STRC's market price implies a 63% chance of a dividend increase, while signaling limited distress or suspension risk. | Credit: CCN.com

Share

Key Takeaways

The 11.5% headline yield from STRC drops to roughly 8% for token holders after US withholding tax, meaning actual investor returns are significantly lower than advertised.

Ondo Finance enables non-US investors to gain exposure to Strategy Inc. preferred stock without needing a traditional brokerage account, removing major access barriers.

Investors face multiple risk layers including Strategy’s Bitcoin-dependent balance sheet, smart contract vulnerabilities, and oracle reliance via Chainlink.

STRC tokenization reflects the broader shift toward bringing real-world assets onchain, positioning preferred stocks as a middle ground between low-yield bonds and volatile equities.

On May 4, 2026, Ondo Finance announced the tokenization of Strategy’s Stretch preferred stock, trading on Nasdaq under the ticker STRC, and made it available across three major blockchains: Ethereum, BNB Chain, and Solana. The token represents Strategy’s perpetual preferred stock, which pays monthly dividends and currently yields 11.5% annually, and is live through the Ondo Global Markets platform.

This launch is not just another crypto product announcement. It sits at the intersection of corporate Bitcoin treasury strategy, real-world asset tokenization, and the ongoing effort to bring traditional fixed-income-style instruments to decentralized rails.

To understand why this matters and where it breaks down, you need to understand each of those three layers individually.

What STRC Actually Is

Before analyzing what Ondo has done, you need a firm grasp of the underlying asset.

Strategy Inc. is the largest publicly traded Bitcoin holder, and STRC is its variable-rate perpetual preferred stock. The word ‘perpetual’ is critical here. Unlike a corporate bond with a maturity date, STRC has no fixed redemption date. Strategy is under no legal obligation to ever return your principal. You are buying a stream of dividend payments, not a loan.

STRC currently yields 11.50% annually, paid monthly, and its preferred coupons are supported by USD reserves of $2.25 billion, which provides coverage for roughly 21.8 months of payments. That reserve figure tells you something important: the dividend is not currently funded by operating profits. Strategy holds Bitcoin, not a profitable enterprise that generates stable cash flow.

STRC’s coupon is funded from a combination of Strategy’s cash reserves, software business revenue, and continued capital raised by issuing more STRC shares, a model that some analysts have described as circular, where new investor capital partly funds existing dividend payments. This does not make STRC fraudulent, but it does mean the sustainability of the dividend is tied to two things: Strategy’s ability to keep raising capital, and the long-term direction of Bitcoin prices that anchor the balance sheet.

As of May 4, STRC was trading at $99.95, having traded slightly below par since April 15, with a 52-week range of $88.00 to $100.42 and a current market cap of approximately $64.57 billion.

Ondo Tokenization Layer and ELN Structure

Ondo’s tokenized STRC is not a direct claim on the underlying preferred stock. It is an equity-linked note, or ELN, which is a blockchain-based instrument that tracks the price and economic performance of STRC without conferring shareholder rights.

Holders gain economic exposure to the underlying preferred, less applicable tax withholdings on dividends, but the tokens themselves are not preferred stock and do not provide rights to hold or receive the actual underlying shares.

The token is issued by Ondo Global Markets (BVI) Limited, a company incorporated in the British Virgin Islands. Tokens trade Monday 8:00 AM ET through Friday 7:59 PM ET, with peer-to-peer transfers available 24/7. Pricing reflects traditional brokerage market data via Chainlink oracles, and tokens are backed 1:1 by underlying securities held in regulated offchain custody with licensed broker-dealers.

Most tokenized stock launches to date, across Ondo, xStocks, Backed Finance, and others, have focused on liquid common stocks like Tesla, NVIDIA, and Apple. Preferred stocks have been largely absent from the tokenization wave, making STRC one of the first to bridge that gap.

STRC’s Headline Yield vs Net Investor Returns

This is where most coverage fails readers. The 11.5% figure is the gross dividend rate declared by Strategy at the underlying-stock level. What you actually receive as a token holder on Ondo is different, for a structural reason rooted in tax law.

The Ondo Global Markets entity that issues the tokens is based in the British Virgin Islands, so dividends paid by US companies to the entity are subject to the standard 30% US withholding tax. When dividends are reinvested, the platform does so net of this withholding tax.

As a concrete example, if STRC paid out $1 in dividend, Ondo would only receive and reinvest $0.70 after the 30% withholding tax is applied. This brings the effective yield you receive as a token holder closer to the 8% figure that Ondo itself displays as the “underlying asset dividend yield” on its platform.

This gap between 11.5% and 8.03% stems from withholding tax rules. Those net dividends are automatically reinvested into more underlying STRC shares rather than paid out in cash, so holders receive total return exposure through a gradual increase in shares per token rather than direct cash distributions.

This is not a hidden fee or a deception. It is disclosed in Ondo’s documentation. But the marketing of an “11.5% yield” without immediate context around the tax treatment is precisely the kind of detail that misleads retail investors who are comparing it to a savings account or a certificate of deposit.

Bull Case for Tokenized STRC Product

Supporters of the launch make legitimate and specific arguments.

That 11.5% annualized yield is 2 to 4 times higher than current short-duration instruments like money-market funds, CDs, or T-bills, even after the withholding adjustment produces an effective yield around 8%. An 8% yield on a Nasdaq-listed preferred stock with monthly distributions is still a significant income instrument for non-US investors who have historically had no clean way to access it.

The Global Markets platform targets non-US investors in Asia Pacific, Europe, Africa, and Latin America. For an investor in Vietnam or Nigeria, accessing a Nasdaq-listed preferred stock through a traditional brokerage is either impossible or operationally expensive. The tokenized version removes that barrier entirely.

The token gives eligible users economic exposure to the shares while keeping settlement and transfers onchain, so investors can move or trade positions 24/7 instead of waiting for traditional market hours. This is a genuine infrastructure improvement over the traditional system, not a marketing claim.

Bear Case Risks and Structural Concerns

Several analysts have raised specific, substantive concerns that deserve detailed treatment.

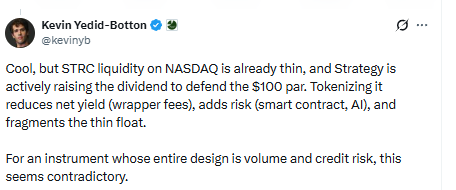

Kevin Yedid-Botton, an investor and portfolio manager at ParaFi Capital, offered the clearest critique: ‘STRC liquidity on NASDAQ is already thin, and Strategy is actively raising the dividend to defend the $100 par. Tokenizing it reduces net yield through wrapper fees, adds smart contract risk, and fragments the thin float.’ Each part of this deserves unpacking

On liquidity: Experts claim the tokenized price could diverge from the STRC price over time. If the underlying stock itself has thin trading volume, the tokenized version inherits that constraint. Ondo’s infrastructure can only provide as much liquidity as the traditional market does, because redemptions must ultimately flow through a broker-dealer buying or selling actual STRC shares.

Kevin Yedid-Botton’s critique of Strategy’s STRC. | Source: X.

On the circular dividend model: The fact that Strategy issues new STRC shares to fund Bitcoin purchases, and that those Bitcoin purchases theoretically support the balance sheet that backs the dividend, creates a reflexive loop. If Bitcoin prices fall sharply, Strategy’s balance sheet weakens, its ability to continue raising capital through STRC issuance becomes harder, and dividend sustainability comes into question. That risk is not unique to the tokenized version, but it is amplified by the fact that token holders are one additional layer removed from the underlying security.

On added risk layers: Token pricing uses a Chainlink oracle infrastructure that delivers real-time pricing, corporate action data, and reserve verification. The tokens query a KYCRegistry smart contract before every transfer, checking both sender and receiver KYC status and sanctions clearance. Each of these components is a potential failure point. Oracle manipulation, smart contract bugs, or regulatory action against the BVI entity issuing the tokens are all risks that a direct holder of STRC on a US brokerage account does not face.

If you believe that $STRC is offering a safe 11.5% yield (I am not commenting on this), then why wouldn't you play your own carry trade and buy $STRC, take a margin loan against it on any platform <5% and reinvest in $STRC?

You have to DEEPLY believe that $STRC will hold par.

The STRC launch comes as tokenized real-world assets are gaining momentum, with the tokenized US Treasury market alone reaching over $15 billion in value in early May 2026. Ondo Finance already ranks among the largest issuers in that space through its USDY and OUSG products.

The tokenization of preferred stocks is a logical next step in that progression. Common stocks carry price volatility. Treasury bills carry low yields. Preferred stocks sit in between: higher yield than government debt, more price stability than equity, and a fixed income stream. Bringing them onchain serves a real market need.

But this product requires an investor who understands three distinct layers of risk: the creditworthiness of Strategy’s Bitcoin-backed balance sheet, the structural tax treatment that reduces gross yield by 30%, and the smart contract and custodial risks introduced by the tokenization wrapper itself. Investors who treat the 11.5% headline number as comparable to a high-yield savings account are making a category error. The yield is real, the access improvement is real, and the risks are equally real.

FAQs

What is Ondo Finance STRC token and how does it work?

Ondo Finance STRC token is a blockchain-based asset that gives investors economic exposure to Strategy Inc.’s preferred stock (STRC). It is structured as an equity-linked note (ELN), meaning holders track the price and dividends of the stock without owning the actual shares. The token is available on networks like Ethereum, BNB Chain, and Solana.

How much yield do investors actually receive from STRC token?

While STRC preferred stock offers an 11.5% annual dividend yield, token holders typically receive closer to 8% net yield. This reduction is due to a 30% US withholding tax applied before dividends are reinvested. Returns are not paid in cash but compounded through additional exposure to the underlying asset.

Is Ondo STRC token safe compared to traditional stocks?

STRC token carries additional risks beyond traditional stock ownership. These include smart contract risk, reliance on oracle pricing (such as Chainlink), and regulatory exposure tied to offshore issuance structures. Investors are also exposed to the financial health of Strategy and Bitcoin market volatility.

Who can invest in tokenized STRC and why is it useful?

Tokenized STRC is primarily designed for non-US investors who may not have easy access to US brokerage accounts. It allows global users to gain exposure to a Nasdaq-listed preferred stock with onchain settlement, 24/7 transfers, and lower barriers to entry compared to traditional financial systems.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy