XRP Over Bitcoin, Gold & the Dollar? What YoungHoon Kim Claims — and What the Differences Actually Reveal

Share

Key Takeaways

XRP and Bitcoin were designed for different purposes, making direct superiority claims context-dependent rather than absolute.

XRP prioritizes transaction speed and settlement efficiency, while Bitcoin prioritizes scarcity and decentralization.

Claims that XRP could replace gold, silver, or the U.S. dollar remain speculative without broad adoption and regulatory clarity.

Evaluating crypto assets requires examining design, use cases, and risk factors, not influencer forecasts alone.

The question of whether XRP is superior to Bitcoin resurfaced after YoungHoon Kim (world’s smartest man) publicly stated that “XRP > Bitcoin,” alongside broader claims that Bitcoin will become the next gold while XRP could function as the next U.S. dollar.

Kim has also suggested that XRP could outperform traditional stores of value such as gold and silver, and emphasized what he describes as XRP’s “real utility.”

My prediction: #XRP may outperform gold and silver in 2026.

These statements have attracted attention because they reflect a common debate within cryptocurrency markets: whether digital assets should be evaluated primarily as stores of value or as transactional payment systems.

However, comparing XRP and Bitcoin directly without context risks oversimplifying assets that were designed to serve fundamentally different roles. Bitcoin, XRP, sovereign currencies, and precious metals each occupy distinct positions within the global financial system, shaped by differences in design, issuance, adoption, and regulation.

This article examines YoungHoon Kim’s claims by outlining the technical architecture, economic structure, real-world use cases, and regulatory positioning of XRP and Bitcoin, while also placing XRP in context against the U.S. dollar, gold, and silver.

Rather than treating these assets as interchangeable, the analysis highlights how stores of value, payment networks, and sovereign currencies historically coexist, each fulfilling separate economic functions.

What World’s Smartest Man Has Claimed About XRP and Bitcoin

YoungHoon Kim has publicly made the following assertions:

XRP is superior to Bitcoin

Bitcoin is evolving into a form of digital gold

XRP is positioned to function as a global transactional currency, comparable to the U.S. dollar

XRP has practical, real-world utility beyond speculation

XRP could outperform gold and silver in future market cycles

These design choices prioritize security, censorship resistance, and monetary scarcity, even at the expense of transaction speed and cost efficiency.

Store-of-Value Thesis

Bitcoin’s capped supply and predictable issuance schedule have led many investors to treat it as a store of value, often compared to gold. Like gold, Bitcoin is:

Scarce

Difficult to alter or debase

Independent of any central authority

This comparison underpins the widely used phrase “digital gold.” However, Bitcoin does not generate cash flows, dividends, or yield, and its value is derived entirely from market consensus and demand.

The XRP Ledger was optimized for speed, scalability, and efficiency, rather than maximal decentralization.

Transactional Utility

XRP’s primary use case is as a bridge asset for payments, particularly in cross-border transactions. Its design allows institutions to:

Transfer value quickly between currencies

Reduce reliance on pre-funded accounts

Lower transaction settlement risk

Economic Structure

Unlike Bitcoin, XRP does not rely on mining rewards. A small portion of XRP is destroyed with each transaction, introducing a deflationary mechanism, although the total supply remains far larger than Bitcoin’s.

XRP holders do not receive dividends, ownership rights, or guaranteed returns.

Asset Dimension

BTC

XRP

Asset classification

Digital commodity / crypto asset

Digital token / payment asset

Primary investment narrative

Store of value (“digital gold”)

Utility-driven transactional asset

Supply structure

Hard-capped at 21 million BTC

Pre-issued 100 billion XRP with small burn per transaction

Bitcoin’s proof-of-work consensus model is intentionally energy-intensive, as computational work is used to secure the network and prevent attacks. Estimates from the Cambridge Centre for Alternative Finance show that Bitcoin’s annual electricity consumption has ranged between 150 and 175 terawatt-hours, comparable to the energy use of some mid-sized countries.

However, multiple studies indicate that a significant and growing share of Bitcoin mining uses renewable or low-carbon energy, driven by miners’ incentives to seek the lowest-cost power sources.

By contrast, XRP’s consensus mechanism does not involve mining and consumes far less energy per transaction. This difference is measurable and well documented, but it reflects design priorities rather than environmental superiority, with Bitcoin prioritizing decentralized security and XRP prioritizing settlement efficiency.

Speed and throughput

Bitcoin processes transactions slowly by design, prioritizing security and decentralization. XRP processes transactions much faster, enabling near-instant settlement.

Faster settlement makes XRP more suitable for payments but does not inherently make it a better store of value.

Decentralization Trade-Offs

Bitcoin’s decentralization is broad and permissionless. In contrast, XRP’s consensus relies on validator nodes, and many participants use a “Unique Node List” (UNL) to decide which validators they trust.

This trade-off favors efficiency over maximal decentralization and remains a point of debate within the crypto community.

What Economists Mean by ‘Currency’ — and Where XRP Fits

Economists define key functions a currency must fulfill for widespread adoption:

Unit of account: a standard measure for pricing goods and services

Medium of exchange: widely accepted to facilitate transactions

Store of value: retains purchasing power over time

Legal tender: backed or recognized by a sovereign government

The U.S. dollar satisfies all these criteria. It is widely used in financial contracts, legal systems, wage pricing, and global trade.

In contrast, XRP does not meet these criteria in practice. It is not legal tender, has no sovereign backing, and is not broadly used to price goods or services. Thus, while it can support payment settlement, it is not a currency in the economic sense that the dollar, euro, or yen are.

XRP’s design emphasizes payment settlement efficiency, not currency status. It uses a consensus mechanism distinct from traditional mining, enabling transactions to finalize in approximately 3–5 seconds and at very low cost, compared with Bitcoin’s slower, resource-intensive model.

XRP’s faster settlement makes it useful as a bridge asset for payments but does not confer the systemic properties of a sovereign currency such as the U.S. dollar. Efficient payment rails typically coexist with fiat currencies rather than replace them, supporting financial activity without becoming the underlying unit of value or legal obligation.

In modern finance, technological improvements in payment systems (such as real-time settlement or digital wallets) do not inherently displace money itself; instead, they operate alongside existing sovereign currencies.

Economic history shows that even highly efficient payment technologies have not replaced sovereign money, as legal recognition, broad acceptance, and institutional trust are foundational to currency function.

US Dollar Performance Over Time and Peter Schiff’s Views

The U.S. dollar has long served as the dominant global reserve currency, widely used in international trade, finance, and central bank holdings. In 2025, the dollar experienced unusually weak performance against major currencies, poised for its largest annual decline since 2003 as markets anticipated Federal Reserve rate cuts and relative strength in other economies.

In this environment, the U.S. dollar Index fell and traders priced potential easing by the Fed in 2026, contributing to dollar depreciation against a basket of currencies.

At the same time, precious metals such as gold and silver rallied sharply, with gold reaching unprecedented levels above $4,500 per ounce and silver climbing past $75, movements often correlated with a weakening dollar and expectations of monetary easing.

Economist and gold advocate Peter Schiff has been an outspoken critic of the dollar’s long-term purchasing power and monetary policy. Schiff argues that ongoing debt, inflation risks, and central bank actions erode confidence in fiat currencies like the dollar.

King dollar’s reign is coming to an end. Gold will take the throne as the primary central bank reserve asset. That means the U.S. dollar will crash against other fiat currencies, and America’s free ride on the global gravy train will end. Prepare for a historic economic collapse.

He has predicted that gold could eventually replace the dollar as the primary reserve asset and has characterized the potential transition as part of a broader structural shift in global finance. Schiff asserts that sustained central bank demand for gold reflects diminishing trust in the dollar, warning of what he describes as a potential historic decline in dollar dominance.

While Schiff’s views represent one perspective on fiat currency risk, the dollar still fulfills core economic functions, such as unit of account, medium of exchange, store of value, and legal tender, and remains central to the global monetary system, even as its purchasing power fluctuates over time.

Gold, Silver and XRP: Performance Comparisons

Kim’s suggestion that XRP could outperform gold and silver reflects a price performance forecast, not a structural property.

In 2025, traditional safe-haven assets such as gold and silver delivered unusually strong returns, driven by macroeconomic factors including expectations of interest rate cuts, inflation concerns, geopolitical tensions, and increased industrial demand (especially for silver). Precious metals hit record highs toward the end of the year, highlighting their continued appeal to diversified investors.

Gold Performance in 2025

Gold prices reached all-time highs above $4,500 per ounce, marking one of the strongest annual gains in decades.

A year-end rally saw gold rising by roughly 67% to 73% year-to-date, reflecting investor demand for traditional stores of value amid macro uncertainty. These gains represent some of the largest annual moves for bullion since the late 1970s, when metals historically surged under high inflation environments.

Historically, central banks and institutional buyers have supported gold demand as part of reserve diversification strategies.

Silver Performance in 2025

Silver exhibited even more pronounced gains in 2025, driven by a combination of industrial demand (for technologies such as solar panels, electric vehicles, and electronics) and safe-haven flows.

In several markets, silver prices surged by over 100% year-to-date, and in some reports exceeded $75 per ounce at record levels before year-end.

This performance outpaced gold by a significant margin in 2025, illustrating silver’s dual role as both a monetary commodity and an industrial metal.

XRP Performance in 2025

By contrast, the digital currency XRP’s price action in 2025 was more muted when measured against these traditional assets.

However, XRP has shown moderate positive performance over the year, including annualized gains stronger than Bitcoin at times, but this performance is far smaller in scale and scope compared to gold or silver.

This contrast highlights a central point in investment analysis: outperformance over a given period does not imply equivalence in role or structural function.

Gold and silver’s rally reflects broader macroeconomic conditions that have historically driven demand for hard assets. XRP’s price is primarily tethered to crypto market sentiment, adoption narratives, and network-specific factors, and while it may outperform Bitcoin or other digital tokens occasionally, it has not matched the exceptional percentage gains seen in precious metals during the same period.

Regulatory Context: XRP vs. Bitcoin

Regulatory treatment is one of the most important structural differences between XRP and Bitcoin, as it directly affects institutional adoption, exchange availability, and long-term market stability. Bitcoin’s regulatory position is comparatively well established in major jurisdictions.

In the United States and several other regions, Bitcoin is widely treated as a commodity-like digital asset, rather than a security. This classification has allowed Bitcoin to be traded on regulated futures markets and to underpin exchange-traded products, reinforcing its perception as a macro asset rather than a financial instrument issued by a centralized entity.

XRP’s regulatory path has been more complex. Unlike Bitcoin, XRP was created and initially distributed by a company, which led regulators to scrutinize whether its sale constituted an unregistered securities offering. This distinction resulted in years of legal uncertainty, particularly in the United States, where enforcement action focused on how XRP was sold rather than on the technology itself.

While public market trading of XRP was ultimately distinguished from certain institutional sales, the prolonged legal process delayed institutional participation, highlighting how regulatory ambiguity can materially affect adoption.

The contrast between Bitcoin and XRP illustrates a broader regulatory principle: assets with no identifiable issuer tend to face fewer securities-law challenges than those associated with a corporate sponsor.

Bitcoin’s anonymous origin and decentralized issuance model insulated it from many of the disclosure and registration requirements that apply to centrally issued assets. XRP, by comparison, has had to navigate a more traditional compliance landscape, which remains a factor in how financial institutions assess risk.

Regulatory clarity matters because it shapes how assets are used and valued. Bitcoin’s relatively stable classification has encouraged its treatment as a long-term store of value and portfolio asset, while XRP’s evolving regulatory status has kept its focus on transactional utility and payment infrastructure rather than monetary dominance.

These regulatory realities underscore why claims that one asset will replace another must be evaluated not only on technical merit, but also on how law and policy shape real-world adoption.

Bitcoin prioritizes monetary scarcity and decentralization

XRP prioritizes transactional efficiency and settlement speed

Comparing them as if one must replace the other ignores how financial systems typically evolve.

Historically, stores of value and payment systems coexist rather than displace each other.

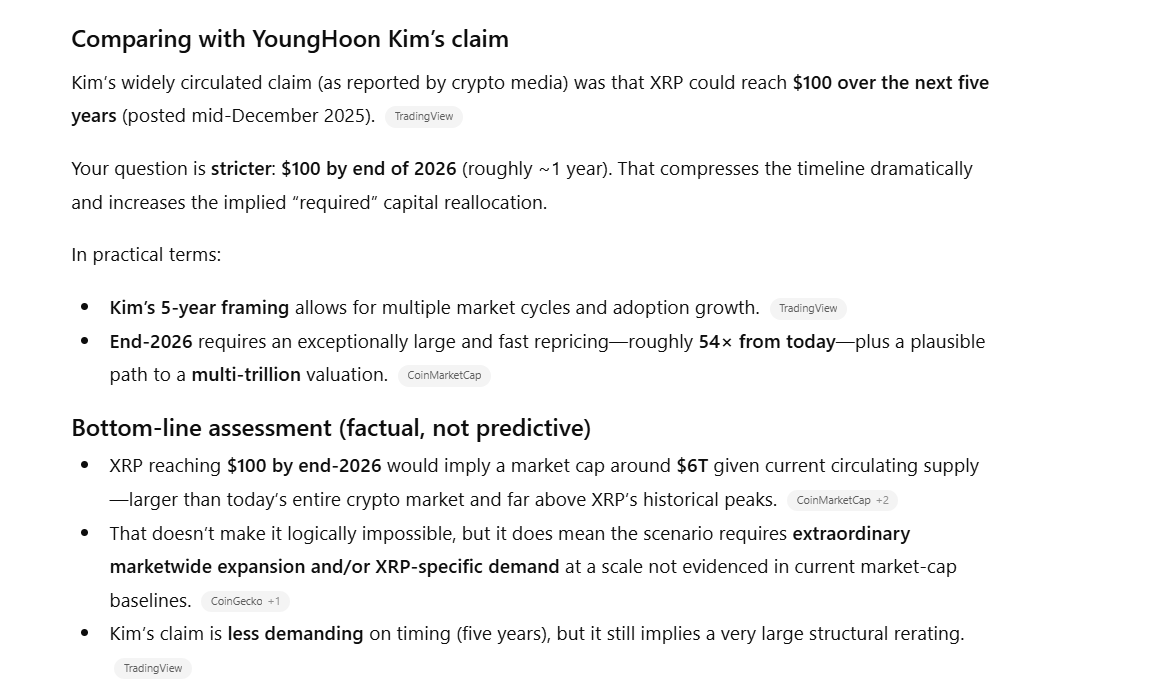

Can XRP Reach $100 by December 2026? ChatGPT Examines Price History and Risk

To analyze whether XRP could reach $100 by the end of 2026, CCN asked ChatGPT to apply basic financial principles rather than narrative-based projections.

From a market-cap perspective, a $100 XRP price would imply a valuation of roughly $6 trillion at current circulating supply, requiring either massive inflows into XRP specifically or a dramatic expansion of the overall crypto market with XRP capturing a large share. While not mathematically impossible, this sets a very high bar relative to today’s market sizes.

From a liquidity standpoint, crypto prices can rise on marginal flows, but sustaining a multi-trillion-dollar valuation typically requires deep, persistent liquidity, broad institutional access, and durable demand beyond short-lived speculative spikes.

Finally, risk-adjusted return considerations matter: XRP and crypto assets have historically shown high volatility and large drawdowns, which institutions factor heavily when assessing long-term allocations, regardless of upside potential.

Now let’s look at XRP’s price and circulating supply:

So $100 XRP by end-2026 implies XRP alone would be roughly 2× the size of the entire crypto market today and multiple times Bitcoin’s current size, unless the whole market expands dramatically.

XRP price analysis by ChatGPT. | Source: ChatGPT

What XRP’s Price History Says (And Doesn’t Say)

XRP’s widely cited all-time high is $3.84.

From today’s $1.86, $100 would be about a 54× move.

From the ATH ($3.84), $100 would still be about 26× above the prior peak.

Historically, crypto can do extreme multiples in short windows, but base rates matter: it’s rarer for a large-cap asset with tens of billions of units outstanding to achieve a multi-trillion market cap in under a year without a market wide boom and/or a major structural shift in demand.

Risks of Crypto Investing Based on High-Profile Claims

High-profile statements, especially when they come from individuals presented as exceptionally intelligent or authoritative, can strongly influence market sentiment.

However, financial outcomes are not determined by credentials, intelligence claims, or conviction alone.

Markets ultimately respond to liquidity, adoption, regulation, and macroeconomic conditions, many of which are unpredictable and outside any individual’s control.

One key risk is over-reliance on forecasts rather than fundamentals. Price targets and replacement narratives (such as claims that an asset could supplant gold, silver, or sovereign currencies) are inherently speculative unless supported by broad, sustained adoption and systemic change. Even well-reasoned frameworks can diverge from real-world outcomes when market conditions shift.

Another risk involves volatility and drawdowns. Crypto assets, including XRP, have historically experienced sharp price swings and prolonged downturns. Investors who enter positions based primarily on bold claims or timelines may underestimate the psychological and financial impact of volatility, particularly if prices move against expectations.

There is also regulatory and structural risk. Changes in regulation, market structure, or institutional participation can materially affect asset prices regardless of prior narratives. These factors often evolve slowly and unevenly, making precise timing difficult.

For these reasons, financial best practices emphasize independent research, diversification, and risk management. Evaluating crypto assets through multiple lenses, such as technical design, economic role, regulatory context, and historical performance, helps reduce the risk of decisions driven primarily by persuasive narratives rather than measurable fundamentals.

Importantly, exercising caution does not imply that a claim is wrong or that innovation will not occur. It reflects the reality that markets reward outcomes, not assertions, and that even compelling ideas must ultimately be validated by adoption, liquidity, and time.

Why Comparing XRP and Bitcoin Requires Context, Not Rankings

YoungHoon Kim’s statement that XRP is superior to Bitcoin reflects a personal opinion that prioritizes transactional utility over monetary scarcity.

That valuation framework is neither universally accepted nor rejected, it is simply one lens among many.

Bitcoin and XRP were built to solve different problems, and evaluating them requires acknowledging those differences rather than ranking them on a single scale.

Thus, claims that one asset will replace gold, silver, or sovereign currencies should be approached with caution, particularly in markets known for volatility and narrative cycles.

Did YoungHoon Kim provide evidence for his claim that XRP is superior to Bitcoin?

YoungHoon Kim has presented his view as a personal assessment rather than a formally documented analysis. His statements do not include a published valuation model, peer-reviewed research, or standardized economic framework comparing XRP and Bitcoin.

Is XRP designed to replace Bitcoin or serve the same purpose?

No. XRP and Bitcoin were built to solve different problems. Bitcoin focuses on decentralized scarcity and censorship resistance, while XRP is optimized for fast, low-cost value transfer, particularly for payment and settlement use cases.

Does XRP’s faster transaction speed make it more valuable than Bitcoin?

Faster transaction speed improves payment efficiency but does not inherently determine asset value. Market valuation depends on multiple factors, including scarcity, network trust, regulatory treatment, and long-term adoption.

Can XRP realistically function as a replacement for the US dollar?

XRP can facilitate payments, but it does not function as legal tender, a unit of account, or a sovereign-backed currency. Historically, payment networks tend to coexist with national currencies rather than replace them.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy