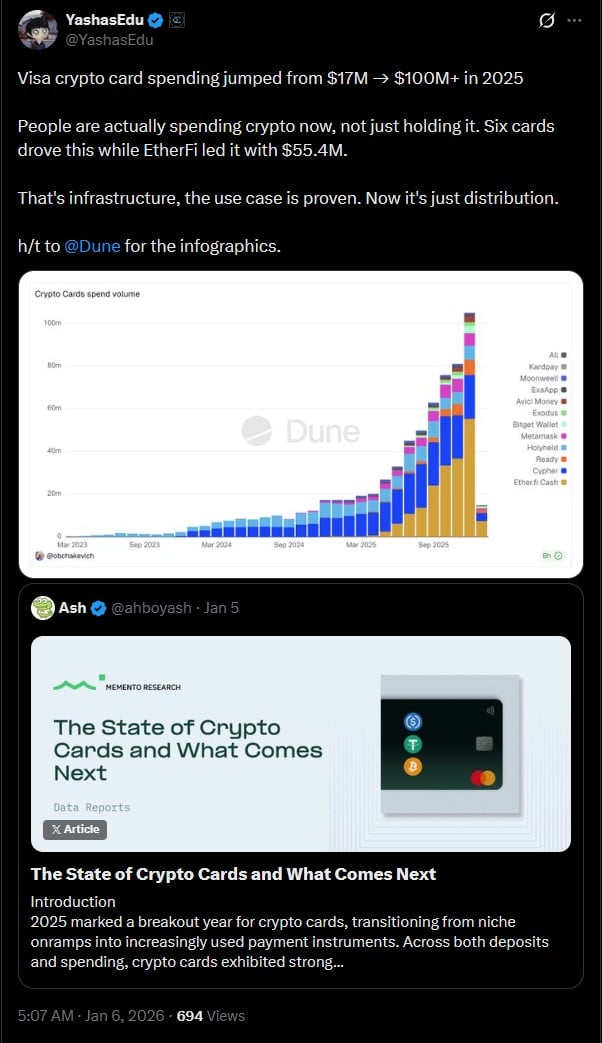

Crypto card spending has surged 500% to $600M monthly. Discover how stablecoins like USDC and USDT are driving crypto payments growth. | Credit: CCN.

Share

Key Takeaways

Crypto debit cards usually sell your crypto for cash at checkout, so the store still gets paid in dollars (or your local currency).

Custodial cards are easier to use, but the company controls your funds.

Self-custody cards give you more control, but you still follow Visa/Mastercard rules and may pay network fees.

Watch for hidden costs like spreads, FX fees, ATM fees, and “premium” subscription tiers.

Crypto debit cards let you pay at normal stores, online shops, and restaurants, all while using digital assets in the background.

The thing is, most merchants aren’t accepting crypto directly. Instead, the card typically converts your crypto into local fiat at the time of purchase, making them feel like a “normal” spend.

That conversion is the current tradeoff. Convenient crypto spending now, though there may be fees, taxes, and other considerations to be wary of.

New Trending Crypto Wallet Offers

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Custodial (exchange/app) cards: You hold assets on an exchange or app, and the card pulls from that balance, often converting crypto into fiat either instantly at the point of sale or via a “top up” process. That said, custodial means trusting a third party with your funds.

Self-custodial (wallet-linked) cards: These let you spend from a wallet you control, though the card will still run on Visa or Mastercard, most likely. This means the card still abides by an issuer and its rules.

Some have been using crypto debit cards for years. Source: @h4l on Reddit

Just be aware that in the US, the Internal Revenue Service (IRS) treats crypto as property. This means that when you spend crypto, you may incur a tax gain or a loss just as if you sold it on an exchange.

With those guidelines in mind, here are ten crypto debit cards that let you spend crypto in the real world.

10 Crypto Debit Cards to Consider

1. Coinbase Card (Custodial Visa Debit)

You can spend your Coinbase balance via the Coinbase Card at any merchant that accepts Visa. The card has no annual fee and zero spending fees, though spreads can still apply.

The card extends the use of your Coinbase holdings, but just remember that while there are no spending fees, spreads can incur additional costs per purchase.

2. Crypto.com Visa Card (Custodial Prepaid)

The Crypto.com Visa card is a prepaid method that has you convert holdings into a local currency, which you can then use to spend or withdraw via ATM. You have to top up the card before use.

Source: @YashasEdu on X

Crypto.com offers extra perks like monthly rewards via the platform’s CRO token, but higher card tiers incur various monthly subscription fees or CRO lockup requirements.

3. Bybit Card (Custodial Mastercard)

Bybit Card is a Mastercard debit card that allows you to spend from your Bybit holdings. The card operates both physically and digitally, and as of January 2025, it supports Bitcoin, Ethereum, XRP, USDT, USDC, and TON coin.

The card does require advanced identity verification and will prioritize the fiat in your Bybit Funding Account before spending cryptocurrency. Also, it charges a 0.9% crypto conversion fee, and other costs can stack depending on ATM or FX spending.

4. Oobit (Self-Custodial Visa)

Oobit isn’t a traditional crypto debit card, per se. It’s a tap-to-pay crypto payments app, allowing you to spend crypto anywhere Visa is accepted. The app links to your existing crypto wallet and converts your assets to fiat at the time of purchase.

Payments with Oobit cost up to 1% per transaction (minimum $0.25), using USD as its base currency. Oobit currently supports a wide variety of cryptocurrencies, including Bitcoin, Ethereum, Solana, BNB, USDT, and many more.

Source: @AriEiberman on X

Oobit also offers various cashback incentives, including up to 10% cashback when using OOB.

5. OKX Card (Custodial Mastercard)

OKX launched its card in Brazil, tied to your OKX Pay balance. You top up your card with Brazilian Reals via PIX, which OKX converts to USD-backed stablecoins. OKX Card currently supports USDG, USDT, or USDC spending anywhere that accepts Mastercard. From there, it automatically converts crypto to the region’s local equivalent upon spend.

As of its launch, OKX Card is entirely free to use and does not charge markup for FX spending.

6. ether.fi Cash (Non-Custodial Visa)

ether.fi is best known for non-custodial Ethereum staking/restaking, allowing you to keep control of your assets while using the protocol. It also offers ether.fi Cash, a non-custodial Visa credit card, that allows you to spend that crypto balance.

ether.fi offers two modes:

Direct Pay: Direct Pay works as a typical debit card, and immediately deducts funds from your ether.fi Vault, currently spending USDC or LiquidUSD.

Borrow Mode: Borrow mode allows you to use your crypto as collateral to borrow funds for a purchase, rather than selling it to make one. Borrow mode features a 4% annual percentage rate (APY), with no minimum payments or billing cycles. Instead, interest compounds over time.

Otherwise, the card offers 3% cashback on all purchases, and multiple membership levels based on membership points.

7. MetaMask Card (Self-Custodial Mastercard)

MetaMask Card allows you to spend your non-custodial holdings where Mastercard is accepted. The card currently supports spending via mUSD, amUSD, wETH, EURe, GBPe, USDC, aUSDC, aBasUSDC, and USDT.

Source: @DanRosario_eth

A virtual MetaMask card offers 1% cashback on all purchases, while the physical Metal card ($199 annual fee) offers 3% with no FX fees. That said, you do pay crypto-to-fiat conversion rates and are charged a small fee for each transaction.

8. Gnosis Pay Card (Self-Custodial Visa)

Gnosis Pay is a self-custodial crypto debit card that spends stablecoins held in the Gnosis Safe wallet, allowing for spending wherever Visa is accepted. You don’t need to top up a custodial account, your funds remain in the Safe wallet for spending, sort of like a checking account.

Gnosis Pay offers up to 5% cashback, with a 1% boost for original non-fungible token (NFT) holders. It also does not charge transaction fees, gas fees, or FX fees.

9. Ledger CL Card (Self-Custodial Visa)

Ledger’s Crypto Life (CL) Card is powered by Baanx and allows you to spend your Ledger holdings with up to 1% cashback in Bitcoin or USDC in the US, or Bitcoin and USDT in the rest of the world. It also offers 2% cashback via Baanx’ BXX token. The card is designed for management via the Ledger App, though you can use the CL Card with other wallets via additional configuration.

As of January 2026, you can spend USDT, USDC, wETH, XRP, and SOL, though more assets should be added soon. You can draw from a stablecoin credit line if you live outside the US, though US citizens cannot access the credit line.

There are no annual fees, but you do have to pay fiat-to-crypto conversion fees as well as charges for deposit via fiat.

10. Wirex Card (Custodial Visa or Mastercard)

Wirex card is a debit card linked to your Wirex account, which makes it a custodial option. You can use it to spend cash, stablecoins, or cryptocurrencies, as well as to withdraw from ATMs.

The Wirex Card should work wherever Visa or Mastercard are accepted, based on your region. It does not charge an annual fee, though it offers up to 8% cashback via the WXT token, based on your subscription tier. The initial tier is free, but higher tiers require significant WXT staking.

Picking the right crypto debit card is important. If you want a simple experience, a custodial card tied to an exchange might be the best path. Self-custody can be a little more complex, but it provides complete control over your assets, despite having to abide by issuer rules.

Either way, make sure you cover all of your bases, examining fees, spreads, fx costs, taxes, and more, alongside card benefits like cashback.

Do stores “accept crypto” when I use a crypto card?

Usually no. The card provider converts your crypto into fiat, and the store gets paid normally.

What’s the difference between custodial and self-custody cards?

Custodial: the app/exchange holds your funds. Self-custody: you hold the funds in your own wallet (but the card still uses Visa/Mastercard rails).

What is a spread in crypto card spending?

It’s the “gap” between the price you expect and the price you actually get when the provider converts your crypto.

Can a crypto debit card trigger taxes?

In many places, yes. In the U.S., spending crypto can count like selling it, which may create gains or losses.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy