How are DATs linked to crypto crashes? | Credit: CCN.com

Share

Key Takeaways

The October flash crash exposed deep fragilities in crypto markets, with cascading liquidations and liquidity breakdowns across exchanges.

Publicly traded firms holding large crypto reserves emerged as potential amplifiers of systemic risk.

Many use debt, derivatives, or equity raises to expand Bitcoin exposure, making them vulnerable when prices fall.

Falling crypto prices reduce DAT asset values and stock prices simultaneously, triggering further selling and liquidity strain.

The October flash crash, a sudden and violent market drop that erased over $19 billion in leveraged crypto positions in just a few hours, exposed weaknesses across the digital-asset ecosystem.

Prices plunged faster than many automated systems could react, liquidations cascaded across exchanges, and liquidity evaporated from key trading pairs.

However, beyond the headlines, one group of players has drawn the attention of analysts and policymakers: Digital Asset Treasury companies, or DATs. These are publicly traded firms that hold large amounts of Bitcoin or other cryptocurrencies on their balance sheets, often utilizing leverage and capital market access to increase their exposure.

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

A Digital Asset Treasury (DAT) company, at its core, is a business that treats cryptocurrency as its primary reserve asset. Instead of focusing on producing goods or services, DATs raise funds through stock offerings, debt issuance, or credit facilities and then deploy that capital into digital assets, such as Bitcoin.

Well-known examples include Strategy in the U.S. and Metaplanet in Japan. Both companies effectively act as “public Bitcoin funds,” providing investors with a way to gain exposure to cryptocurrency without directly owning it.

Some DATs go further, engaging in yield-generating activities such as lending, selling options, or staking. These practices help generate income during calm periods but can increase risk when markets fluctuate.

In many ways, DATs resemble hedge funds or leveraged ETFs wrapped in a corporate shell. They have boards, shareholders, and reporting requirements, yet their financial health depends heavily on the price of a volatile asset.

This model performs well during bull markets, when rising cryptocurrency prices boost both their token holdings and their stock prices. But when prices fall, the same financial structure can magnify losses.

The Rise of DATs and Why They Matter

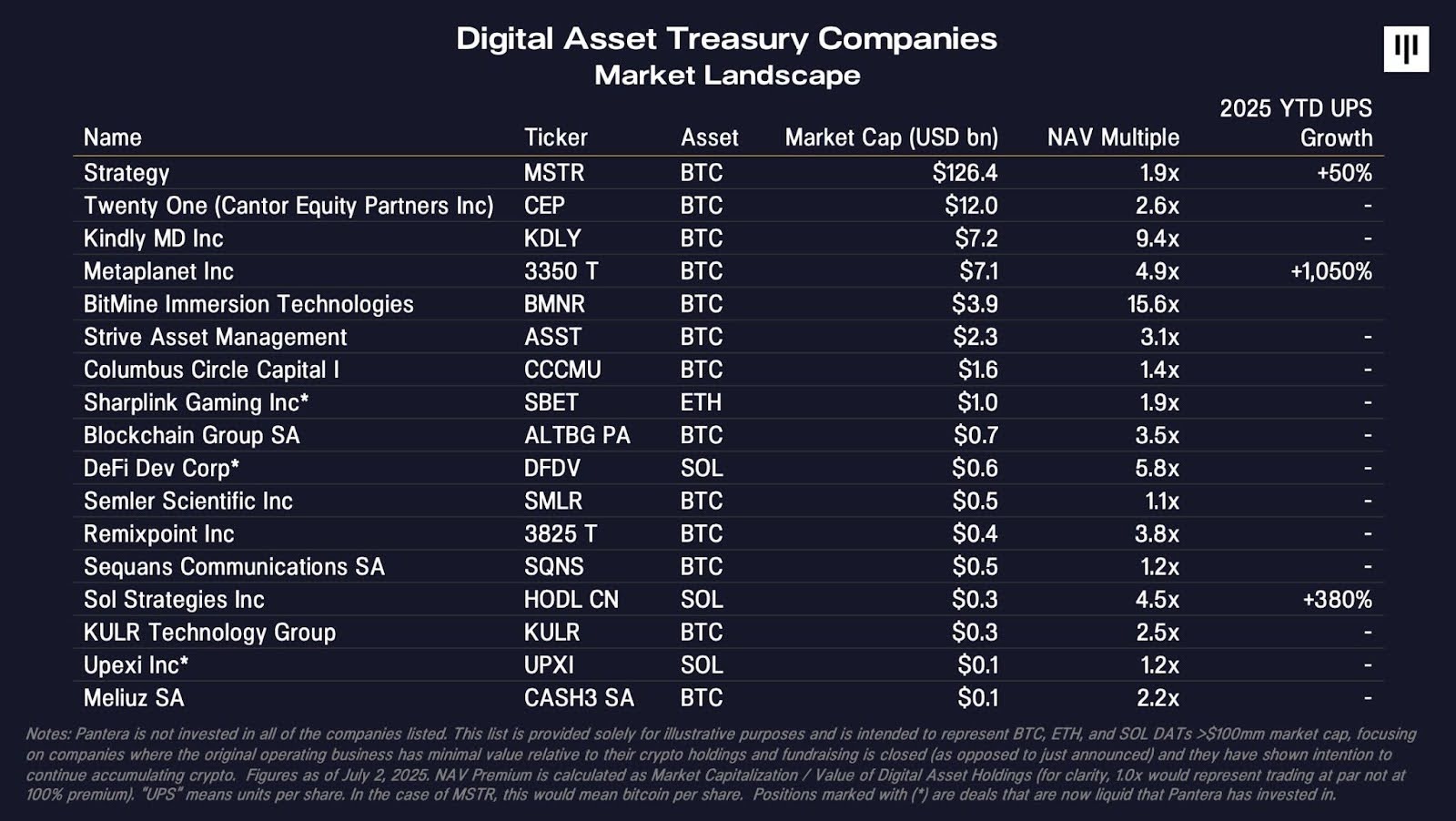

Over the past two years, the number of public and private firms holding digital assets on their balance sheets has skyrocketed. Collectively, DATs are now estimated to control tens of billions of dollars in crypto, a non-trivial share of the total market.

Major digital asset treasury companies. | Credit: Pantera

This concentration matters for several reasons:

Scale and visibility: Public DATs serve as a bridge between traditional investors and the crypto market. Their actions are closely watched, and even small announcements, such as a new Bitcoin purchase, can significantly impact sentiment and prices.

Correlation: DATs often buy and sell at similar times, responding to the same signals. When prices rise, many add exposure; when prices drop, they all face the same margin calls or investor pressure.

Feedback loops: A decline in crypto prices reduces the value of a DAT’s holdings, which may lower its stock price. Falling equity values then make it harder to raise new capital, forcing some companies to sell crypto or take on risky loans, amplifying the downward spiral.

These patterns resemble early warning signs observed in traditional finance before systemic crises: high leverage, tight interconnections, and one-sided risk exposures.

What Happened During the October 2025 Crypto Flash Crash

The October 2025 flash crash was triggered by a combination of factors, including a sharp decline in liquidity, a wave of liquidations on perpetual futures exchanges, and a temporary dislocation in several stablecoin trading pairs. Within hours, Bitcoin and Ethereum lost more than 15% of their value.

For most retail traders, the event was another reminder of crypto’s volatility. But for DATs, it revealed something more structural. Many of them rely on short-term credit lines or derivative strategies to manage exposure. When prices fall rapidly, the value of their collateral drops just as lenders demand more margin.

Bitcoin and other cryptocurrencies crashed on Oct. 10. | Credit: TradingView

Some DATs reportedly drew on emergency credit facilities or paused new purchases altogether. While few were forced to liquidate large amounts of Bitcoin, the episode highlighted the fragility of their funding models under stress. A handful of highly leveraged players selling into a thin market can inadvertently accelerate a crash.

Moreover, several DATs use covered-call or option-selling strategies to generate yield. These strategies earn small, steady returns when markets are calm but can lead to significant losses when volatility spikes. As options positions moved against them in October, some treasuries reportedly had to hedge or close contracts at unfavorable prices, which added to the overall selling pressure.

The crypto market is taking another sharp hit, with fear now at its highest level in a year. The total cap is falling fast, Bitcoin has slipped below $98,000, and momentum across the market has turned decisively bearish.

The total crypto market cap has been sliding since its $4.27 trillion peak on Oct. 4. After briefly bouncing from $3.24 trillion, the market failed to recover key levels. The drop back below $3.60 trillion turned support into resistance, and the capitalization is now breaking through its final major zones near $2.92 trillion and $2.50 trillion.

Technical indicators confirm the weakness: both RSI and MACD have flipped bearish, signaling strong downside momentum. Longer-term charts show the completion of a full five-wave cycle before an ascending-wedge breakdown—classic signs of a cycle top and the start of a broader downturn.

Bitcoin fell to around $96,000 on Nov. 14. | Credit: CoinMarketCap

Bitcoin hit $96,712, its lowest since May, mirroring the total cap’s completed five-wave pattern. BTC broke down from its own ascending wedge, confirming a likely market top.

A bearish monthly candle, RSI and MACD divergences, and a MACD bearish cross all point to more decline. The next major support area lies between $57,600 and $70,600.

The market cap of the entire crypto market has fallen harder than BTC so far, but if Bitcoin accelerates downward, the broader market could slide even faster. With key supports lost and momentum weakening across all timeframes, the data suggests the previous crypto cycle has ended, and a deeper corrective phase is underway.

When Crypto Stress Becomes Systemic: Risk Channels in DATs

Systemic risk occurs when problems at a few institutions spread across the entire system. For DATs, several potential contagion channels exist:

Balance-sheet linkages: Falling Bitcoin prices simultaneously hit DAT asset values, stock valuations, and the collateral behind any loans. This triple exposure can create a feedback loop between crypto and equity markets.

Funding strains: DATs that borrow against crypto holdings face the same “margin call” dynamics as hedge funds. If their lenders tighten collateral terms, forced sales can ripple through exchanges.

Market signaling: Because DATs are publicly traded, their actions influence sentiment far beyond their balance sheets. A single large sale or loan announcement can trigger panic among smaller investors.

Cross-asset correlation: Investors often treat DAT stocks as a proxy for crypto prices. In downturns, selling in both markets can feed on itself, tightening liquidity across the system.

Individually, these factors are manageable. Combined, they resemble the early leverage loops that once linked mortgage securities, hedge funds, and banks before the 2008 financial crisis, though on a smaller, faster scale.

Are DATs the Root Cause of Crypto Volatility in Q4 2025?

The quick answer is no. DATs didn’t cause the October crash, just as hedge funds didn’t cause every market crisis in traditional finance. The primary trigger was excessive leverage across exchanges and derivative platforms. But DATs acted as amplifiers, not initiators.

Their growing presence adds new channels for risk to move between crypto and traditional markets. For example, when a DAT’s share price collapses, investors may sell other crypto-related equities or pull funds from similar vehicles. The psychological and liquidity effects spread rapidly.

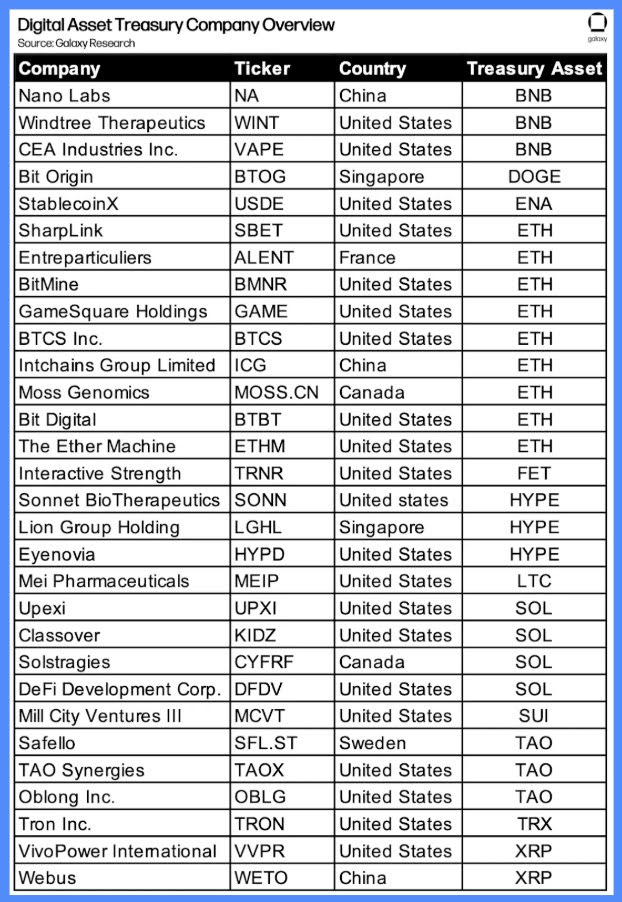

DATs overview. | Credit: Galaxy Research

It’s worth noting that not all DATs are highly leveraged or speculative. Some, such as long-term treasury models, maintain conservative balance sheets with large cash buffers.

The danger lies not in any single company but in the collective behavior of many DATs following the same high-beta strategies.

Key Lessons from the October Event for Markets and Regulators

The October event offers several lessons for both market participants and regulators:

Transparency matters: Investors and counterparties require clear information on the amount of leverage DATs are utilizing, the collateral backing their loans, and the performance of their risk models under stress.

Liquidity buffers are crucial: DATs that hold adequate cash or stable assets can avoid forced selling during sharp downturns.

Diversified income sources help stability: Relying solely on option premiums or Bitcoin appreciation is risky. A mix of yield streams reduces dependence on any single factor.

Market infrastructure needs testing: Exchanges, lenders, and custodians should coordinate stress tests simulating extreme price swings and network congestion.

“Good DATs Do Hard Things”: What Bitwise CIO Matt Hougan Says Separates Winners from Losers

In the wake of the October crash, industry voices have started to draw sharper distinctions between good and bad Digital Asset Treasury companies, and one of the most precise analyses came from Bitwise CIO Matt Hougan in a viral X thread.

Hougan argues that not all DATs are created equal. “Some should trade above NAV, others below,” he wrote, emphasizing that the difference comes down to how much real work a company is doing to justify its crypto exposure.

“Buying a crypto asset and putting it on a balance sheet today isn’t hard,” he noted. “If that’s all a DAT is doing, you’re better off owning an ETF.”

To Hougan, the firms worth paying attention to are those tackling complex structural or financial challenges, not merely buying Bitcoin, but actively innovating in how they manage, finance, or deploy it. He points to Strategy as an example of a DAT “doing something hard.”

Despite being best known for accumulating Bitcoin, Michael Saylor’ Strategy has engineered complex financing through convertible debt and preferred share issuances, allowing it to expand its holdings without dilution.

Matt Hougan intervened in the DATs/crypto crash discussion. | Credit: Matt Hougan X profile

“It’s not easy to raise $56 billion in equity capital to buy Bitcoin,” Hougan wrote. “That scale alone creates new strategic options.”

He also highlighted other “hard” areas where DATs can add value, such as writing covered calls effectively, participating prudently in DeFi, or making smart collateralized loans. These activities, while riskier, involve sophisticated treasury management that can differentiate disciplined firms from speculative ones.

“Good companies get rewarded for doing hard things well,” Hougan concluded. “Bad companies that execute poorly or take the easy route get punished. This will be true in DAT-land, too.”

How Regulation Could Help Without Killing Innovation

Regulators around the world are watching DATs more closely, but responses remain uneven. In the United States, DAT-style companies fall under securities law but are subject to few crypto-specific regulations. In Japan, regulators have begun requiring more precise accounting for digital assets and disclosure of loan terms, steps that could serve as a model.

Reasonable oversight doesn’t have to stifle innovation. Basic principles, such as transparency, capital adequacy, and the separation of customer funds from corporate treasuries, already exist in traditional finance. Extending those standards to DATs would make the ecosystem more resilient without undermining legitimate experimentation.

Another promising idea is self-regulation through industry standards. DATs could voluntarily publish standardized reserve reports, similar to proof-of-reserves disclosures by exchanges.

Independent audits of collateral, leverage ratios, and derivative exposures would help investors gauge risk before problems spread.

Why DATs Could Be the Next Bridge — or Fault Line — Between Crypto and Finance

As digital asset-linked companies become more intertwined with traditional markets, their influence on investors’ portfolios is growing rapidly. The October flash crash highlighted how risks once contained within crypto can now ripple across broader financial systems.

DATs (Digital Asset-Linked Traders) are becoming a bridge between traditional finance and crypto, linking both markets more closely than ever.

Their stocks are held in ETFs, pension funds, and retail brokerage accounts, meaning crypto market movements can now affect traditional portfolios.

The October flash crash showed how crypto volatility can spill over into mainstream equity indexes.

A margin call or liquidity issue at a major DAT could trigger wider disruptions beyond digital assets.

Investing in a DAT’s stock doesn’t mean buying Bitcoin, as it comes with added corporate leverage, operational, and regulatory risks.

Investors need to understand how these risks interact to protect themselves from unexpected market shocks.

A Growing Systemic Footprint of DATs in the Digital-Asset Economy

DATs have become an influential new layer in the digital-asset economy. By pooling billions of dollars of investor capital and leveraging it into cryptocurrencies, they’ve accelerated adoption, but also introduced new points of fragility.

The October flash crash didn’t break the system, but it revealed how interconnected it has become. DATs link public equity markets, corporate balance sheets, and decentralized exchanges in almost unthinkable ways just a few years ago.

To prevent a future crisis, the solution isn’t to ban or restrict DATs, but to acknowledge their growing systemic footprint. Stronger transparency, prudent funding rules, and better stress testing will allow the market to grow safely. Ignoring the warning signs, on the other hand, could turn the next flash crash into something much larger.

In short, DATs are not villains: they’re a symptom of crypto’s rapid maturation. However, as the October crash demonstrated, even well-intentioned innovation can create unforeseen risks. Recognizing those risks early may be the difference between a healthy digital-asset economy and the first actual systemic failure in crypto history.

A Digital Asset Treasury, or DAT, is a publicly traded company that holds cryptocurrencies, such as Bitcoin or Ethereum, as its main reserve asset. Rather than producing goods or services, DATs raise capital through stock or debt offerings and invest that money directly into digital assets.

How do DATs differ from traditional crypto funds?

DATs operate like hybrid entities, part hedge fund, part corporation. Unlike private crypto funds, they are listed on public markets and subject to corporate disclosure rules. Their stock gives investors indirect exposure to crypto without needing to hold the assets themselves.

What happened during the October 2025 flash crash?

In October 2025, crypto markets saw a sudden $19 billion liquidation of leveraged positions within hours. Prices of Bitcoin and Ethereum fell over 15%, liquidity vanished, and automated trading systems failed to keep up, leading to cascading liquidations across exchanges.

How were DATs affected by the flash crash?

Many DATs faced margin pressure as their crypto collateral dropped in value. Some were forced to draw on emergency credit lines or unwind derivatives positions. Although few sold large amounts of Bitcoin, the event exposed how vulnerable their funding models are to rapid market declines.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy