Nebraska-Chartered Telcoin Launches First Regulated Onchain Bank Accounts

Share

Key Takeaways

Telcoin launched the first US onchain bank account tied to a regulated bank-issued stablecoin.

Telcoin operates under a Nebraska Digital Asset Depository Institution charter that authorizes it to accept deposits, issue eUSD, and apply for approval to connect to the Federal Reserve payment system.

The company is betting that bank-issued digital dollars will outperform non-bank stablecoins over time.

Telcoin Digital Asset Bank went live with onchain bank accounts for US residents on June 23, becoming the first regulated institution to connect a bank account directly to an onchain dollar.

The product runs on the company’s eUSD stablecoin, issued by Telcoin Digital Asset Bank under a Digital Asset Depository Institution (DADI) charter from the Nebraska Department of Banking and Finance, and is accessible through Telcoin Wallet, a self-custodial digital asset wallet integrated with the bank.

The launch places Telcoin in a different regulatory category from every other crypto company currently seeking banking-adjacent status in the United States. Circle and Ripple both received conditional approval for national trust charters from the Office of the Comptroller of the Currency, a route that explicitly excludes cash deposit-taking, fractional reserve operations, and checking or savings accounts.

Telcoin holds a full bank charter under the Nebraska Banking Act, which authorizes it to accept deposits, issue eUSD, and apply for approval to connect to the Federal Reserve payment system nationwide.

Why Nebraska and Why Now

Telcoin obtained its DADI charter in November 2025, the first company to do so under the Nebraska Financial Innovation Act, legislation Telcoin itself helped develop in 2021. That act created a first-of-its-kind state-level framework specifically designed to accommodate digital asset banking, establishing a regulatory pathway that predates the current federal scramble for stablecoin oversight by several years.

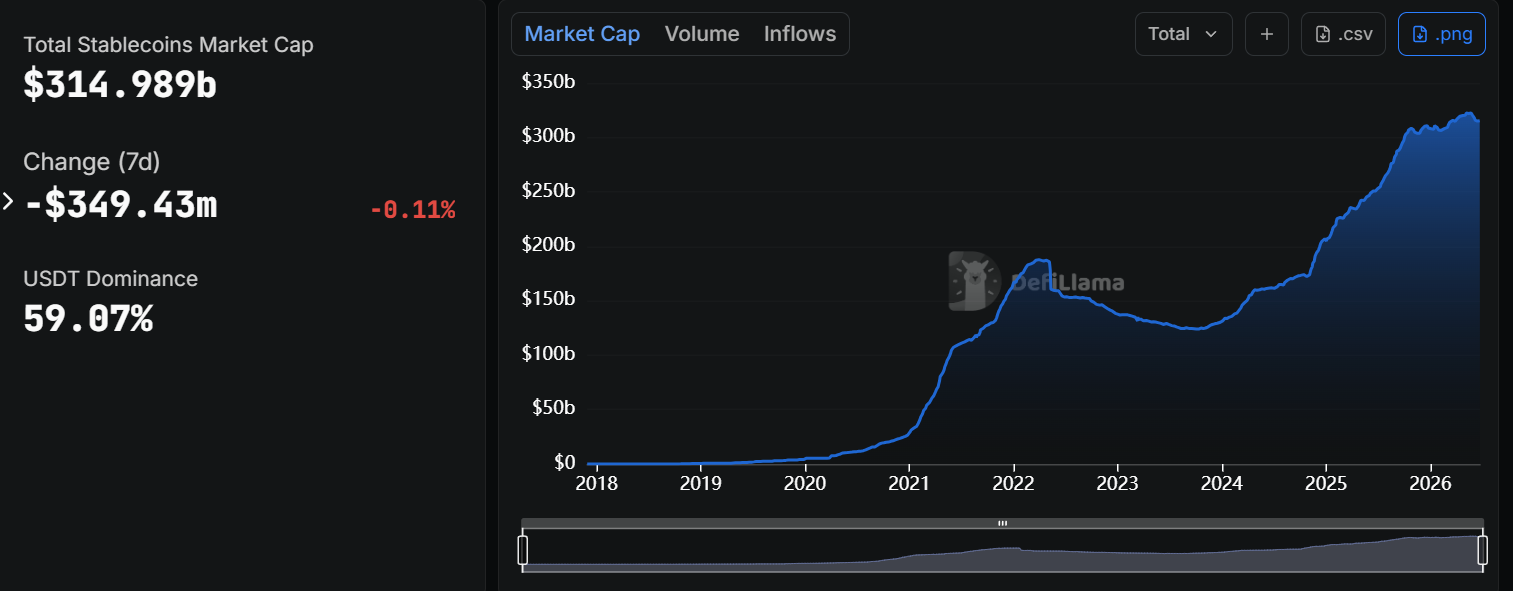

The GENIUS Act, signed into law in 2025, has since brought stablecoin issuance explicitly within the banking regulatory perimeter. Total stablecoin market supply stands at approximately $314.98 billion as of June 24, 2026 according to DeFiLlama, dominated by Tether’s USDT and Circle’s USDC. Both are non-bank issued.

Telcoin’s argument is that bank-issued digital dollars, operating within the existing payments infrastructure rather than parallel to it, represent the next structural shift.

The company frames the current moment as a window before that shift consolidates. More than a dozen crypto companies have sought regulatory standing in the past year alone, including several pursuing the OCC trust charter route. None has moved to replicate the Nebraska DADI structure.

Paul Neuner, founder and CEO of Telcoin, told CCN the reason is structural, not accidental.

“Any bank in the United States can legally do this right now, yet none have.

Regarding those who have sought trust charters, that is because they do not want to become a bank holding company. If a large non-bank institution wants to become a bank holding company, there is a clear path to do that. If they want to operate outside of the banking system, they will face structural challenges.”

Federal Preemption and the Deposit Question

A state-chartered bank taking deposits nationwide raises an obvious question: what stops federal regulators from asserting preemption over a Nebraska-authorized institution operating across state lines?

Neuner is direct on this:

“This issue of federal preemption doesn’t apply to us, because we are legally a bank according to the Nebraska Banking Act. We do not see any issues on this front at all.”

The legal basis for that confidence sits in the Nebraska Banking Act’s recognition of Telcoin Digital Asset Bank as a bank rather than a novel fintech category, a distinction that carries different preemption exposure than a state money transmitter license or a trust charter.

State-chartered banks have operated with nationwide deposit-taking authority under dual banking system precedent for decades. The DADI structure layers digital asset functionality on top of that existing foundation rather than creating a new legal category outside it.

The GENIUS Act Yield Question

Telcoin has announced that future releases of Telcoin Wallet will include yield on eUSD balances, which it describes as GENIUS Act-compliant. The GENIUS Act’s implementing rules are still being written by regulators, which raises the question of what happens to that product if rulemaking diverges from the company’s structural assumptions.

Neuner says the core legal question is already settled.

“The GENIUS Act is already law, and it is already clear that passive yield for simply holding a stablecoin is not allowed. The CLARITY Act is simply closing a loophole that Coinbase and others have been exploiting. This loophole will eventually get closed one way or another. While the rulemaking part of the GENIUS Act is important, we do not expect rulemaking to expressly counter a very basic tenet of the law, particularly when we are on the side of the banks and federal regulators on this one,” he said.

Telcoin argues that eUSD should be treated as a bank deposit product rather than a non-bank stablecoin. Under that interpretation, yield paid through a chartered bank would fall within existing banking rules rather than the GENIUS Act’s restrictions on non-bank stablecoin issuers.

Capital Constraints and Telcoin Network

The Nebraska Banking Act imposes capital deployment constraints on regulated entities. Telcoin is simultaneously building Telcoin Network, a layer-1 blockchain it describes as the first exclusively validated by telecommunications networks, which would expand eUSD’s reach through carrier distribution channels globally. The question of whether a regulated bank can fund speculative blockchain infrastructure inside its regulatory perimeter is not a trivial one.

Neuner says the corporate structure answers it cleanly.

“Telcoin Network is built and operated by the Telcoin Association, which is a Swiss Verein, a foundation, not owned by Telcoin Inc., Telcoin Digital Asset Bank’s parent company. So there are no capital constraint issues there.”

He adds a further dimension from the GENIUS Act’s language on bank holding companies.

“The GENIUS Act says that stablecoin activity is now considered banking activity as related to the Bank Holding Company Act. So this can be very widely interpreted to operating infrastructure related to settling stablecoin transactions, particularly if they are digital cash stablecoins issued by a bank. So it is really no problem for Telcoin Digital Asset Bank to be deeply involved in Telcoin Network, which is what is happening now and will give the network a distinct advantage,” Neuner explained.

On the broader competitive dynamics, Neuner pushes back on the narrative that every crypto company racing to issue a branded stablecoin represents the market’s direction of travel.

“Non-bank branded stablecoins in circulation are still a tiny fraction of the overall money supply, and frankly not really increasing as exponentially as people thought. The industry tends to lunge at quick money, and currently that is playing out in every crypto company trying to issue their own branded stablecoin that nobody really wants. Our bet is on unbranded bank-issued digital dollars, operating within the existing banking system,” Neuner noted.

What Comes Next

The current Telcoin Wallet release is focused on individual accounts tied to eUSD balances. Merchant and institutional accounts are in development, as are debit cards and API integrations designed to expand eUSD adoption across financial and digital asset platforms.

The NVIDIA GB200-era stablecoin infrastructure build is still early, but Telcoin’s bet is that its Nebraska Digital Asset Depository Institution charter, which explicitly authorizes it to accept customer deposits, issue eUSD, and apply for access to the Federal Reserve payment system, creates a structural moat that national trust banks cannot easily replicate.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.