5 Scary Things That Happen to Your Crypto if Your Exchange Loses Its MiCA License on July 1

Share

Key Takeaways

Unlicensed EU crypto exchanges could freeze withdrawals or block users after July 1.

MiCA protections apply only to authorized exchanges, leaving users of unlicensed platforms exposed.

Moving funds to licensed exchanges or self-custody before July 1 reduces regulatory risk.

History has a habit of warning people before financial systems break. In 2008, customers of Washington Mutual, the largest US savings and loan association to ever fail, did not wake up one morning to find their money gone.

While most retail depositors were protected by FDIC insurance, investors were not. WaMu bondholders lost about $30 billion, shareholders were left with just 5 cents per share, and institutions including TPG Capital wrote off billion-dollar investments as years of litigation followed.

July 1, 2026 is the European crypto market’s most significant regulatory deadline to date, and users who assume their exchange is prepared could be the ones most exposed.

1. Withdrawals Could Freeze Before You Expect Them To

The first sign of an exchange winding down is rarely a public announcement. More often, it’s slower withdrawals. During the 2022 crypto credit crisis, Celsius quietly delayed withdrawals before freezing them on June 12, while Voyager followed a similar path. In both cases, users who exited early fared better than those who waited for official confirmation.

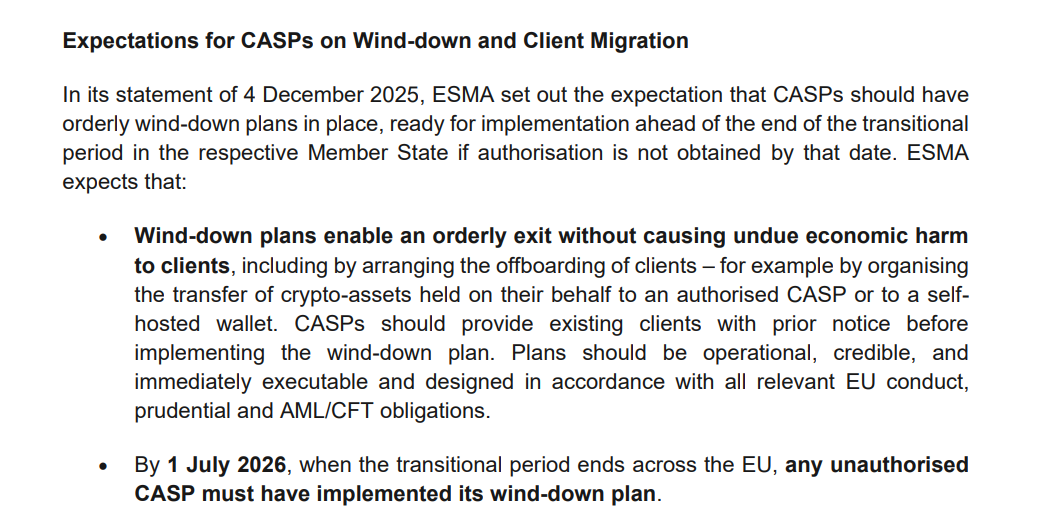

The European Securities and Markets Authority (ESMA) requires unlicensed providers to prepare orderly wind-down plans and notify customers before services end. But not every exchange may be ready.

ESMA expects licensed CASPs to actively onboard migrating clients before July 1, but users should still expect fresh identity checks and AML verification, as authorization does not automatically transfer between platforms. Delays are possible if large numbers of customers move at once, making an early transition the safer option.

If your platform has not clearly communicated its MiCA licensing status or transition plan, that uncertainty should be treated as a warning, not reassurance.

2. Your MiCA Investor Protections Disappear Immediately

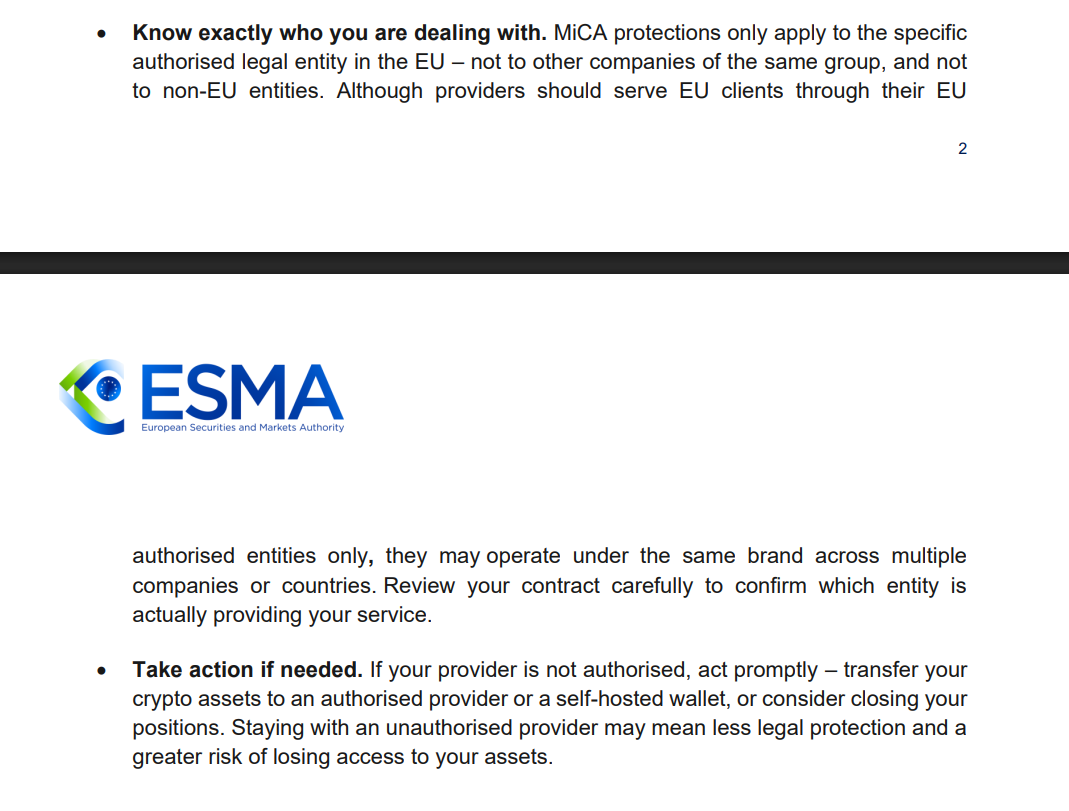

ESMA has warned explicitly that MiCA protections apply only to the authorized EU entity, not necessarily to other companies operating under the same brand name.

MiCA protections only apply to authorized EU entities. | Source: ESMA

This means an exchange may operate through a licensed EU subsidiary while other entities under the same brand remain unlicensed. Brand recognition does not guarantee MiCA protection.

3. You May Be Forced to Migrate to a Platform You Did Not Choose

When an unlicensed exchange winds down, it nominates an authorized provider to receive its migrating clients. The receiving firm must conduct full onboarding checks from scratch.

Authorization does not carry over from the old provider, meaning users must re-submit identity documents, wait for KYC approval, and potentially be rejected by the receiving platform if their risk profile does not meet its requirements.

This mirrors what happened to customers of collapsed UK payment firm Wirecard in 2020, whose accounts were frozen overnight following regulatory action, forcing users into emergency migrations with no preparation time and no customer service capacity capable of handling the simultaneous volume of requests.

Users in higher-risk jurisdictions or those with complex transaction histories may find the nominated platform does not accept them at all, leavingself-custody wallets as the only remaining option.

4. Criminal Liability Falls on the Exchange, Not You, But You Still Pay the Price

Operating without MiCA authorization after July 1 exposes firms to administrative fines of up to 5 million euros or 3% of total annual turnover, whichever is higher.

France’s AMF has gone further, warning that operating without authorization after the deadline could expose companies to criminal prosecution. Users are not personally liable for their exchange’s regulatory failure, but enforcement action against a platform tends to freeze operations while regulators investigate.

Regulatory action against an exchange can leave users waiting months to access their funds, with no clear timeline for resolution. Being legally entitled to your assets is not the same as being able to access them.

The pattern is familiar: regulators intervene, withdrawals are restricted or frozen, complaints take time to process, and funds remain locked while legal and administrative proceedings unfold.

5. Your Exchange May Simply Stop Serving You With No Warning

When Mt. Gox froze withdrawals in February 2014, users had no idea hundreds of thousands of Bitcoin were already missing. The exchange continued operating and accepting deposits until the collapse became impossible to hide.

MiCA’s wind-down rules are designed to avoid a similar scenario by requiring firms to notify customers and manage an orderly exit before losing authorization.

Even so, users should not assume every platform will wait until the last minute to communicate changes. Some may begin restricting services, geo-blocking EU users, or directing customers to migrate before July 1.

The practical lesson from every prior exchange failure is the same: by the time the announcement arrives, the easy exit has already closed.

Check the ESMA Interim MiCA Register first. ESMA publishes a public database of licensed crypto-asset service providers updated weekly. If your exchange does not appear on that register, it is operating without MiCA authorization and your funds should be treated as at risk regardless of how functional the platform looks today.

Move to a licensed exchange before June 30. Major exchanges that have secured MiCA authorization include Coinbase, Kraken, Bitstamp, Bitpanda, Bitvavo, OKX, Crypto.com and Revolut, each holding a CASP license passported across EU member states. Moving to one of these platforms before July 1 means your assets sit inside the MiCA protection framework.

Do not wait for a platform announcement. Celsius did not announce its withdrawal freeze in advance, and neither did Voyager. By the time an exchange publicly acknowledges a problem, users often have fewer options than those who acted earlier.

Unlike assets held on exchanges, crypto stored in self-custody wallets is not directly affected by an exchange’s MiCA authorization status. However, transfers between self-custody wallets and regulated exchanges may still be subject to EU Travel Rule checks and wallet verification requirements, while self-custody itself carries risks such as lost private keys, phishing attacks, and operational mistakes.

According to OKX Europe CEO Erald Ghoos, as many as 80% of crypto exchanges could disappear from the European market because they failed to meet MiCA’s requirements.

History suggests that during periods of financial or regulatory disruption, those who act before deadlines and service changes are typically better positioned than those who wait.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.