Crypto payment card volumes are hitting record highs, but weak compliance infrastructure could cause many crypto neobanks to fail. | Credit: CCN.com

Share

Key Takeaways

Crypto payment cards are experiencing record adoption, with tracked onchain volume surpassing $10.59 billion.

Rapid growth does not guarantee survival, as many crypto neobanks rely on fragile issuer relationships.

Past industry disruptions highlight the risks, as companies such as Binance and Ready Card lost payment processing partnerships.

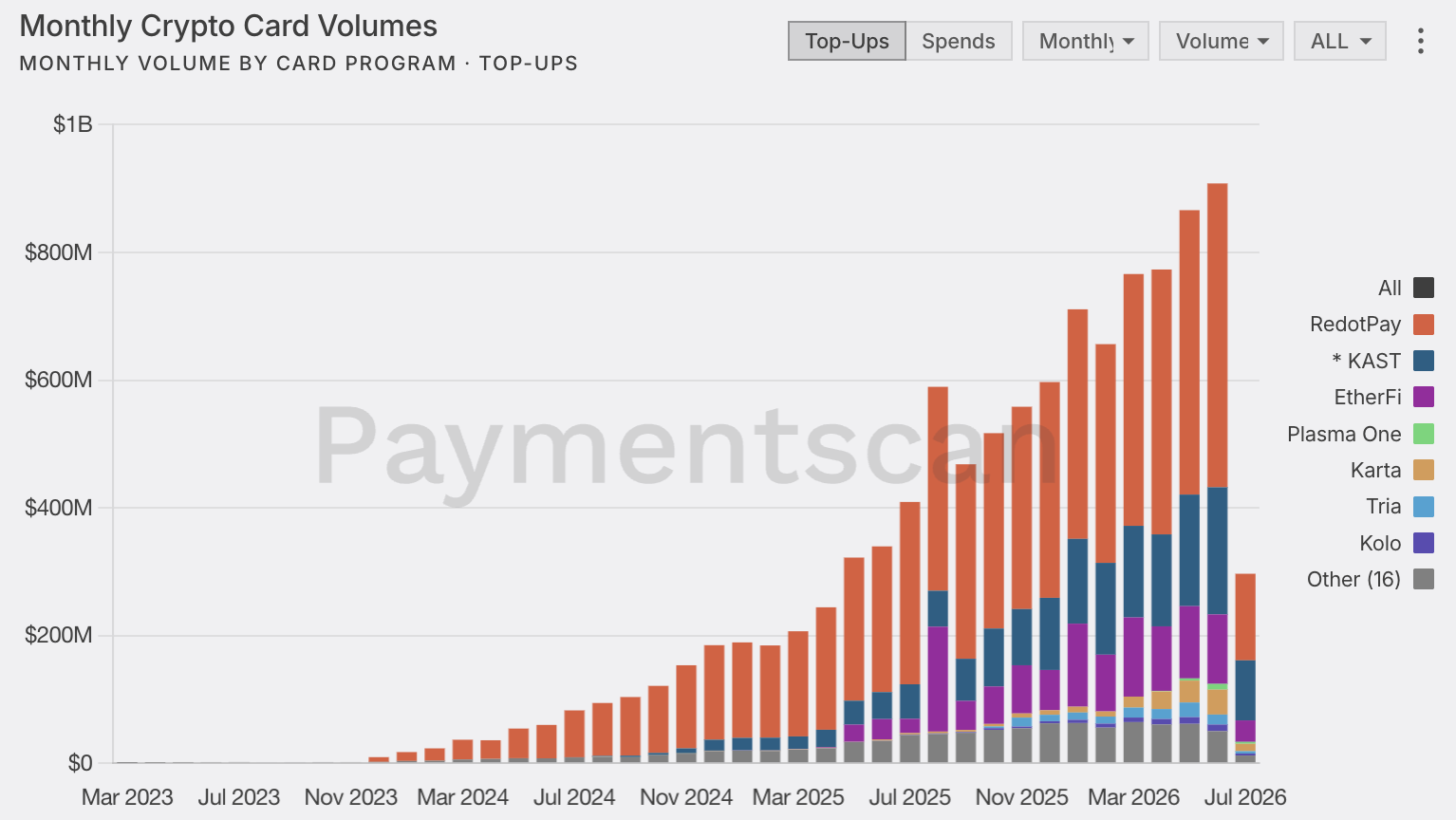

Crypto payment cards are no longer a niche experiment. Onchain data from PaymentScan shows total tracked crypto card volume has reached $10.59 billion, across more than 25.2 million transactions and 1.7 million addresses.

Monthly volume climbed from just $489,000 in April 2023 to $908 million in June 2026, before July’s partial-month figure reached $296.7 million.

RedotPay, KAST, and EtherFi now dominate tracked top-up flows, with RedotPay alone accounting for $6.37 billion in cumulative volume.

At first glance, the trend appears to be a breakout moment for crypto-native neobanks. Demand is growing, users are topping up cards, and stablecoins are increasingly being used for everyday payments.

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

PaymentScan data shows the monthly tracked volume rose from $184.9 million in December 2024 to $597 million in December 2025, then continued to climb to $711 million in January 2026 and $908 million in June.

Transactions also expanded from 280,637 in December 2024 to more than 2.2 million in June 2026.

Users are not only holding stablecoins or trading tokens; they are increasingly trying to spend digital assets through card networks, merchant rails, and neobank-style apps.

But volume can create a false sense of safety. A neobank can grow quickly while its compliance infrastructure lags behind. That is where the next 18 months could become dangerous.

The crypto card market depends on a three-way relationship between the neobank, the card issuer, and the payment network.

If either the issuer or the network loses confidence in the compliance stack, access can disappear quickly.

Compliance Failures Can Shut Card Programs Overnight

Recent history shows how fragile card access can be. Binance’s European Visa debit card program ended in December 2023, while Mastercard also cut several Binance card partnerships in Latin America and other markets in 2023.

More recently, Ready Card users outside the European Economic Area received about one hour’s notice before card services were halted following a card issuer transition.

User assets were not the issue. The payment rail was.

most neobanks will not survive the next 18 months.

not because demand disappears. $245M in top-ups in a single week proves demand is the least of your problems, they will die because of what they built underneath:

That distinction matters. Many crypto neobanks market themselves as self-custodial or stablecoin-native, but card spending still relies on regulated issuers, networks, sanctions controls, KYC, transaction monitoring, and jurisdiction-by-jurisdiction reporting.

The traditional banking sector has already shown what happens when controls fail to keep pace with growth.

The UK Financial Conduct Authority fined Starling Bank nearly £29 million after finding weaknesses in its financial crime systems and sanctions screening.

The FCA said Starling grew from around 43,000 customers in 2017 to 3.6 million in 2023, while its financial crime controls failed to scale at the same speed.

For crypto neobanks, the lesson is clear: growth does not protect a business if the control layer breaks.

The Survivors Will Build Compliance Before Products

The next phase of competition will not be won only by the apps with the best user experience or the highest cashback. It will be won by companies that build compliance as core infrastructure rather than a dashboard added after launch.

That means continuous sanctions screening, transaction-level monitoring, defensible KYC, source-of-funds checks, clean audit trails and separated ledgers for any yield or earn product.

It also means understanding that ramps, cards, rewards and stablecoin balances are not separate products from a regulatory perspective. They are connected risk surfaces.

They may have users, volume, and brand momentum, but still depend on weak issuer relationships, fragmented compliance tools, or unclear fund structures.

The winners will likely be the firms that treat compliance as the foundation of the business. The losers will be those who treat it as something to fix after scale arrives.

The $10.59 billion crypto card market shows demand is real. But the next test is not adoption. It is survivability.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.