The Bank of Japan’s December 19 rate hike could trigger another liquidity shock. Bitcoin has dropped 20–30% after each BoJ tightening. | Credit: CCN.com

Share

Key Takeaways

The Bank of Japan is a critical driver of global liquidity.

BoJ’s expected 25 bps rate hike on Dec. 19 could have outsized effects on risk assets, including Bitcoin.

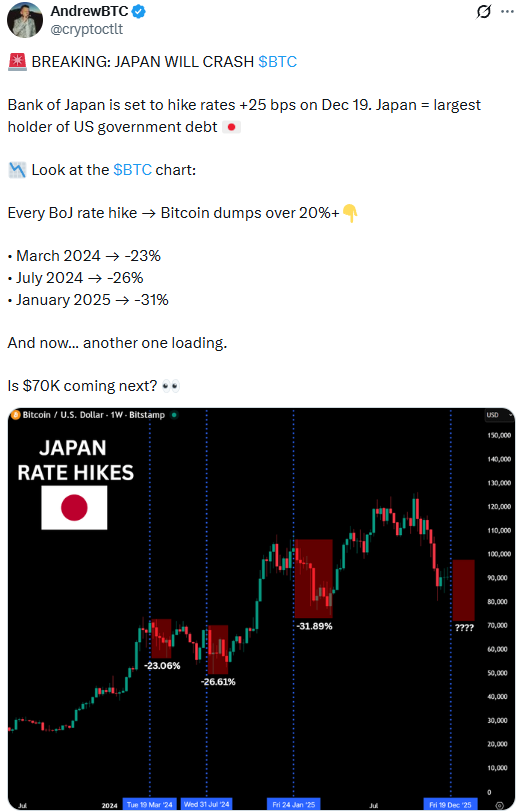

Bitcoin has fallen 20%–30% after each of the last three BoJ rate hikes, underscoring its sensitivity to Japanese monetary policy.

When the BoJ tightens, the yen strengthens and carry trades unwind, draining liquidity and forcing leveraged investors to sell risk assets.

For years, Japan’s ultra-loose monetary policy has quietly underpinned global risk-taking. While investors focused on the Federal Reserve, inflation prints, and ETF flows, the Bank of Japan (BoJ) played a more subtle yet decisive role in global liquidity. Now, that role may be about to flip, and Bitcoin could be caught in the crossfire.

Markets widely expect the BoJ to raise rates again, likely to around 0.75%, during its December 18–19, 2025 policy meeting, marking another key step in Japan’s gradual move away from decades of ultra-loose monetary policy. The probability of a hike is widely estimated above 90%, and history suggests that when Japan tightens, Bitcoin does not react kindly.

In fact, the last three BoJ rate hikes coincided with Bitcoin drawdowns of 20% to over 30%. With another hike looming, investors are asking an uncomfortable question: could Japan’s next move send Bitcoin toward the $70,000 level, or lower?

To understand why this risk is being taken seriously, it’s essential to understand Japan’s unique position in global finance and the mechanics of the so-called yen carry trade.

How Japan’s Fight Against Deflation Made the Yen the World’s Cheapest Funding Currency

Japan has spent decades fighting deflation. As a result, the BoJ kept interest rates near zero, and even negative, for a long time after other central banks had normalized their policies. This made the Japanese yen the cheapest funding currency in the world.

Markets price a rat hike by the Bank of Japan at over 91%. | Credit: Bloomberg

Global investors and institutions took advantage of this by borrowing yen at exceptionally low rates and deploying that capital into higher-yielding or higher-risk assets elsewhere. This strategy, known as the carry trade, became a structural pillar of global liquidity.

When markets were calm and interest rates remained low, the carry trade thrived. Cheap yen flowed into:

U.S. Treasuries and corporate bonds.

Global equities.

Emerging markets.

High-beta assets, such as technology stocks and, eventually, Bitcoin.

As long as Japanese rates remained anchored, there was little incentive to unwind these positions.

What Happens When the Bank of Japan Raises Interest Rates?

A BoJ rate hike changes the equation almost immediately.

Bitcoin, despite its narrative as “digital gold,” still trades like a high-risk liquidity asset in moments of stress. When liquidity drains, Bitcoin is often one of the first assets sold.

This is not theoretical. It has already happened, repeatedly.

What the Japan Carry Trade Is and How It’s Linked to Bitcoin

The Japan carry trade is basically a way investors try to make money by borrowing cheaply in Japan and investing in something that earns more somewhere else.

Because Japan’s interest rates are close to zero (at present), investors can take out loans in yen at very low cost. Then they convert that yen into another currency, such as U.S. dollars, and invest in higher-return assets, including stocks, bonds, or even Bitcoin.

Here’s a simple example:

Imagine an investor borrows ¥10 million in Japan at an interest rate of 0.1%. They convert it into about $70,000 USD and buy Bitcoin.

If Bitcoin’s price increases by 10%, the investor earns $7,000, which is significantly more than the minimal cost of borrowing yen.

However, if the yen suddenly strengthens or the Bank of Japan raises rates, the investor may lose money when converting back to yen.

In that case, they might sell their Bitcoin quickly to cut losses, which can push Bitcoin’s price down.

So, when Japan keeps interest rates low, investors tend to borrow more and take on risk, which helps assets like Bitcoin rise. But when Japan’s central bank tightens policy or the yen gets stronger, those trades often unwind, and Bitcoin can fall as a result.

Correlation Between BoJ Tightening and Bitcoin Price Drops

A stronger yen can force Japanese institutions to repatriate capital, while global investors scramble to adjust hedges and funding structures. This creates second-order effects that ripple far beyond Japan’s borders.

Bitcoin, deeply integrated into global risk sentiment, rarely escapes these waves unscathed.

Fed vs BoJ Policy Divergence: A Major Risk for Bitcoin Markets?

The current setup is particularly fragile because it may involve policy divergence.

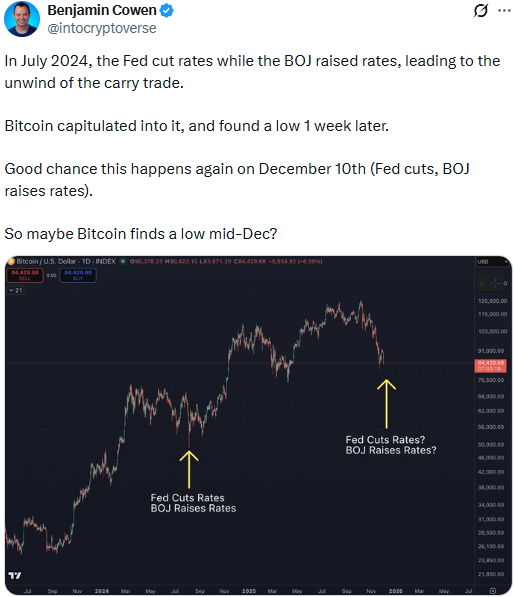

Expectations on Bitcoin around BoJ rate decision. | Credit: Benjamin Cowen X profile

When U.S. rates fall, and Japanese rates rise, the yield advantage that supported borrowing yen to buy U.S. and global assets collapses. This accelerates unwinds, compresses leverage, and drains liquidity from speculative corners of the market, including crypto.

A similar dynamic played out in July 2024, when Bitcoin sold off sharply before finding a local bottom roughly one week later.

Could Bitcoin Fall to $70,000 After the Next BoJ Rate Hike?

A 20-30% drawdown from recent highs would mathematically place Bitcoin near the $70,000 level, making this scenario plausible rather than sensational.

That does not mean Bitcoin is “broken” or that the long-term thesis has changed. This means that short-term price action remains highly sensitive to global funding conditions.

Greater market depth and liquidity than in prior years.

Increased awareness among macro investors.

At the same time, leverage remains elevated in derivatives markets, and retail sentiment has turned optimistic, conditions that can exacerbate downside moves during shocks.

Whether Bitcoin drops 10%, 20%, or more will likely depend on positioning, leverage, and how aggressively carry trades unwind, rather than solely on the rate hike.

Key Signals Investors Should Watch Ahead of the BoJ Decision

As December approaches, several signals will matter:

Funding rates and open interest in crypto derivatives.

Cross-asset stress in equities and bonds.

If Bitcoin sells off sharply in the lead-up to the BoJ decision, it may already be pricing in much of the risk. Conversely, complacency ahead of the meeting could leave the market vulnerable to a sudden air pocket.

Yen Carry Trade Unwind: How Japan’s Bond Market Triggers Bitcoin Sell-Offs

For years, Bitcoin was framed as an asset detached from traditional finance. The events of late 2025 told a different story.

When Japan’s bond market jolted in early December, Bitcoin didn’t merely react; it moved in sync with the yen, erasing billions in value and suffering the most enormous liquidation wave in crypto history. This wasn’t a crypto-specific crash. It was the mechanical unwinding of a global system built on decades of ultra-cheap Japanese money.

Japan spent nearly 30 years as the world’s primary funding engine. Near-zero rates turned the yen into the cheapest borrowing currency in the world, fueling the yen carry trade. Institutions borrowed yen, converted it into foreign currencies, and deployed the capital into higher-yielding assets, from equities and bonds to, increasingly, Bitcoin.

By mid-2025, Japan held over $3.6 trillion in foreign securities, with yen-funded positions conservatively estimated to be above $3.4 trillion and potentially far higher. That structure depended on one assumption: Japanese yields would stay low.

On Dec. 1, that assumption cracked. Japan’s 10-year yield surged to 1.877%, the highest since 2008. Markets priced in a BoJ rate hike, and the yen strengthened sharply, as carry trades began to unwind.

As funding costs rose, leveraged positions were rapidly closed, draining liquidity across global markets. Bitcoin, now deeply embedded in institutional portfolios, was among the first assets sold.

Why Global Liquidity and Central Banks Still Drive Bitcoin

Bitcoin is often portrayed as an asset that operates outside the traditional financial system. In practice, its price remains deeply intertwined with global liquidity cycles.

Japan’s role as the world’s hub for cheap money means that BoJ policy changes have a significant impact. When the carry trade unwinds, Bitcoin tends to feel fast and hard.

Whether or not $70,000 is the next stop, one lesson is clear: ignoring the Bank of Japan has become increasingly costly for crypto investors.

As history shows, when Japan tightens, Bitcoin listens.

Why does the Bank of Japan matter so much for Bitcoin?

The Bank of Japan has kept interest rates near zero for decades, making the yen the cheapest funding currency in the world. This allowed global investors to borrow yen and invest in risk assets, including Bitcoin. When the BoJ tightens policy, that cheap liquidity disappears, often triggering sell-offs in high-risk assets like crypto.

What is the yen carry trade, in simple terms?

The yen carry trade involves borrowing Japanese yen at very low interest rates, converting it into other currencies, and investing in higher-yielding assets such as stocks, bonds, or cryptocurrencies. As long as Japanese rates stay low, the strategy is profitable. When rates rise, investors rush to unwind these trades, selling assets to repay yen loans.

Is there evidence that BoJ rate hikes hurt Bitcoin?

Yes. The last three BoJ tightening episodes coincided with Bitcoin drawdowns of more than 20%. In March 2024 Bitcoin fell about 23%, in July 2024 it dropped 26%, and in January 2025 it declined roughly 31%, each time following BoJ rate hikes or tightening signals.

What should investors watch next?

Key indicators include the BoJ’s rate decision, movements in the yen, funding rates and leverage in crypto derivatives, and signs of stress across equities and bond markets. These signals can help gauge whether liquidity pressures are intensifying or easing.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy