Where do we expect the eurozone interest rates to be in five years? | Credit: Ralph Orlowski/Getty Images

Share

Key Takeaways

The European Central Bank raised its interest rates in June.

This marks the first rate increase for the first time in almost three years.

The next monetary policy decision is scheduled for July 22, 2026.

The European Central Bank (ECB) increased its interest rates in June, for the first time after almost three years, in a move widely anticipated by markets.

Policymakers warned that higher energy prices could fuel broader inflationary pressures, while the conflict may weigh on growth through weaker incomes and confidence.

The European Central Bank (ECB) raised its three key interest rates by 25 basis points, citing inflation risks linked to the ongoing war in the Middle East.

The ECB said it will continue to take a data-dependent approach and remains committed to returning inflation to its 2% target over the medium term. Following the decision, the deposit facility rate rises to 2.25%, the main refinancing rate to 2.40%, and the marginal lending rate to 2.65%.

The ECB also provided new economic forecasts: it now expects eurozone inflation to average 3.0% in 2026, 2.3% in 2027, and 2.0% in 2028, while economic growth is projected at 0.8%, 1.2%, and 1.5%, respectively.

“The outlook remains uncertain, with upside risks for inflation and downside risks for economic growth. The full implications of the war for medium-term inflation and growth will depend on the intensity and duration of the energy price shock, as well as the scale of its indirect and second-round effects,” the ECB said.

“This uncertainty is also reflected in the broad range of outcomes for inflation and growth in the updated illustrative scenarios put together by Eurosystem staff. These will be published with the staff projections on the ECB’s website.”

A Hike Now, But What’s Next?

As said, the hiking move by the Frankfurt-based institution was highly expected by the markets. But what lies ahead for the eurozone bank?

According to Bas van Geffen, CFA, Senior Macro Strategist at Rabobank, “Lagarde stated that a rate hike was the robust decision across multiple scenarios. We believe this makes a follow up hike more likely; we maintain September is the most likely timing.”

But it also suggests the ECB may not be willing to raise rates much higher than that.

“The new staff projections are worse than in March, but revisions were smaller than anticipated. This confirms that the ECB is not in a rush to adjust its policy stance.”

For van Geffen, “Lagarde did not give the impression that the Governing Council is in a rush to tighten. The ECB did not sound overly concerned about the inflation dynamics yet, and the relatively modest revisions to the staff projections also lower the urgency of follow-up hikes.”

“The “robustness check” also favours September, in our view. By then, the ECB will have another update of the economic projections, and at that time it may be a bit clearer to what extent the initial energy price shock is leading to broader price pressures. So, September probably allows for a better robustness test.”

Introducing the European Central Bank

The European Central Bank (ECB) is a central component of the Eurosystem and the European System of Central Banks (ESCB), making it one of the seven institutions of the European Union (EU). As one of the world’s foremost central banks, it holds a position of immense significance on the global stage.

The ECB Governing Council formulates monetary policy for the Eurozone and the European Union. It manages the foreign exchange reserves of EU member states, conducts foreign exchange operations, and defines the intermediate monetary objectives and key interest rates within the EU.

To execute these policies and decisions, the ECB Executive Board operates under the authority of the Governing Council and may issue directives to the national central banks as needed. Additionally, the ECB possesses the exclusive authority to authorize the issuance of euro banknotes. Meanwhile, member states’ issuance of euro coins requires prior approval from the ECB. The ECB also oversees the functioning of the TARGET2 payments system.

Established in May 1999 through the Treaty of Amsterdam, the ECB’s crucial mission is to ensure and preserve price stability. Subsequently, on Dec. 1, 2009, the Treaty of Lisbon came into effect, officially designating the ECB as an EU institution.

Eurozone Expansion

Initially, the ECB was established to serve the Eurozone, consisting of eleven member countries. Over time, the Eurozone expanded to include Greece in Jan. 2001. It also added Slovenia in Jan. 2007, Cyprus, and Malta in Jan. 2008. Furthermore, Slovakia in Jan. 2009, Estonia in Jan. 2011, Latvia in Jan. 2014, Lithuania in Jan. 2015, and Croatia in Jan. 2023.

Currently, President Christine Lagarde leads the ECB, which has its headquarters in Frankfurt, Germany. Before its new headquarters, it operated from the Eurotower.

The ECB operates in direct accordance with European Union law. Its €11 billion capital stock is collectively owned by all 27 central banks of EU member states as shareholders. Based on the population and GDP of member states, the initial capital allocation key was established in 1998 but has since undergone adjustments. Notably, shares within the ECB are non-transferable and cannot serve as collateral.

ECB Interest Rates

The key interest rates are instrumental tools the ECB uses within its operational framework to preserve price stability within the euro area.

These rates hold significant importance in conducting monetary policy, as they directly impact the cost of borrowing for various economic entities. These include governments, businesses, and households, both in capital markets and the market for bank loans. Furthermore, they influence the returns on various saving instruments, such as bank deposits.

Consequently, the ECB’s monetary policy decisions have a far-reaching impact on households’ and businesses’ spending, saving, and investment choices. It ultimately affects overall economic activity and, in turn, inflation rates.

ECB establishes this rate to provide the banking system with weekly liquidity injections. It determines the cost credit institutions incur when borrowing funds from the ECB for one week.

Deposit Facility Rate

The ECB also sets the rate for the deposit facility. This dictates the interest paid to credit institutions for overnight deposits held at the central bank. Notably, the deposit facility rate remained negative from 2014 until July 2022.

Marginal Lending Facility Rate

This rate represents the cost credit institutions bear when they borrow money overnight from the ECB.

These interest rates are pivotal in the ECB’s pursuit of its monetary policy objectives. They significantly influence the broader economic landscape and inflation dynamics.

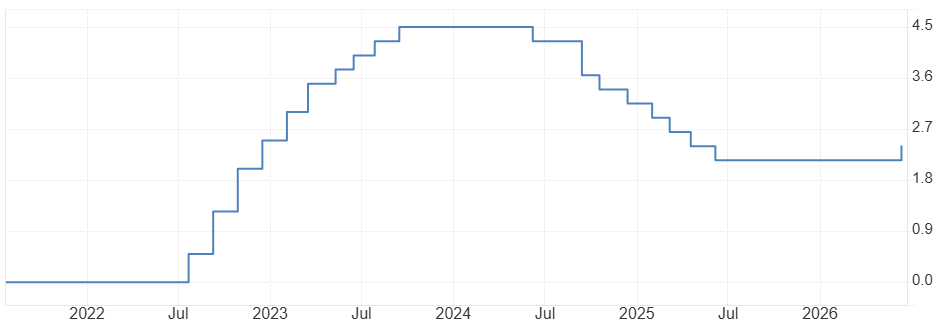

Eurozone Interest Rate Projections for the Next 5 Years

Given the many current uncertainties, formulating a realistic forecast for ECB interest rates over the next five years presents a considerable challenge. Nevertheless, the European Central Bank itself has offered projections extending as far as 2025 in its survey of professional forecasters.

According to their ECB interest rate predictions, they foresaw a rise to 3% in Q1 2023, a figure already materialized. They also predicted a further increase to 3.5% in Q2. A gradual decrease below 3% in 2024 and 2025 would follow.

In contrast, ING’s March policy rate forecasts suggested the ECB interest rate would climb to 3.5% in Q1 2023. It would reach 4% in Q2, maintaining this level until early 2024. Their analysts expected a rate of 3.5% in late 2024, gradually declining to 3% in late 2025.

Based on their econometric models, trading Economics anticipated a decrease to 2.75% in 2024 and a further decline to 1.5% in 2025.

The Influence of Interest Rates on Cryptocurrency

Cryptocurrencies, Bitcoin included, have demonstrated remarkable resilience even in the face of rising interest rates. Notably, Bitcoin experienced significant growth, with a surge of 2,000% observed between 2015 and 2016.

However, it is crucial to recognize that elevated interest rates can produce diverse effects on the cryptocurrency market. Some experts argue that persistently high inflation, rising gas prices, and increased energy costs linked to higher interest rates may potentially reduce risk appetite, thus creating challenges for cryptocurrencies.

Central Banks and Their Impact on Cryptocurrencies

Central banks have a significant influence on shaping economic conditions, directly impacting money circulation and financial market stability. Their ability to adjust interest rates directly affects borrowing rates for financial and banking institutions.

In response to widespread inflation, major central banks in developed economies, such as the Fed, the ECB, and the BoE, have chosen to raise interest rates.

It is worth noting the increasingly intertwined relationship between cryptocurrencies and these macroeconomic and monetary shifts. The decisions to raise interest rates, particularly by the Fed, have immediate repercussions for cryptocurrency markets.

The Federal Reserve’s more assertive stance has injected uncertainty into the cryptocurrency space, affecting market sentiment as tighter monetary policies take hold.

Giuseppe Ciccomascolo began his career as an investigative journalist in Italy, where he contributed to both local and national newspapers, focusing on various financial sectors.

Upon relocating to London, he worked as an analyst for Fitch's CapitalStructure and later as a Senior Reporter for Alliance News. In 2017, Giuseppe transitioned to covering cryptocurrency-related news, producing documentaries and articles on Bitcoin and other emerging digital currencies. He also played a pivotal role in establishing the academy for a cryptocurrency exchange website. Crypto remained his primary area of interest throughout his tenure as a writer for ThirdFloor.