Tokenized SpaceX shares saw strong demand, but crypto platforms lacked direct relationships with IPO underwriters.

Many products marketed as tokenized equities offer only synthetic price exposure rather than legal ownership of underlying shares.

Deep liquidity in tokenized or synthetic products does not guarantee access.

When SpaceX’s IPO drew roughly $250 billion in demand against a $75 billion offering, crypto platforms promising tokenized share access delivered nothing.

Ashley Ebersole, co-founder and chief legal officer of RWA marketplace, tx, says the failure had nothing to do with blockchain and everything to do with who sits inside the allocation process.

SpaceX IPO was probably the easiest way to explain tokenization to normal people

everyone wanted to trade before it opened: private markets, perps, tokenized products

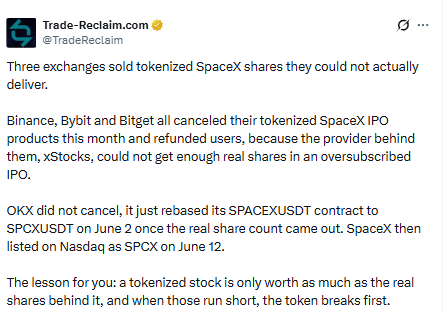

Platforms including Kraken’s xStocks, Binance, Bybit, and Bitget Wallet all relied on third-party intermediaries to source SpaceX shares rather than dealing directly with underwriters.

Crypto exchanges sold tokenized SpaceX shares they couldn’t deliver. | Source: @TradeReclaim on X.

When the offering was oversubscribed by 4x, anyone without a primary relationship with the underwriting syndicate was effectively shut out.

Ebersole pushes back on the idea that this constitutes a failure of tokenization.

“The SpaceX tokenized shares were a resounding success that had immense buyer demand. The inability, in some cases, of the tokenized stock platforms to meet that demand wasn’t a failure of the blockchain or of tokenization in general. Some orders for traditional SpaceX stock also went unfilled due to the same supply/demand dynamic,” he noted.

He is equally direct on what the gap between traditional brokers and crypto platforms actually reveals.

“Fidelity, Schwab, and SoFi have direct relationships with underwriters. They sit inside the allocation process as recognized broker-dealers. xStocks was downstream of that, dependent on whatever allocation its counterparty could source and pass through. With demand this extreme, anyone without a primary relationship with the underwriting syndicate was effectively at the back of the line. That’s not a blockchain problem. It’s a market access problem that predates crypto entirely.”

As of June 23, SpaceX shares had officially dropped below their $150 IPO price, erasing gains from the company’s public debut.

xStocks disclosed that its SpaceX tokens offered price exposure only, not direct ownership. Ebersole says that the disclaimer was technically accurate but largely invisible to most users, and that the broader market has a classification problem.

“A meaningful portion of what’s currently labeled tokenized equities in the market falls into one of three buckets: synthetic exposure with cash settlement, custody-backed tokens where the custody relationship has meaningful counterparty risk, and actual compliant onchain issuance with real legal ownership. The problem is that all three often get described with similar language until something goes wrong,” Ebersole noted.

On whether regulators should treat exposure-only tokens differently from asset-backed tokens, his answer is unambiguous.

“Regulators should absolutely address this distinction directly rather than waiting for more stress tests. The difference between a price-tracking token and an asset-backed security with onchain representation is not a minor footnote. It’s the entire legal and economic basis of the product,” he said.

Liquidity Depth Does Not Equal Delivery Infrastructure

Bitget and Block Scholes reported that NVDA-linked perpetuals reached liquidity depth close to 75% of Bitget’s Bitcoin spot market during the same period. Ebersole says that the number obscures more than it reveals.

“When you see NVDA-linked perpetuals reaching liquidity depth approaching 75% of Bitcoin spot markets, that’s not evidence that tokenized equity infrastructure is mature. It’s evidence that synthetic exposure is scaling faster than compliant delivery can. Deep liquidity in a synthetic or exposure-only product can create the impression of robust market infrastructure when the custody and settlement layer hasn’t been stress-tested. The SpaceX IPO was that stress test, ” Ebersole said.

What Compliant Delivery Actually Requires

Ebersole describes the full stack required for genuine tokenized equity issuance as sequential and non-negotiable.

“There’s no shortcut around the traditional capital markets stack. Tokenization just adds a layer on top of it. You start with a direct relationship with the underwriting syndicate or a registered broker-dealer who participates in primary issuance. That gives you a real allocation of actual shares at IPO pricing. Once purchased, those shares need to land with a qualified custodian. From there, you need a compliant issuance mechanism to mint tokens that represent legal claims on those custodied shares, not just price exposure.”

He says the platforms that failed were attempting to access a high-demand IPO through a chain of intermediaries without controlling any piece of that stack directly. “When allocation was scarce, there was no place to pull from.”

CLARITY Act Falls Short on Custody

Ebersole is measured but critical of the CLARITY Act’s ability to address the structural gap exposed by the SpaceX situation.

“The CLARITY Act spends most of its energy on classification: is this a digital asset, a security or a commodity? That’s genuinely important groundwork. But classification frameworks don’t resolve the custody and settlement questions that the xStocks situation exposed,” he noted.

He identifies three specific gaps: standards for the compliant custody of underlying assets supporting tokenized securities, disclosure requirements distinguishing exposure-only products from asset-backed ones, and a definition of settlement finality when a token is intended to represent a real equity position.

“Without that, you get a cleaner classification system sitting on top of the same ambiguous delivery infrastructure,” he said.

What Has to Be True for $2.7 Trillion

Standard Chartered analyst Geoff Kendrick projects DeFi TVL could reach $2.7 trillion by 2030, driven largely by tokenized RWAs. Ebersole says that number is achievable, but only if three parallel developments occur.

“Tokenized custody and settlement infrastructure needs to professionalize at scale, which means more institutions building or acquiring regulated custody relationships rather than relying on intermediated exposure products. Regulatory frameworks need to draw a clear line between exposure products and asset-backed tokens. And the primary market access problem needs to be solved. Tokenized equity platforms need the regulatory standing to participate in IPO distributions directly, not as a downstream consumer of whatever allocation someone else can secure,” Ebersole explained.

He adds a note of caution on how that forecast figure could be inflated.

“Without that, the $2.7 trillion number risks being inflated by synthetic products that don’t represent real onchain asset ownership. The SpaceX situation was a preview of what happens when demand scales faster than the infrastructure supporting it.”

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.