Bitcoin has turned deflationary with a −0.21% effective inflation rate as dormant supply grows, while the US, Russia, and China now control 65% of global Bitcoin hashrate. | Credit: CCN.com

Share

Key Takeaways

Bitcoin is now effectively deflationary as liquid supply is shrinking, resulting in an estimated -0.21% net inflation.

Long-term holders and lost coins are reducing available supply faster than new BTC is being mined.

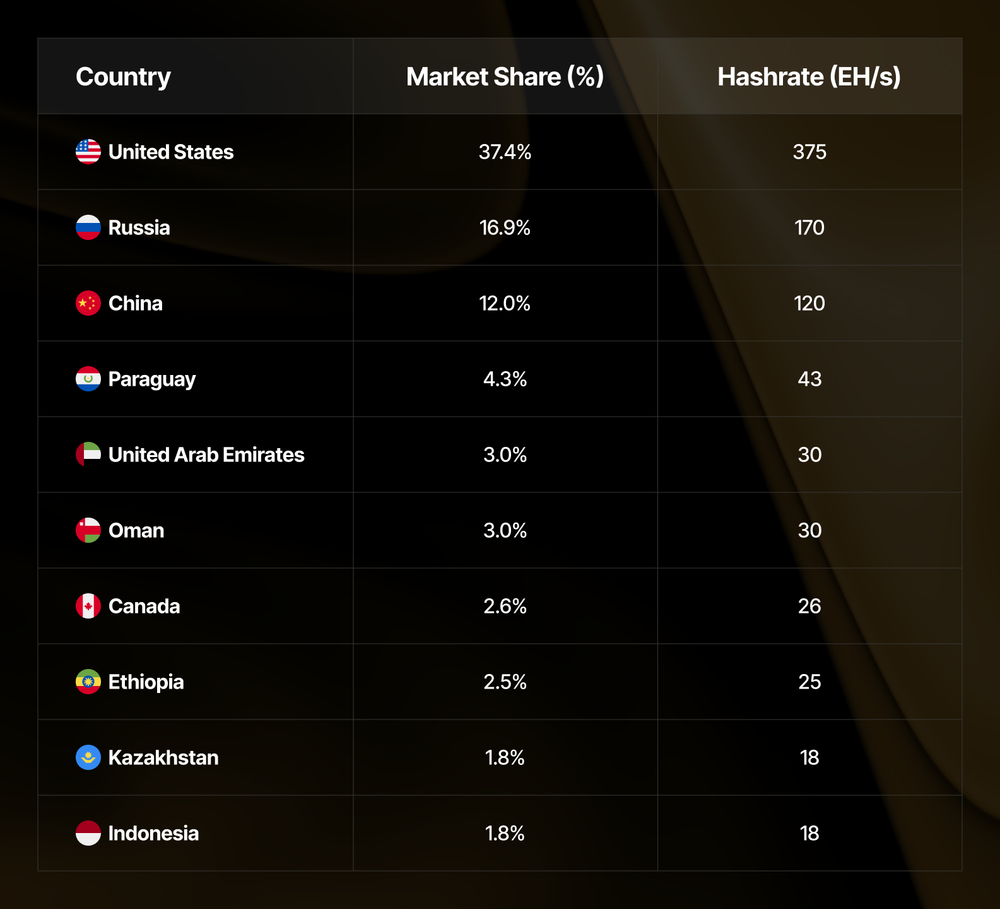

The US, Russia, and China control 65% of global hashrate, highlighting ongoing centralization risks at the infrastructure level.

Mining is becoming less profitable for many operators as rising costs and low hash price are forcing older machines offline and pushing weaker miners out of the market.

Bitcoin is often described as a scarce digital asset, but recent data suggests its scarcity may now be intensifying in a new way. According to Binance Research, Bitcoin is already operating in deflationary territory, with net inflation at roughly -0.21%. In simple terms, more bitcoin is effectively disappearing from active circulation than is being newly created.

That shift comes from an unusual imbalance as around 164,000 BTC is issued each year through mining rewards and roughly 290,000 BTC goes dormant annually.

Dormant coins are not destroyed, but they are coins that appear to have fallen out of active circulation for long periods, whether because their holders refuse to sell, have lost access to their wallets, or simply are not moving them. The result is that Bitcoin’s liquid supply may be shrinking even while the network continues to produce new coins.

At the same time, Bitcoin’s security infrastructure tells a very different story. Mining power remains heavily concentrated geographically. According to the latest Hashrate Index data for Q2 2026, the US (37.4%), Russia (16.9%), and China (12.0%) together account for about 65% of global Bitcoin hashrate.

Why Bitcoin Is Becoming Deflationary: Supply Shrinks as Dormant BTC Rises

Bitcoin has a fixed maximum supply of 21 million coins, but that does not automatically make it deflationary in day-to-day market terms. New BTC is still issued every block as miners secure the network. What changes the picture is the rate at which coins stop circulating.

The “21M hard cap” narrative understates real scarcity. | Credit: Binance Research

If 164,000 BTC is mined in a year, but 290,000 BTC becomes dormant, then the active supply available to traders, institutions, and everyday holders is shrinking.

Markets respond to available supply, not just theoretical supply. A bitcoin that has not moved in years may still exist on-chain, but if it is highly unlikely to be sold, it behaves almost like a removed supply.

What Dormant Bitcoin Means for Long-Term Holders and Market Supply

It is tempting to interpret dormant BTC as a sign of stagnation, but that would be misleading. Dormancy often reflects conviction.

Many long-term holders treat Bitcoin less like a transactional currency and more like a strategic reserve asset.

Some dormant BTC is almost certainly lost forever, which strengthens scarcity further. But a large portion is more likely held by investors, treasuries, funds, and early adopters who are choosing not to move their coins.

In other words, Bitcoin can become more scarce even while adoption and infrastructure continue to grow.

If the supply side looks increasingly decentralized, the mining side remains more concentrated than many Bitcoin supporters would like.

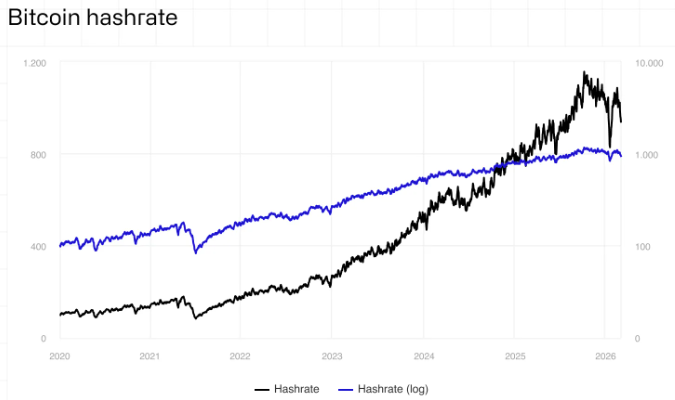

Hashrate Index reports that global hashrate fell from 1,066 EH/s in Q1 2026 to 1,004 EH/s in Q2 2026, a 5.8% quarter-over-quarter decline, driven primarily by falling profitability.

Top countries by hashrate share. | Credit: Hashrate Index

Risks of Bitcoin Mining Centralization in the US, Russia, and China

Bitcoin is designed to resist centralized control, but geographic concentration introduces risk. When mining is clustered in a few countries, external factors can have outsized effects.

History shows that these risks are real. China’s mining bans and enforcement actions have repeatedly shifted global hashrate, while regional conflicts have impacted countries like Iran.

However, Bitcoin has remained resilient. When one region declines, mining activity typically relocates rather than disappears.

Emerging Bitcoin Mining Hubs: Kyrgyzstan, Paraguay, and Ethiopia

The concentration story is evolving. Several emerging markets are gaining share, particularly those with cheap energy and modern infrastructure.

Bitcoin may be becoming more deflationary, but its infrastructure is still consolidating. Whether the network becomes more decentralized from here will depend not on ideology, but on energy markets, regulation, and the economics of next-generation computing.

Yes, based on recent estimates, Bitcoin is effectively deflationary in terms of liquid supply. While new BTC is still issued (164,000 per year), a larger amount (290,000 BTC annually) is becoming dormant, resulting in negative net inflation (-0.21%).

What does “dormant Bitcoin” mean?

Dormant Bitcoin refers to coins that have not moved on-chain for a long period of time. This can happen because long-term holders are choosing not to sell, some coins are permanently lost due to inaccessible wallets, or institutions and treasuries are holding assets without transacting. While these coins still exist, they are effectively removed from active market circulation.

How does dormant BTC affect Bitcoin’s price?

When more BTC becomes dormant than is newly mined, the amount of Bitcoin available for trading decreases. This reduction in liquid supply can limit selling pressure and make prices more sensitive to changes in demand. As a result, in periods of rising demand, price movements can become more pronounced.

Which countries control most of Bitcoin mining?

As of Q2 2026, Bitcoin mining remains highly concentrated geographically. The United States accounts for about 37.4% of global hashrate, followed by Russia at 16.9% and China at 12.0%. Together, these three countries control roughly 65% of the network’s total computational power.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.

Easy

Easy