applications.

5. GOLD.com Secures $150M From Tether to Expand Tokenized Gold Infrastructure

GOLD.com joined Q1’s major funding rounds as tokenized commodities gained momentum alongside stablecoins and private credit.

GOLD.com integrates vaulting, minting, and token issuance with blockchain-based trading and lending services, according to the company.

The capital injection expands tokenized real-world assets beyond government securities, signaling broader institutional appetite for blockchain-based exposure to commodities such as gold.

6. LMAX Group Secures $150M From Ripple to Advance Stablecoin Settlement

LMAX Group closed one of Q1’s notable strategic investments as institutional players strengthened infrastructure for foreign exchange and digital asset markets.

Institutional foreign exchange (FX) and crypto trading infrastructure with stablecoin settlement.

LMAX delivers regulated liquidity and execution services for professional traders, according to the company.

The funding underscores growing institutional trust in stablecoin settlement as a core infrastructure layer for cross-border trading, liquidity management, capital efficiency, and 24-hour market access.

7. Anchorage Digital Secures $100M From Tether to Expand Regulated Crypto Banking

Anchorage Digital added to Q1’s institutional funding momentum as regulated crypto banking platforms attracted strategic capital.

Anchorage holds a U.S. federal trust charter, according to the company.

Its platform integrates regulated custody with compliance controls required by institutional clients, reinforcing demand for federally chartered digital asset banks that support secure storage, staking participation, governance execution, and regulatory oversight.

8. Superstate Raises $82.5M Series B to Expand Compliant Tokenized Fund Infrastructure

Superstate closed one of Q1’s notable Series B rounds as institutional investors increased exposure to regulated tokenization platforms.

Superstate operates as a registered investment adviser, enabling tokenized funds and securities on public blockchains, according to the company.

The funding reflects institutional demand for programmable financial products backed by established regulatory frameworks, combining blockchain efficiency with investor protections, compliance standards, transparency requirements, and traditional fund structures.

9. Mesh Raises $75M Series C to Scale Cross-Chain Crypto Payments Network

Mesh secured one of Q1’s prominent Series C rounds as investors backed infrastructure connecting fragmented blockchain ecosystems.

Round details

$75 million Series C.

Led by Dragonfly.

What it Builds

Cross-chain crypto payments network.

Mesh’s APIs link wallets and payment providers, enabling instant settlement across chains alongside integrated anti-money laundering (AML) compliance, according to the company.

The funding highlights continued demand for payments infrastructure that reduces friction between ecosystems, improves interoperability, strengthens compliance, and supports broader digital asset adoption.

10. TRM Labs Raises $70M Series C to Expand On-Chain Risk Intelligence Platform

TRM Labs closed one of Q1’s strategic infrastructure rounds as compliance technology gained importance across digital asset markets.

Round Details

$70 million Series C.

Led by Blockchain Capital and Goldman Sachs.

What it Builds

On-chain risk intelligence.

Forensic analytics.

Compliance tooling.

TRM’s platform provides transaction monitoring and sanctions screening for institutions and governments, according to the company.

The rise reflects how risk intelligence, forensic tracing, compliance automation, and sanctions screening have become mandatory infrastructure for regulated digital asset markets.

Crypto Funding Shifts Toward Core Infrastructure as Institutional Conviction Deepens

Q1 2026 reflects a decisive allocation of capital toward fundamental crypto infrastructure. Stablecoin rails captured the largest share of funding.

Custody platforms advanced into public markets. Real-world assets expanded beyond government debt into private credit and commodities. Compliance tooling solidified its role as a requirement for institutional participation.

Deal count declined, yet average deal size increased, signaling stronger conviction in scalable infrastructure rather than speculative applications.

If stablecoins integrate into mainstream commerce, if tokenized assets reshape capital markets, and if institutions continue expanding into digital assets, these firms will form the backbone of that shift.

Crypto’s next growth phase appears less driven by speculation and more defined by systems that connect digital assets with the real economy.

FAQs

What was the largest crypto funding round in January 2026?

Rain, a stablecoin payments infrastructure firm, led the month with a $250 million Series C at a $1.95 billion valuation.

Is BitGo a public company now?

Yes. BitGo completed an IPO in January 2026, raising $212.8 million and listing on the NYSE under the ticker BTGO.

What is the “stablecoin payment volume” reported by Rain?

Rain reports facilitating over $3 billion in annualized transaction volume for over 200 partners, including Western Union.

Which company is tokenizing Latin American credit card receivables?

BlackOpal secured a $200 million facility in Q1 2026 to expand tokenized receivables, specifically targeting Brazil’s credit market.

Who are the major investors backing these infrastructure raises?

Prominent firms include ICONIQ Capital (Rain), Goldman Sachs (TRM Labs), and Tether (GOLD.com and Anchorage Digital).

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Lorena Nessi is an award-winning journalist and media technology expert with 15 years of experience in digital culture and communication. Based in Oxfordshire, UK, she combines academic insight with hands-on media practice.

She holds a PhD in Communication, Sociology, and Digital Cultures, and an MA in Globalization, Identity, and Technology.

Lorena has taught at Fairleigh Dickinson University, Nottingham Trent University, and the University of Oxford. She is a former producer for the BBC in London, with additional experience creating television content in Mexico and Japan.

Her research focuses on digital cultures, social media, technology, capitalism, and the societal impact of blockchain innovation.

She has written extensively on digital media and emerging technologies, with her work featured in both academic and media platforms. Her Web3 expertise explores how blockchain technologies shape culture, economics, and decentralized systems.

Outside of work, Lorena enjoys reading science fiction, playing strategic board games, traveling, and chasing adventures that get her heart racing. A perfect day ends with a relaxing spa and a good family meal.

Easy

Easy