Ripple Now Holds 75+ Global Licenses: Can XRP Capture 14% of SWIFT’s $150T Market by 2030?

Share

Key Takeaways

RLUSD’s $1.40 billion market cap is a strategic milestone, not just a growth metric.

RLUSD serves as a stable unit of account and settlement asset, while XRP functions as a liquidity bridge between currencies and systems.

RLUSD’s adoption highlights how stablecoins are moving beyond trading tools into payments, treasury management, and cross-border settlement.

Network throughput, liquidity efficiency, and integration into enterprise flows matter more than retail holder counts or speculative demand.

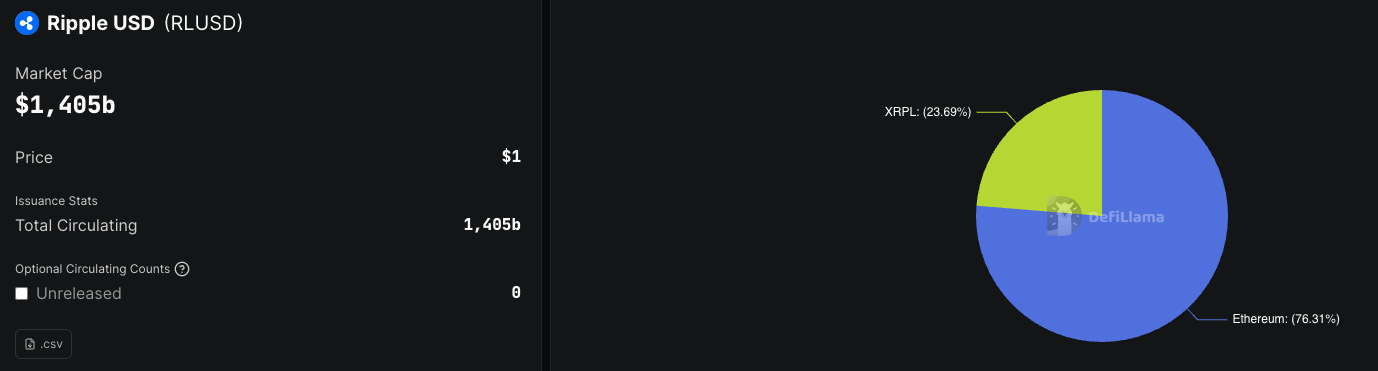

Ripple’s U.S. dollar-backed stablecoin, RLUSD, has quietly crossed a significant milestone: a $1.40 billion market capitalization (as of January 19, 2026). While that figure still pales in comparison to giants like USDT and USDC, its significance goes far beyond size.

RLUSD’s growth marks a strategic inflection point for Ripple, and raises essential questions about XRP’s evolving role in the crypto ecosystem as we head into 2026.

For years, XRP’s value proposition has been debated, misunderstood, and often conflated with Ripple, the company. The emergence of RLUSD adds a new layer to that discussion, clarifying how Ripple envisions payments, liquidity, and token utility working together, not in competition, but in complementary roles.

What Is RLUSD? Ripple’s Stablecoin Explained

RLUSD is Ripple’s fully collateralized, fiat-backed stablecoin, designed primarily for enterprise payments, on-chain settlement, and institutional liquidity management.

Unlike algorithmic stablecoins or lightly regulated offshore issuers, RLUSD has been positioned from day one as a compliance-first product, aligned with U.S. regulatory expectations and built to integrate with traditional financial infrastructure.

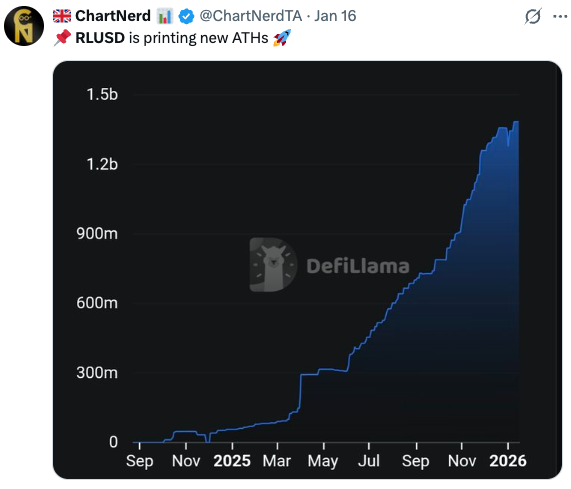

RLUSD on-chain data. | Credit: DefiLlama

Its rapid growth to a $1.40 billion market cap signals three things:

Institutional demand for regulated on-chain dollars is rising.

Stablecoins are becoming core financial infrastructure, not just a trading tool.

RLUSD is not meant to replace existing stablecoins in retail DeFi. Instead, it targets payments, treasury operations, and cross-border settlement, areas where predictability, regulatory clarity, and integration with banks matter more than yield farming or speculative liquidity pools.

Does RLUSD Replace XRP? Understanding the Difference Between XRP and Stablecoins

At first glance, a Ripple-issued stablecoin might appear to undermine XRP’s purpose. After all, if you can move dollars on-chain instantly, why use a volatile asset like XRP?

RLUSD acts as a unit of account and settlement currency.

XRP functions as a bridge asset for liquidity and interoperability.

In cross-border payments, especially between illiquid currency corridors, holding prefunded accounts in every local currency is expensive and inefficient. XRP’s role is to provide instant liquidity between two currencies that don’t have deep direct markets, while RLUSD provides a stable endpoint for settlement.

In practice, this can look like:

Local currency to XRP.

XRP to RLUSD.

RLUSD to destination currency.

Rather than displacing XRP, RLUSD reduces friction in XRP usage, especially for institutions that require a stable, dollar-denominated asset at some point in the transaction.

How XRP’s Utility Is Evolving as Ripple Expands RLUSD

As we move toward 2026, XRP’s role is becoming more specialized and more institutional.

And increasingly about invisible infrastructure, not speculative hype.

This mirrors what happened in traditional finance: the most valuable systems are often the ones end users never see.

The Impact of Stablecoin Regulation on Ripple, RLUSD, and XRP

One reason RLUSD’s growth matters so much is timing.

By 2026, stablecoin regulation in major jurisdictions, including the U.S. and Europe, is expected to be far clearer. In that environment:

Regulated stablecoins become trusted settlement assets.

Unregulated or opaque issuers face shrinking institutional relevance.

Interoperability between blockchains and banks becomes a competitive advantage.

Ripple has spent years positioning itself for this moment, even at the cost of slower growth and prolonged legal battles. RLUSD reflects that strategy: build products that institutions can actually use, not just speculate on.

For XRP, regulatory clarity reduces existential uncertainty. Instead of debating whether XRP is “a security,” the focus shifts to how it functions operationally within compliant payment flows.

Stablecoins vs. Liquidity Tokens: Why XRP Still Matters in Payments

One of the most important lessons of the last crypto cycle is that stablecoins are the interface layer of on-chain finance. They are what users, treasuries, and institutions interact with directly.

This is where assets like XRP remain relevant. XRP is not competing with stablecoins; it is a complementary infrastructure, designed to move value between them efficiently.

As RLUSD grows, demand for fast, neutral, and liquid bridges grows alongside it.

How RLUSD Changes the XRP Value Proposition in 2026

Its role in multi-asset, multi-chain payment systems.

This doesn’t guarantee price appreciation, but it does anchor XRP’s relevance in utility rather than narrative, which is precisely where institutional markets tend to gravitate.

Risks to XRP and RLUSD Adoption Investors Should Watch

None of this is without risk.

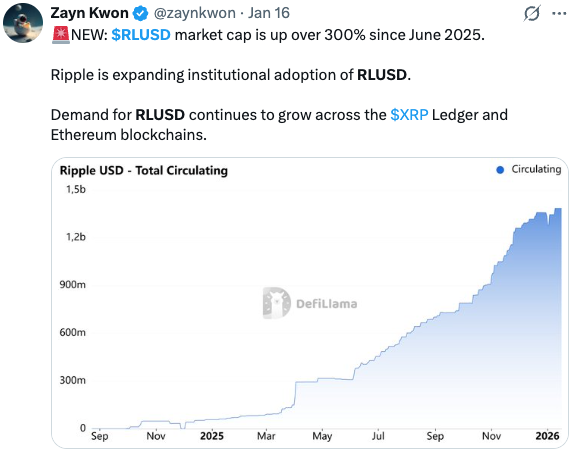

RLUSD market cap jumped by over 300% since June 2025. | Credit: Zayn Kwon

Will competing blockchain ecosystems offer cheaper or more flexible liquidity solutions?

Can Ripple maintain neutrality and interoperability in a fragmented multi-chain world?

There is also a strategic balance to strike. If too much value accrues to RLUSD without sufficient demand for XRP as a bridge, XRP’s role could narrow. Conversely, if XRP remains the most efficient liquidity rail, RLUSD’s growth could indirectly strengthen it.

In that world, XRP is less a headline-grabbing asset and more a critical piece of plumbing.

For investors, developers, and policymakers, the key takeaway is this: Ripple isn’t betting against XRP, it’s redefining what XRP is for.

By 2026, XRP’s success may not be measured by how loudly it trends, but by how deeply it is embedded in the global movement of value, often unseen, but increasingly indispensable.

RLUSD is Ripple’s U.S. dollar-backed stablecoin. It is fully collateralized, fiat-backed, and designed primarily for enterprise payments, on-chain settlement, and institutional liquidity management rather than retail DeFi speculation.

How big is RLUSD today?

RLUSD has reached approximately $1.38 billion in market capitalization, a notable milestone given its relatively quiet rollout and its focus on regulated, institutional use cases rather than retail trading.

How is RLUSD different from USDT or USDC?

Unlike many stablecoins that grew through crypto trading and DeFi usage, RLUSD is positioned as a compliance-first stablecoin, built to integrate with banks, payment providers, and regulated financial infrastructure from day one.

Why use XRP if RLUSD already moves dollars on-chain?

Stablecoins like RLUSD handle settlement, but they do not solve liquidity between illiquid currency pairs. XRP enables instant, capital-efficient liquidity between currencies or stablecoins that lack deep direct markets.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy