STRC's market price implies a 63% chance of a dividend increase, while signaling limited distress or suspension risk. | Credit: CCN.com

Share

Key Takeaways

STRC’s market price suggests a dividend increase is the most likely outcome, according to analyst Khing Oei.

Much of the discount reflects the upcoming dividend decision and unpaid dividend accrual rather than concerns about solvency.

Because STRC is a cumulative preferred security, unpaid dividends would continue to accrue and eventually need to be repaid before other shareholder distributions.

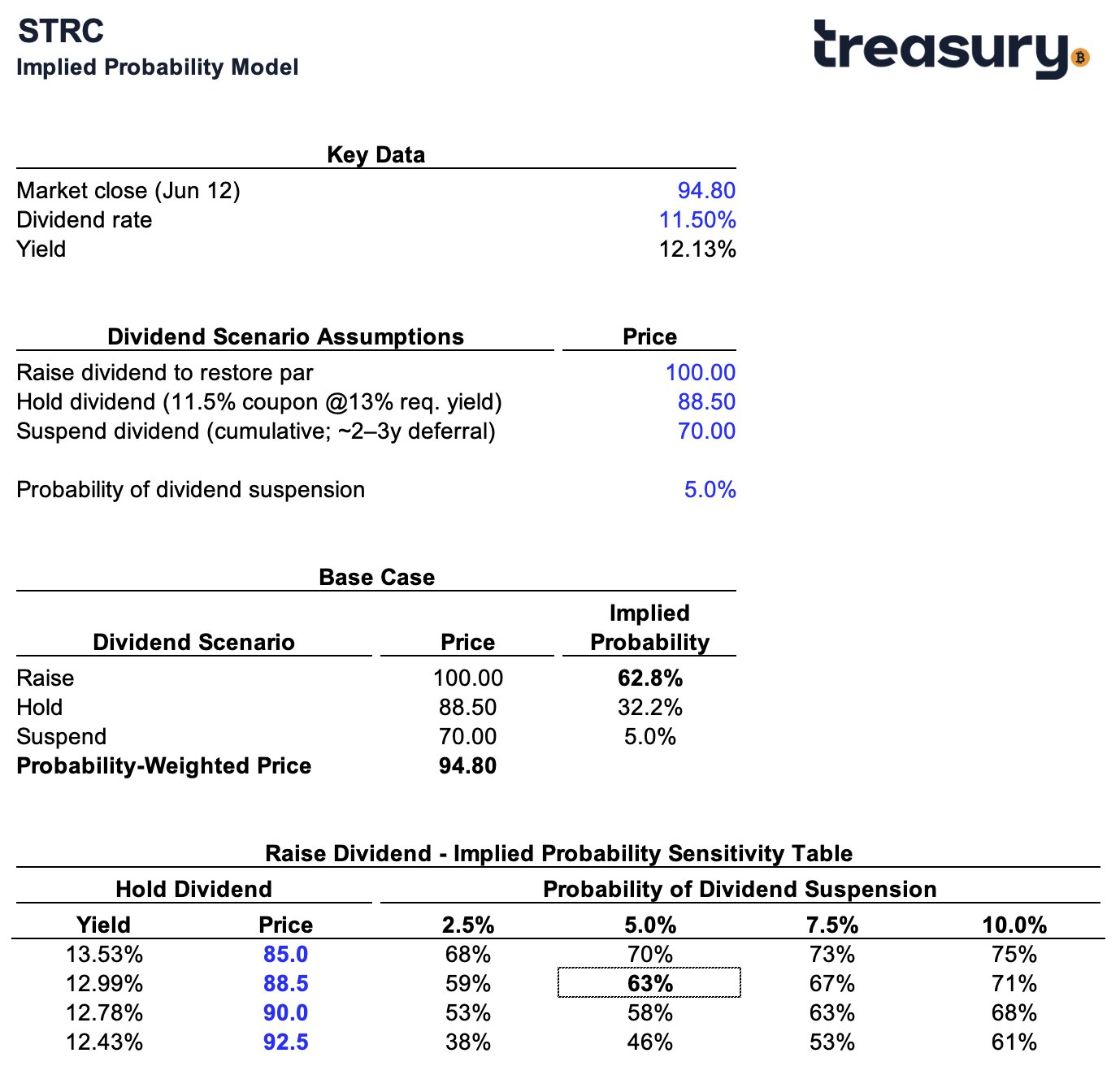

STRC closed at $94.80 on Friday ahead of its upcoming ex-dividend date, with investors closely watching Strategy’s month-end dividend decision.

The preferred stock is trading 5.2% below its $100 par value, sparking debate over whether Strategy executives Michael Saylor and Phong Le will raise the dividend to restore par, maintain the current payout, or suspend dividends altogether.

However, according to a new analysis by investor and former hedge fund founder Khing Oei, the market is signaling a much clearer message than the ongoing debate suggests.

By treating STRC’s current price as a probability-weighted reflection of potential outcomes, Oei argues that investors are effectively assigning a 63% probability to a dividend increase, while pricing only a minimal risk of distress.

Try Our Recommended Crypto Exchanges

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

Oei’s framework assumes that Strategy’s dividend decision at the end of June will result in one of three outcomes, each carrying a different implied valuation for STRC.

In the most bullish scenario, Strategy raises the dividend sufficiently to restore the stock to its $100 par value.

Oei notes that par effectively serves as the ceiling because the company’s at-the-market issuance mechanism can sell unlimited shares at that level, preventing the stock from sustainably trading above it.

This is the clearest explanation I’ve seen regarding $STRC and the depeg + the impact on the dividend and the risk for $BTC through a potential selloff.

— Michaël van de Poppe (@CryptoMichNL) June 14, 2026

The second scenario assumes Strategy maintains the current 11.5% dividend rate. Under that outcome, Oei estimates STRC would reprice to approximately $88.50 based on a market-required yield of 13%, similar to comparable securities.

The final scenario involves a dividend suspension. While often viewed as a worst-case outcome, Oei argues that the market may be overstating the potential damage.

Because STRC’s dividends are cumulative, any unpaid distributions continue accruing and must eventually be repaid before other shareholder distributions can occur.

Using a discounted cash flow framework that assumes a three-year recovery period and a distressed required return of 25%, Oei estimates the suspension scenario would still imply a value of roughly $70 per share.

“Anyone marking suspension at 50 or 60 is implicitly assuming the structure is permanently impaired, for which there is no basis at 3x-plus asset coverage,” he wrote.

Market Pricing Implies Dividend Increase Is Most Likely Outcome

With the stock trading at $94.80, he assumed a 5% probability of dividend suspension and then solved for the remaining probabilities. The result suggests investors are pricing in a 63% chance of a dividend increase, a 32% chance of the current dividend remaining as it is, and only a 5% chance of suspension.

According to the analysis, the stock’s current price sits closer to the $100 “raise” scenario than to the $88.50 “hold” scenario, indicating that investors are leaning toward a favorable outcome.

More importantly, Oei argues that the near-par valuation itself serves as evidence that the market is not pricing significant distress risk.

“If investors genuinely believed suspension was a meaningful possibility, STRC could not remain trading only five points below par,” he said.

Even a modest increase in suspension probabilities would drag the probability-weighted valuation into the mid-$80 range, well below current trading levels.

In that sense, the stock’s price acts as a market-based rejection of severe downside fears.

Yield Expectations Matter More Than Suspension Risk

Perhaps the most notable conclusion from the analysis is that suspension risk has surprisingly little influence on the model’s output.

Oei’s sensitivity analysis found that increasing the assumed suspension probability from 2.5% to 10% only moved the implied probability of a dividend increase from roughly 59% to 71%.

By contrast, small changes in the yield investors would demand if the dividend remains unchanged produced much larger swings in the outcome.

For example, adjusting the assumed ‘hold’ valuation from $92.50 to $85, equivalent to investors demanding a slightly higher yield, caused the implied probability of a dividend increase to shift from the mid-40% range to around 70%.

As a result, Oei concludes that the central question facing STRC investors is not whether Strategy will suspend dividends but rather how much the market will require in compensation if management chooses not to restore the stock to par.

“The question priced into STRC this weekend is not will they suspend,” Oei wrote. “The real driver is what discretionary capital costs when the issuer chooses not to defend par.”

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.