Strategy’s $11.2 Billion Bitcoin Loss Sparks New Fears Over Michael Saylor’s Treasury Strategy

Share

Key Takeaways

Strategy’s 843,706 BTC position is sitting on an $11.2 billion unrealized loss as Bitcoin trades near $62,560, well below the company’s $75,699 average cost basis.

The sale of just 32 BTC to fund preferred stock dividends ended a four-year no-sell streak, triggering fears of a feedback loop between STRC falling below par, rising dividend obligations, and further forced Bitcoin sales.

With cash reserves down from $2.25 billion to $900 million and $750-800 million in annual preferred dividend obligations, Strategy’s ability to keep accumulating Bitcoin at current prices is effectively exhausted.

The company disclosed on June 1 that it sold 32 Bitcoin between May 26 and May 31 at an average price of $77,135 per coin. The proceeds were earmarked for distributions on its STRC perpetual preferred stock. The sale itself is economically immaterial, but the signal it sent is not.

According to an 8-K filing with the SEC, Strategy sold 32 BTC between May 26 and May 31 for approximately $2.5 million. | Source: WuBlockchain on X.

How the Math Got Here

Strategy holds 843,706 BTC acquired at an average cost of $75,699 per coin, giving the company a total cost basis of roughly $63.8 billion. With Bitcoin trading near $62,560 as of June 4, the reserve is valued at approximately $52.6 billion, producing an unrealized paper loss of $11.2 billion.

This figure does not include the $14.46 billion unrealized loss already recorded for Q1 2026 under FASB fair value accounting rules, which require Strategy to mark its entire Bitcoin position to market every quarter and to run those losses through the income statement.

The equity picture is equally uncomfortable. MSTR stock has fallen roughly 72% from its July 2025 peak. The company began 2026 with a $2.25 billion liquidity reserve. That figure has since declined to $900 million, meaning Strategy burned through approximately $1.35 billion in roughly five months.

Combined annual dividend obligations across its five series of preferred stock now run between $750 million and $800 million per year, a number that is not shrinking.

STRC: The Pressure Valve

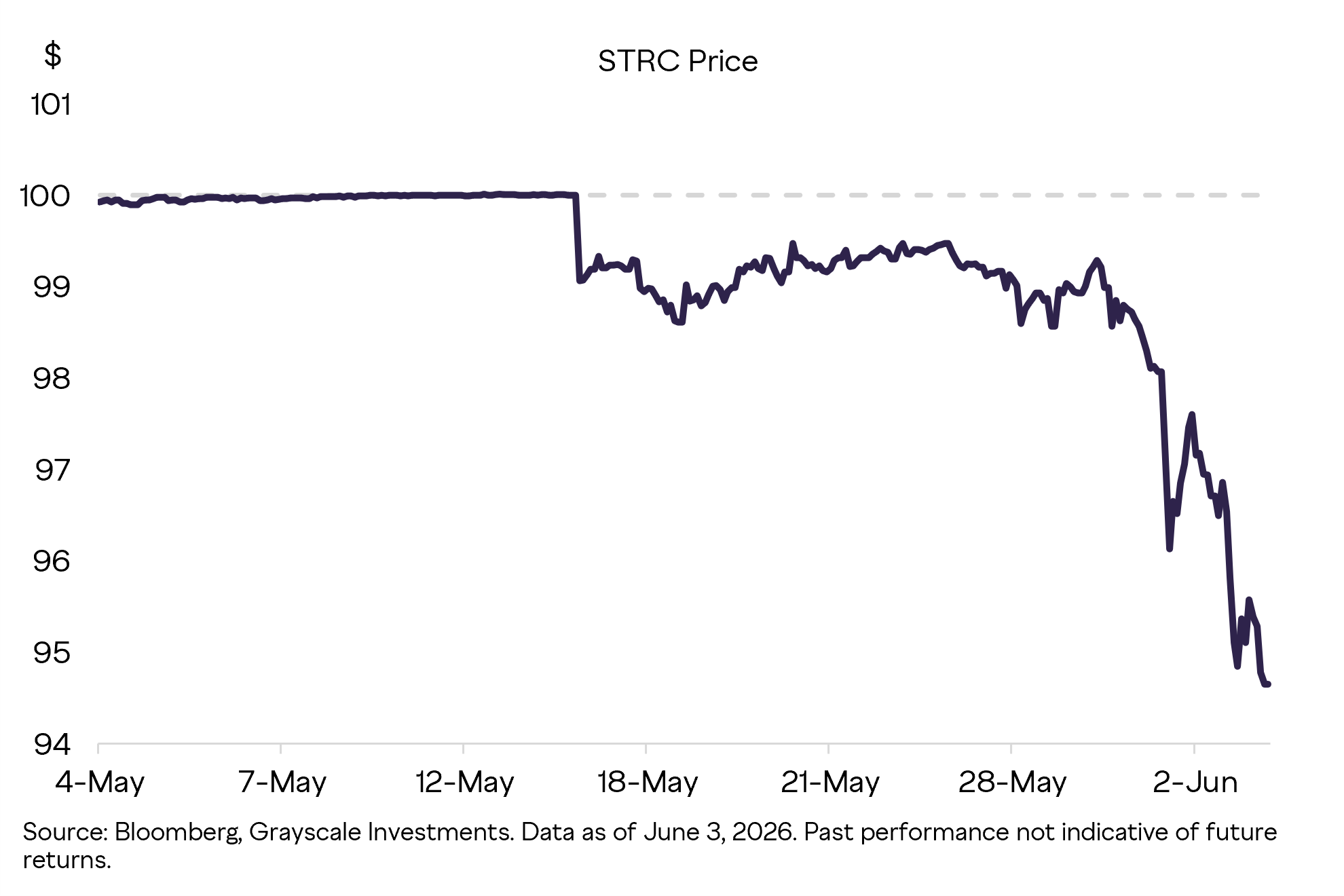

Grayscale Research’s Zach Pandl, writing on June 4, identified the real vulnerability in Strategy’s structure: not the Bitcoin position itself, but what happens to STRC, its variable-rate preferred equity instrument designed to trade at $100 per share.

STRC currently pays an 11.5% dividend and is trading below par at around $94.60. When STRC trades below $100, investors are demanding a higher return than the dividend currently offers.

Falling share price of STRC may require Strategy to raise dividend. | Source: Grayscale

Strategy can raise the dividend to bring buyers back, but that deepens its cash flow obligations, which in turn puts more pressure on Bitcoin sales and further downward pressure on Bitcoin prices. It is a feedback loop with no clean exit.

That dynamic has also hit MSTR’s leveraged derivative products. MSTY, MSTU, and MSTX, the trio of ETFs built on Strategy’s common stock, have seen acute volatility this week as confidence in the accumulation model wavers.

Spot Bitcoin ETFs reported $396.6 million in net outflows on the same day Strategy’s sale became public, adding to a broader liquidation that erased roughly $1.63 billion in leveraged positions within 24 hours.

Saylor’s Defense and the June 8 Vote

Michael Saylor has not gone quiet. Talking to X on June 4, he framed the Bitcoin selloff not as a loss of confidence but as a shift in capital. He said AI infrastructure is attracting about $400 billion in investment over six months, and that roughly $4 billion in Bitcoin ETF outflows since May 14 reflect money moving into that trend rather than weakening Bitcoin fundamentals.

Capital markets are funding the AI buildout at historic scale: ~$400B over 6 months. Bitcoin ETFs have seen ~$4B of outflows since May 14, pressuring $BTC. This is a capital rotation, not a Bitcoin impairment. Volatility creates opportunity.

A shareholder vote scheduled for June 8 on capital structure matters will test whether that narrative holds with institutional investors.

Grayscale’s Pandl offered the more considered long-term framing, arguing that less Bitcoin concentrated on levered corporate balance sheets and more distributed across diversified holders would ultimately be healthier for BTC price stability. In the short run, however, that transition requires other buyers to absorb what Strategy cannot.

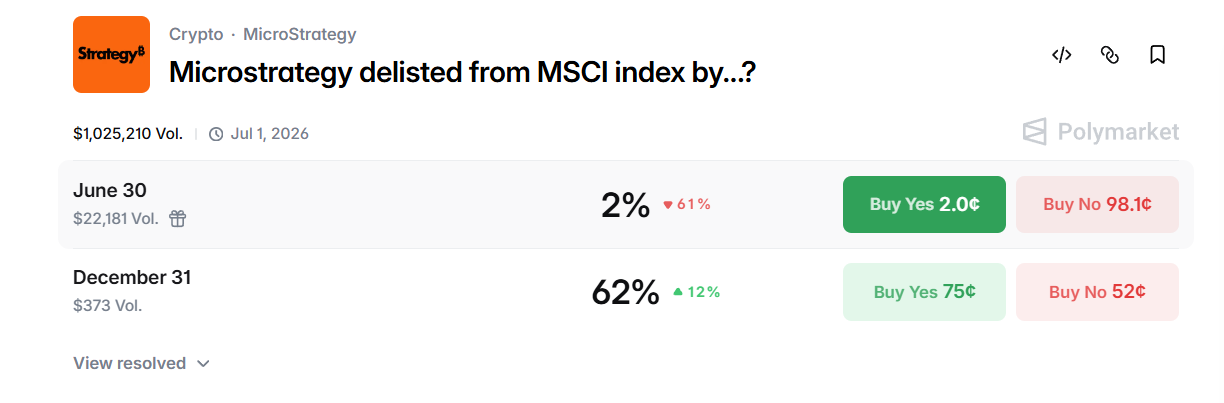

Polymarket is currently pricing a 2% chance that Strategy will be delisted from either the MSCI World or MSCI USA Index by June 30, 2026, suggesting that real-money traders consider the near-term removal risk negligible.

Strategy Faces MSCI Index Delisting Speculation on Polymarket. | Source: Polymarket

The more meaningful number sits in the December 31 contract, where the probability jumps to 62%, reflecting genuine market concern that a sustained Bitcoin price decline, continued MSTR share price weakness, and the structural pressures on the company’s preferred equity instruments could push Strategy below MSCI’s eligibility thresholds before year-end.

An MSCI removal would matter well beyond symbolism: it would force passive index funds and ETFs tracking those benchmarks to sell their MSTR positions simultaneously, adding mechanically driven selling pressure on top of an already stressed balance sheet at exactly the wrong moment for Bitcoin price stability.

The 32-coin sale may be remembered as a footnote. It may also be remembered as the moment the market realized Strategy’s accumulation model had structural limits that Bitcoin’s price decline was beginning to expose.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.