MSTR’s Net Bitcoin Holdings Now Exceed Its Market Cap by $3.4B — Here’s Why That’s Extremely Risky.

Share

Key Takeaways

MSTR trades like a leveraged BTC bet, not a normal tech stock, as Strategy buys BTC with a mix of convertible debt and new sales.

Strategy’s new $1.44 billion cash reserve buys time to cover dividends and interest, but it comes at the cost of further dilution.

With spot Bitcoin ETFs now widely available, many institutions may not see the need to hold MSTR for Bitcoin exposure.

Critics from macro analysts to gold advocates argue that Strategy’s debt-heavy model could become fragile in a deep BTC downturn.

Michael Saylor’s Strategy (MSTR), formerly known as MicroStrategy, holds around 650,000 BTC as of November 30, 2025. It most recently purchased 130 BTC for $11.7 million at around $89,960 per Bitcoin, according to Saylor himself. At that same $89,960 price, Strategy’s Bitcoin holdings are worth around $58.4 billion.

Michael Saylor on BTC acquisition. | Source: @saylor on X

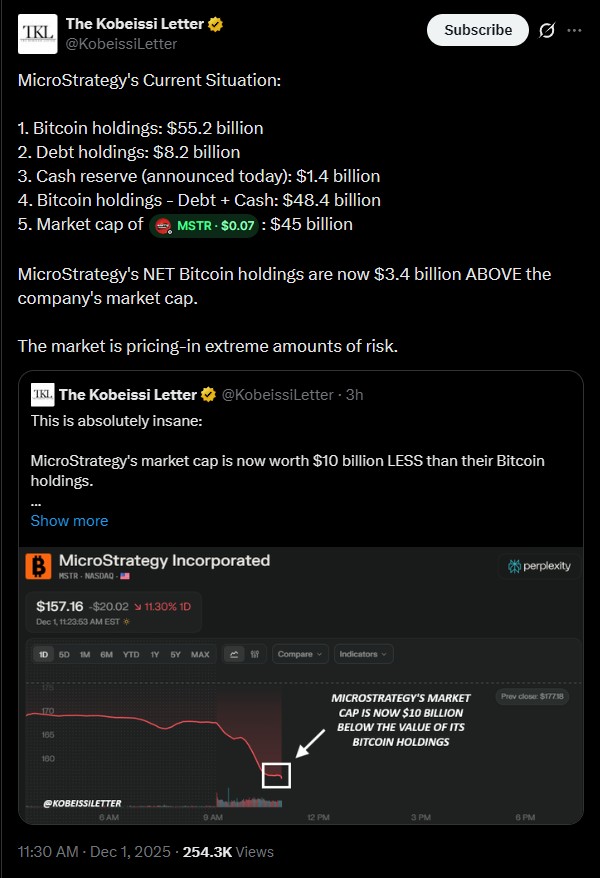

That amount in Bitcoin, on some days, can be higher than Strategy’s $45 billion equity market cap, a number that arrived after a -12% single-day crash.

This drop created a rare inversion, as pointed out by The Kobeissi Letter on X:

Strategy’s current situation. | Source: @KobeissiLetter on X

Michael Saylor’s Strategy Trades Below Its Bitcoin Value – What Does It Mean

Essentially, Strategy’s market cap is around $45 billion, but its Bitcoin is worth about $58.4 billion. So the company is worth $13 billion less than its Bitcoin. To some, this can represent a chance to “buy Bitcoin at a discount” through MSTR, as the majority of its value is tied up in the digital asset.

In practice, markets don’t typically hand out free arbitrage, but when a company with transparent hard assets trades below its net asset value (NAV), the “discount” usually signals fear, or the ability to realize those assets under stress.

New Trending Crypto Wallet Offers

Sponsored

Disclosure

We sometimes use affiliate links in our content, when clicking on those we might receive a commission at no extra cost to you. By using this website you agree to our terms and conditions and privacy policy.

NAV is a simple formula: company assets – company liabilities = NAV.

For Strategy, you must look at its NAV like this:

Start with its Bitcoin holdings ($58.4 billion)

Subtract its debt and other liabilities (about $8.2 billion)

Add its cash reserve ($1.4 billion)

You result in around $51.6 billion NAV, a number much higher than its $45 billion stock value, which is what experts like the Kobeissi Letter talk about as a “gap” of a few billion dollars.

Think of Strategy like a box:

Inside the box: Bitcoin, cash, a small software business, and a layer of debt.

Outside the box: The stock (MSTR) you can buy.

If the stuff inside the box (Strategy’s Bitcoin holdings) is worth more than the price of the box (its market cap), one must wonder if they can trust what they’re seeing.

This is similar to a closed-end fund or an old Bitcoin trust trading below NAV. The assets inside might be perfectly viable, but if investors factor in volatility, risk, and fees, they might want a discount before buying.

So Strategy’s NAV “discount” looks like a deal on Bitcoin, but in reality, it’s pricing in a huge amount of risk.

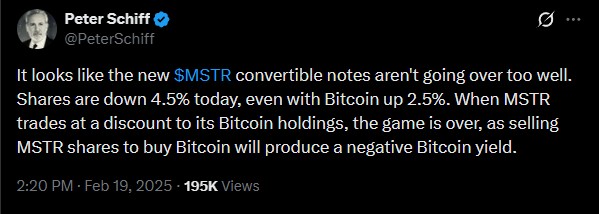

Economist Peter Schiff predicted MSTR’s inversion back in February. Source: @PeterSchiff on X

Why MSTR Investors Are Pricing in Extreme Risk

So, why does this NAV gap exist? Why are investors currently treating MSTR as riskier than Bitcoin itself? The asset MSTR has most of its value in?

We can break it into four points:

Volatility: Bitcoin is already quite volatile, with price movements of 10-20% in days. MSTR moves even more, as it uses debt and stock sales to buy more BTC. While MSTR might go up more when BTC does, it will also crash just as hard. For many investors, that extra swing is too extreme on top of traditional volatility.

Leverage risk: Strategy has about $8.2 billion in debt. Debt is money the company must pay back, with interest, even if Bitcoin falls. Debt holders are paid before shareholders, and if BTC drops hard, what’s left for said shareholders shrinks even faster.

Liquidity concerns: In theory, Strategy could sell its BTC for cash, but liquidity concerns make this tricky. If Strategy sells a massive amount of BTC during a market downturn, trading might panic, pushing the asset even lower.

Dilution: Strategy’s shift from a software company to a Bitcoin company creates new risk. It often sells new shares to raise cash for buying BTC, which dilutes existing shareholders. Strategy’s BTC focus leaves little room for diversification. It’s essentially one big Bitcoin bet, and some investors aren’t on board with that. Plus, Saylor has the heaviest say, meaning investors rely on the decisions of one man, not a board of people.

All of this makes MSTR a riskier play than simply owning Bitcoin or a Bitcoin ETF. In fact, some consider Strategy a leveraged bet on the world’s first cryptocurrency.

Leverage and Margin Risk

Leverage, or using debt to buy more BTC, can boost gains but amplify losses.

A simple example using Strategy’s numbers:

Bitcoin: $55.2 billion

Debt: $8.2 billion

Cash: $1.4 billion

Market cap: $45 billion

Now imagine Bitcoin drops 20%:

Bitcoin’s value falls from $55.2B to about $44.2B.

Debt stays at $8.2B.

Cash stays around $1.4B.

A Bitcoin drop means Strategy’s total assets (BTC + cash) fall about $11 billion, but its debt, debt that it acquired by borrowing to invest in Bitcoin, remains the same. Because most of its assets are tied up in volatility, a 20% crash translates to an even larger hit for shareholders.

Sure, the debt invested in Bitcoin can pay off if the asset rockets in value, but that’s why investors treat MSTR as a leveraged call option on BTC.

Strategy’s $1.44B USD Reserve — A Buffer or a Warning?

Strategy set up a $1.44 billion USD cash reserve to counter this risk, but it raised the money by selling stock, which further diluted its existing stockholders. While the cash might help cover dividends and interest for at least a year if BTC drops, the stock dilution required to achieve such funding presents more questions than answers.

Investor Sentiment and Market Confidence: Why MSTR Trades Below Its Bitcoin Value

As of late 2025, the market’s pricing of Strategy reveals deep skepticism about the sustainability of its debt-financed Bitcoin accumulation. Once viewed as a bold, high-conviction treasury strategy, the firm is increasingly seen more like a leveraged Bitcoin vehicle than a traditional operating company.

The “discount” — i.e., Strategy’s market capitalization falling below the value of its net Bitcoin holdings, which reflects growing investor concern over governance, regulatory exposure, and severe liquidity risk.

Moreover, in past instances when firms traded significantly below their intrinsic or net-asset value, the gap often served as a warning sign: markets didn’t believe such firms could realize (or protect) their assets under stress, especially when they were leveraged or concentrated. This historical context helps explain why the discount is not seen as a bargain, but rather as a red flag.

How Sentiment and Liquidity Shape MSTR’s Valuation

Institutional investors increasingly view Strategy not as a diversified company, but as a high-volatility, single-asset proxy, and that changes how they price it. With alternatives like spot Bitcoin ETFs now available, many believe there’s no need to tolerate the added complexity of corporate leverage, debt, and potential dilution just to gain BTC exposure.

Rising doubts about index-eligibility and possible removal from major benchmarks (like those managed by MSCI) add to the risk: forced selling by passive funds could further depress the stock and deepen the discount.

Meanwhile, macroeconomic headwinds, such as tighter liquidity globally, amplify the risk that a BTC downturn could trigger severe liquidity stress for leveraged entities like Strategy.

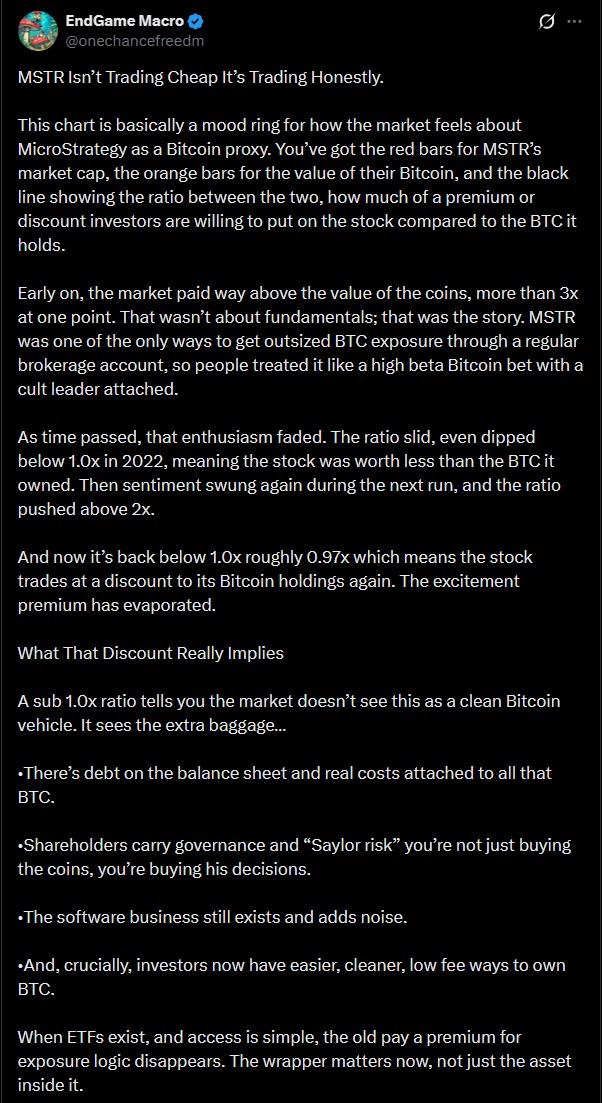

One strategist presents another angle. Source: @onechancefreedm on X

What This Means for MSTR Investors

For investors, Strategy represents a high-beta way to gain Bitcoin exposure, but wrapped in corporate and structural risk that direct BTC doesn’t carry. The supposed $3.4 B gap between net BTC holdings and market cap isn’t a free-lunch arbitrage; it’s a risk premium.

Because of the leverage, debt load, and dependence on BTC price, any meaningful Bitcoin drawdown could wipe out equity value quickly. Historically, companies in similar positions have suffered sharp losses or faced liquidity stress when volatility spikes.

If you’re considering holding or buying, this isn’t a passive play; it requires high conviction in BTC’s upside and a strong stomach for volatility. Key metrics to monitor: Bitcoin price, debt maturities or convertible-debt triggers, new equity issuance, and announcements around index inclusion or liquidity events.

Importantly, this phenomenon was especially pronounced in the financial sector, banks, and financial services companies, where asset valuations (mortgages, securities, “Level-3” assets) were highly uncertain.

The persistence of the gap (market < book) was often a warning sign: signaling potential impairment, credit risk, or uncertainty over asset realizability.

A market-to-book gap is not just a discount; it can signal fear that asset values may never be realized, or that liabilities might overwhelm assets. For MSTR, the fact that net Bitcoin holdings exceed market cap could likewise signal that investors doubt the company’s ability to extract full value (or believe potential downsides are large).

Extreme Leverage and “Too-Many-Assets-in-a-Box”: Failed Firms with Concentration Risk

Some firms have collapsed (or nearly collapsed) when they used excessive leverage to hold risky or volatile assets. A classic example is Long-Term Capital Management (LTCM), a hedge fund, not a public corporation, which collapsed in 1998 after using high leverage to hold positions that underperformed.

Another example is Babcock & Brown, an Australian investment firm whose heavy leverage and complex structure led to rapid devaluation and insolvency during the 2008 crisis.

Although these are not identical, none held Bitcoin, they illustrate the danger when firms are heavily leveraged and/or have concentrated exposure to volatile or illiquid assets. When confidence erodes, valuations can evaporate quickly.

Why Historical Examples Have Limits — MSTR Is a Unique Case

The “book value vs. market cap” metric works for traditional companies because assets are relatively stable, and liabilities are often predictable. But MSTR’s “assets” are largely Bitcoin, a highly volatile, non-traditional asset whose price swings dramatically. That adds a layer of unpredictability absent from most historical examples.

For closed-end funds, the differences (discounts/premiums) are often due to liquidity constraints, manager fees, and investor sentiment, all well-understood in the finance world. For MSTR, additional risks like crypto regulatory changes, crypto-asset custody, Bitcoin network/market dynamics, and macro environment play roles.

Historical leverage-driven collapses (like LTCM or Babcock & Brown) usually involved debt on corporate balance sheets combined with complex derivatives or opaque assets. MSTR’s leverage is used to hold Bitcoin, which can be liquidated relatively quickly (in theory), but doing so on a large scale might significantly move the market, causing large slippage and price impact.

Because of these differences, there’s no perfect historical parallel. The past provides frameworks and cautionary analogies, not exact matches.

Extreme Risk Signals Require Extreme Caution

Strategy’s valuation gap is not a hidden value; it’s a warning. The discount shows that the market doesn’t trust that the company can deliver or preserve the full value of its assets under stress.

For long-term investors, it should be viewed as a leveraged Bitcoin proxy, not a stable or diversified business. The upside exists, but so does the risk, and it compounds faster than with pure crypto or diversified equities.

Unless one truly believes in a continued BTC bull run (and is comfortable with significant drawdowns), treating this as a speculative, high-volatility instrument, not a long-term safe holding, is the prudent approach.

Some investors like MSTR’s leveraged BTC bet. If Bitcoin rallies hard, Strategy’s stock can sometimes outperform BTC.

Could Strategy reduce risk by selling some Bitcoin and paying down debt?

Yes, in theory, but management has long branded itself around a “never sell” mantra. So large asset sales could damage its narrative and signal stress to the market.

How do rating agencies see Strategy today?

Recent coverage notes that rating agencies treat Strategy as a Bitcoin treasury vehicle with significant balance sheet risk.

Could MSTR ever become more “safe” over time?

The only realistic ways to make Strategy safer would be to reduce leverage, rely less on new equity investments, and diversify beyond Bitcoin. But that approach would take away from Strategy’s ultra-BTC approach.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Max Moeller is a Chicago‑based writer and video editor passionate about games, tech, and crypto. Whether it’s crafting clear, insightful articles or piecing together engaging video retrospectives, he’s driven by curiosity and takes pride in keeping things human. Since 2017, Max has been published in a variety of notable crypto magazines.

Easy

Easy