Bernstein reiterates its $150,000 Bitcoin price target for 2026, arguing the current downturn is the “weakest bear case” in BTC’s history. | Credit: CCN.com

Share

Key Takeaways

Bernstein maintains a $150,000 Bitcoin price target, calling the recent 45% correction the “weakest bear case in history” due to strong underlying fundamentals.

Institutional demand is reshaping the market, with ETFs and structured products like STRC bringing in long-term, less volatile capital.

Bitcoin is outperforming traditional safe havens, gaining 8% during geopolitical tensions while gold has declined, strengthening its “digital gold” narrative.

A $13.5B Bitcoin options expiry makes $75,000 a key trigger level, where a breakout could spark liquidations and accelerate upside momentum.

Bitcoin’s recent price action has tested investor conviction. A roughly 45% drawdown from its October highs would, in previous cycles, have triggered widespread panic and narratives of a prolonged bear market. Yet, according to global research firm Bernstein, this time may be fundamentally different.

In a recent note, Bernstein reaffirmed its bold long-term outlook, maintaining a $150,000 Bitcoin price target while describing the current correction as the “weakest bear case in history.”

For investors trying to make sense of mixed macro signals, institutional flows, and volatile price action around the $70,000 level, the key question is clear: what exactly has changed?

This article breaks down the evolving Bitcoin thesis, spanning institutional demand, on-chain behavior, derivatives positioning, and macro context, to explain why some analysts believe the bottom may already be forming.

Why Bernstein Calls This the Weakest Bitcoin Bear Market in History

Historically, Bitcoin bear markets have been driven by structural breakdowns: exchange collapses (Mt. Gox, FTX), liquidity crises, regulatory shocks, or speculative excess unwinding across the entire ecosystem.

By contrast, the current 45% pullback lacks a clear systemic trigger. Instead, it reflects a combination of:

Bernstein argues that none of these factors undermine Bitcoin’s long-term fundamentals. In fact, the firm suggests that the current environment is characterized by continued accumulation beneath the surface, rather than capitulation.

Three Key Reasons Bernstein Still Predicts $150K Bitcoin

Bernstein’s thesis rests on three core structural drivers that remain intact despite volatility.

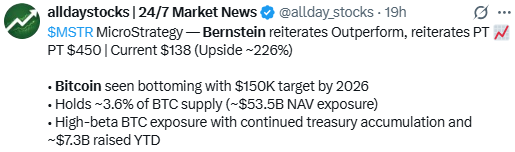

One of the most notable developments is the continued accumulation by Strategy Inc. (formerly MicroStrategy).

The company now holds 3.6% of total Bitcoin supply.

Its holdings are valued at approximately $53.5 billion.

It continues buying despite short interest and market uncertainty.

Bernstein reiterates its Outperform view and target price on MSTR. | Credit: allday_stocks X profile

This behavior is critical because it represents non-speculative demand. Unlike retail traders, Strategy operates with a long-term treasury strategy centered on Bitcoin as a reserve asset.

Even more interesting is the rise of its preferred instrument, STRC, which offers:

This signals a broader shift: Bitcoin exposure is increasingly being financialized into structured products, making it accessible to income-focused investors.

Demand is increasingly driven by wealth managers, pension funds, and sovereign entities.

This is a major departure from previous cycles, where Bitcoin demand was largely retail-driven.

ETF inflows represent sticky, long-duration capital. Unlike speculative trading flows, these allocations are often part of diversified portfolios and are less sensitive to short-term volatility.

In practical terms, this creates a structural bid under Bitcoin, reducing downside pressure during corrections.

Long-Term Bitcoin Holders Show Strong Conviction

On-chain data provides perhaps the strongest evidence for Bernstein’s bullish stance.

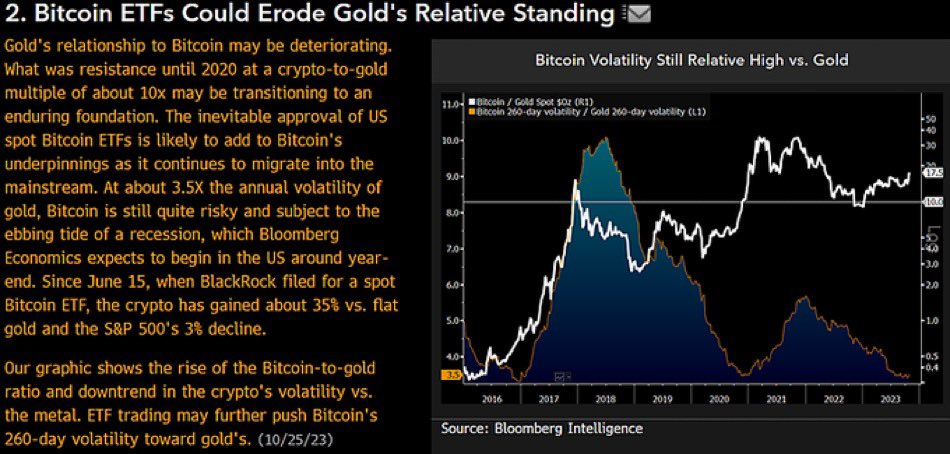

Bitcoin outperforming gold during a geopolitical crisis is significant. It suggests that:

Investors are increasingly viewing Bitcoin as a digital alternative to gold.

BTC is gaining credibility as a non-sovereign hedge asset.

While this narrative is still evolving, it reinforces the idea that Bitcoin is transitioning from a speculative asset to a macro-relevant financial instrument.

Bitcoin Price Analysis: Key Support and Resistance Levels to Watch

Despite strong fundamentals, Bitcoin’s price remains in a consolidation phase.

Key observations:

Price is hovering near the $70,000 psychological level.

Support lies around $67,500-$68,000.

Multiple EMAs are tightly clustered between $70,082-$70,755.

Resistance sits near $74,000.$76,000.

This compression suggests a coiled market, where a decisive move could trigger momentum in either direction.

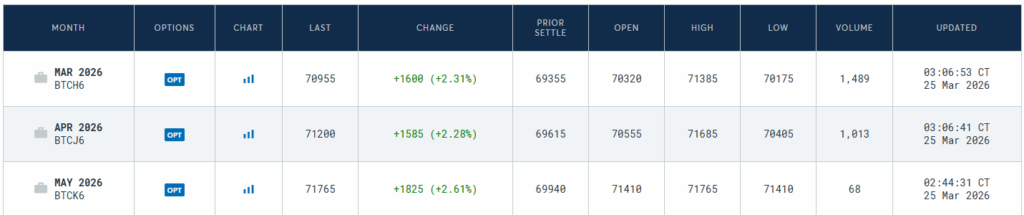

Bitcoin Options Expiry: Why $75,000 Is the Critical Price Level

One of the most important short-term catalysts comes from the derivatives market.

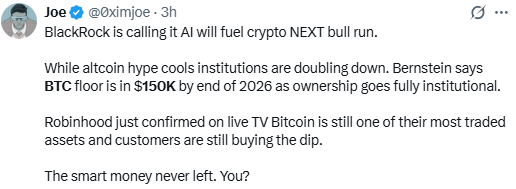

Updated (December): $150,000 by end of 2026 and potential $200,000 cycle peak in 2027

BlackRock is calling it AI will fuel crypto next bull run. | Credit: Joe X profile

The downward revision from $200,000 to $150,000 may appear conservative, but it reflects a more measured, institutional adoption curve rather than a speculative blow-off top.

How This Bitcoin Cycle Differs From Previous Bull and Bear Markets

To understand Bernstein’s confidence, it’s important to compare this cycle to previous ones.

On the other, the long-term picture appears stronger than ever:

Institutional capital continues to flow in

Long-term holders remain steadfast

Bitcoin is increasingly behaving like a macro asset

Bernstein’s $150,000 target is not just a price prediction; it reflects a broader thesis: that Bitcoin is undergoing a structural transition from speculative asset to financial infrastructure.

If that thesis holds, then the recent 45% correction may indeed prove to be what Bernstein calls it, the weakest bear case in Bitcoin’s history.

And if the $75,000 level breaks decisively, the next phase of the cycle may arrive faster than many expect.

What is Bernstein’s Bitcoin price prediction for 2026?

Bernstein currently maintains a $150,000 Bitcoin price target by the end of 2026, with the potential for Bitcoin to reach $200,000 at the cycle peak in 2027. The forecast reflects growing institutional adoption and long-term demand rather than speculative hype.

Why does Bernstein call this the “weakest Bitcoin bear case in history”?

Bernstein argues that the recent 45% Bitcoin correction lacks typical bear market triggers like exchange collapses or systemic failures. Instead, institutional inflows, strong holder conviction, and continued accumulation suggest this is a temporary pullback rather than a structural downturn.

Is Bitcoin outperforming gold as a safe haven asset?

Recently, Bitcoin has outperformed gold during geopolitical tensions, rising while gold declined. This suggests Bitcoin is increasingly being viewed as a digital store of value and alternative safe haven, though the narrative is still evolving.

Are long-term Bitcoin holders selling during the current dip?

No. On-chain data shows that around 60% of Bitcoin supply has not moved in over a year, indicating strong conviction among long-term holders who are largely ignoring short-term price fluctuations.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy