Mining Bitcoin vs Training AI in 2026: HIVE Digital's Frank Holmes on Profitability and Infrastructure

Share

Key Takeaways

Both Bitcoin mining and AI computing convert electricity into value, but AI generates significantly higher revenue per unit of energy.

AI cloud margins reach 95% to 98%, while Bitcoin mining ranges from 13% to 83%.

High-end GPUs such as the NVIDIA H100 can generate strong revenue, but only when consistently used by paying customers.

Bitcoin mining can return capital in 1 to 3 years, while AI infrastructure may take about 10 years but offers more stable, contract-based income.

In 2026, the profitability debate between Bitcoin mining and AI computing is no longer theoretical. It is being shaped by infrastructure costs, energy constraints, and contract-based revenue models.

HIVE Digital Technologies’ Co-Founder and Executive Chairman Frank Holmes told Crypto Citizens Network (CCN)’s Dr. Guneet Kaur that both businesses start from the same premise but diverge sharply in outcomes.

“Electricity in. Bitcoin and AI revenue out. That’s the entire business model,” Holmes said.

Founded in 2017, HIVE was among the first publicly listed firms to focus on digital asset mining powered by green energy. It now operates Tier I and Tier III data centers across Canada, Sweden, and Paraguay, supporting both Bitcoin mining and GPU-based AI workloads.

Mining Bitcoin vs Training AI Explained

At the most basic level, both Bitcoin mining and AI training are ways of using powerful computers to turn electricity into something valuable. The difference is what those computers are doing and what they produce.

Bitcoin mining is the process of using specialized machines to secure the Bitcoin network and verify transactions. These machines solve complex mathematical problems. When they succeed, they earn newly created Bitcoin as a reward. In simple terms, miners are competing in a global system, and the winner gets paid in Bitcoin.

AI training, on the other hand, is the process of teaching computer models how to understand and generate information. Powerful chips, such as the NVIDIA H100, process massive datasets so the AI can learn patterns, language, images, or predictions. Instead of earning a fixed reward like mining, companies get paid by customers who need computing power to train or run AI systems.

A simple way to think about it:

Bitcoin mining = computers compete to earn digital money

AI training = computers are rented out to do complex tasks for businesses

Both use large data centers and consume electricity, but the output is different. Bitcoin mining produces a digital asset (Bitcoin) that can be sold immediately. AI training produces a service (computing power) that must be sold to customers.

This is why the two industries often use similar infrastructure, such as power, cooling, and hardware, but operate under very different business models.

Bitcoin Mining Margins Tighten After 2024 Halving

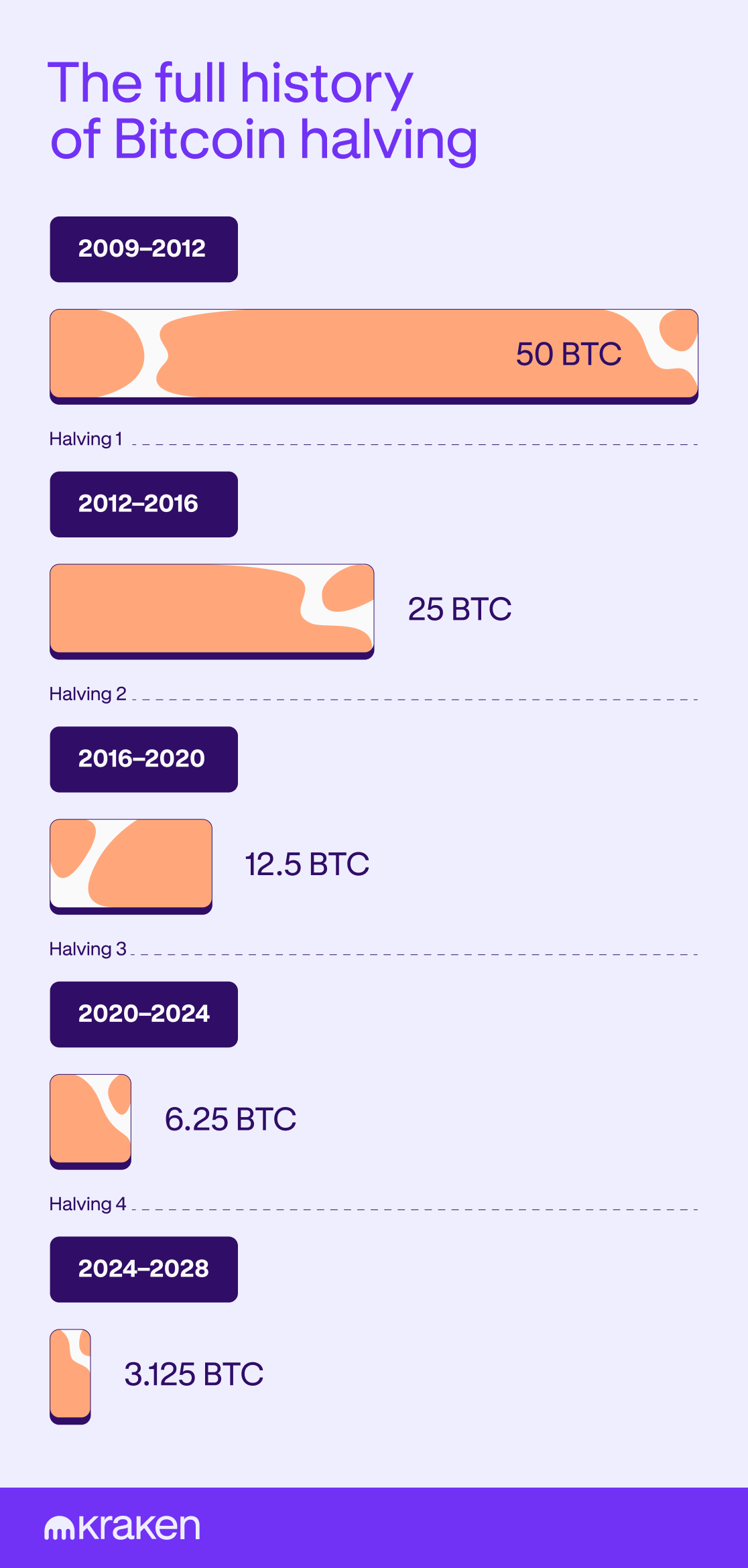

Bitcoin mining profitability in 2026 remains structurally constrained by the Bitcoin halving in April 2024, which reduced block rewards to 3.125 BTC. Since then, the global network hashrate has continued to expand, increasing competition among miners for a fixed issuance of new coins.

A timeline outlining the history of Bitcoin halving events. | Source: Kraken

Data from CoinShares indicates that the weighted average cost to produce one Bitcoin among publicly listed miners reached about $79,995 in late 2025, while hashprice, a key measure of mining revenue, declined to roughly $28 to $30 per petahash per day in early 2026. With Bitcoin trading near those levels, many operators are working within narrow margins.

The Bitcoin network hashrate. | Source: CoinShares

Mining economics are determined by four variables: the price of Bitcoin, network difficulty, hardware efficiency, and electricity cost. Of these, only hardware and power pricing are directly controllable. This creates a model in which profitability is highly sensitive to external conditions.

A real-world example illustrates the constraint. The Bitmain Antminer S21 Pro, operating at about 234 terahash per second and consuming roughly 3,510 watts, generates approximately $6.55 to $7.02 in daily revenue at current hashprice levels. At electricity rates of $0.06 per kilowatt-hour, daily power costs approach $5.05. At $0.10, they rise to $8.42, exceeding revenue.

Even more advanced systems, such as the Bitmain Antminer S21 XP Hyd, with higher output and efficiency, remain dependent on low-cost energy to sustain profitability. Once capital recovery, cooling, maintenance, and operational overhead are included, margins compress further.

These conditions explain why Bitcoin mining in 2026 favors operators with access to scale and low-cost energy, rather than small or retail participants.

AI Computing Generates Higher Revenue per Unit of Energy

In contrast, AI computing produces significantly higher revenue per unit of electricity, though it requires far greater capital investment.

Holmes cited data from the Cambridge Centre for Alternative Finance (drawing on J.P. Morgan’s research) showing that Bitcoin mining facilities cost approximately $1.2 million per megawatt to build, while AI compute infrastructure reaches about $40 million per megawatt. The difference reflects the technical complexity of AI systems, including power redundancy, liquid cooling, and high-speed networking.

‘The 33x capital cost difference is driven by power redundancy, precision cooling, high-speed GPU networking, and the engineering depth AI workloads require,’ Holmes said.

Despite this higher cost base, revenue generation is substantially stronger. Cambridge data places AI cloud revenue between $1,600 and $4,000 per megawatt-hour, compared with $80 to $151 for Bitcoin mining.

This translates into markedly different margin profiles.

‘Gross margins on AI cloud run 95% to 98%. Bitcoin mining ranges from 13% to 83% depending on BTC price, network difficulty, and electricity cost,’ Holmes said.

The economics are driven by demand for compute-intensive workloads such as large language model training and inference, typically powered by GPUs like the NVIDIA H100. These systems command premium pricing in cloud markets, particularly when supply remains constrained.

At HIVE, both engines run on the same renewable infrastructure we have been building since 2017. “On Bitcoin, we sell hashing to a US-based mining pool and receive newly minted BTC directly – no transaction history, no counterparty risk on the asset. On AI, BUZZ HPC operates on multi-year contracted GPU clusters with management projecting 80% operating margins after electrical and data center costs. Bitcoin margins move with the market. AI margins are contractually defined and denominated in US dollars,” Holmes noted.

Utilization Defines AI Profitability

While Bitcoin mining generates revenue continuously through protocol issuance, AI computing depends on utilization. Infrastructure must be matched with paying workloads, often through enterprise contracts.

A typical 8-GPU system using H100 hardware can generate several hundred dollars per day at full utilization, with monthly revenue approaching $9,000. Power consumption for such systems remains relatively modest compared with revenue, often in the range of $11 to $19 per day depending on electricity pricing.

The key constraint is not energy cost alone, but whether the system is actively processing customer workloads.

‘AI cloud revenue requires signing and retaining enterprise clients on contract. Bitcoin mining revenue is available to any operator with hashrate,’ Holmes said.

This distinction introduces different forms of risk. Bitcoin mining carries market volatility but immediate liquidity. AI computing offers higher margins but depends on customer acquisition and retention.

Infrastructure Becomes the Central Competitive Advantage

Across both sectors, control of infrastructure, particularly access to power, is emerging as the defining factor.

‘The real bottleneck is power. Permitted, renewable megawatts are the scarce resource,’ Holmes said.

Facilities originally built for Bitcoin mining can be adapted for AI workloads, as both require large-scale energy, cooling and connectivity. HIVE’s model reflects this flexibility, operating what Holmes describes as a dual-engine system in which Bitcoin mining and AI computing share the same infrastructure base.

This approach allows operators to allocate capacity dynamically, shifting between mining and AI depending on market conditions and contract availability.

“On the commercial side, we have genuine optionality. Colocation, renting capacity to hyperscalers, is a path we can pursue where the economics make sense. We are also positioned to operate compute directly, capturing the full margin stack where we have visibility on the contract backlog. Most peers are building for one model or the other. We are not locked in. The right answer depends on the contract, the counterparty, and the opportunity in front of us, Holmes emphasized.”

The divergence in capital intensity leads to different investment horizons.

Holmes notes that Bitcoin mining infrastructure, with its lower upfront cost, can achieve payback within 1 to 3 years under favorable conditions. AI infrastructure, by contrast, requires longer timelines, with payback periods around 10.8 years.

‘Bitcoin pays back faster because it costs far less to build. AI takes longer but generates durable, contract-locked revenue once it does,’ he said.

This creates a complementary dynamic rather than a purely competitive one.

‘One finances the other,’ he said.

Paraguay Energy Strategy Gives Hive Long-Term AI Cost Advantage

In Paraguay, HIVE’s AI operations benefit from USD-denominated energy rates locked for up to 15 years under Decree 5306 – one of the most favorable AI infrastructure cost structures in the Western Hemisphere.

Bitcoin mining in Paraguay operates under separate commercial power arrangements. Both give HIVE an energy cost advantage, but the long-term rate lock under Decree 5306 is specific to AI workloads and is a meaningful part of why Paraguay is central to BUZZ Cloud’s growth strategy.

Industry Shifts Reflect Changing Economics

The broader market is increasingly aligning around the economics of higher-value compute, with capital flowing toward infrastructure that can support AI workloads at scale.

Recent data highlights the magnitude of this shift. Global AI spending is projected to approach $1.5 trillion, reflecting rapid enterprise adoption of AI software, cloud services and specialized infrastructure. At the same time, the AI data center market is expected to grow at a 28.6% compound annual growth rate through 2030, driven by demand for high-performance computing environments.

This demand is translating into unprecedented infrastructure investment. Industry estimates indicate that large technology firms could collectively invest more than $600 billion in AI infrastructure in 2026 alone, as they scale data centers and secure advanced chips.

The expansion is also visible at the hardware level. Semiconductor suppliers are raising forecasts due to strong AI-related demand, signaling that capacity constraints, not lack of interest, are shaping the market.

At the infrastructure layer, the buildout is increasingly energy-driven. Data centers are projected to account for a growing share of global electricity consumption, with demand expected to rise sharply through the end of the decade. This reinforces a central industry dynamic: profitability is no longer just about compute, but about access to scalable, reliable power.

At the same time, long-term agreements for compute capacity are becoming more common, reflecting the need for predictable access to GPUs and data center resources. Multi-billion-dollar AI infrastructure deals and expanding revenue backlogs point to sustained enterprise demand for compute services rather than short-term cycles.

These trends indicate a structural shift. Profitability is increasingly tied to the ability to deploy capital into high-density, energy-intensive infrastructure and monetize that capacity through higher-value workloads such as AI training and inference, rather than lower-margin compute outputs.

Profitability Depends on Allocation Not Replacement

In 2026, the relationship between Bitcoin mining and AI computing is not defined by substitution but by allocation. Both rely on the same foundational inputs, and both can coexist within a single infrastructure framework.

Holmes emphasized that HIVE’s strategy is designed to avoid choosing between the two.

He emphasized that Bitcoin is a proven, global, decentralized asset with a fixed supply schedule. Institutional demand is growing. HIVE receives newly minted Bitcoin directly from block rewards – no counterparty risk, no transaction history on the coins. That is a structurally different acquisition model than buying BTC on an exchange.

AI compute demand is supply-constrained globally and growing faster than any infrastructure builder can match. Cambridge projects data center electricity consumption exceeding 1,000 terawatt-hours by 2030, a 14.5% compound annual growth rate. This is the largest infrastructure build since electrification. There is also a sovereign dimension most have not priced in: nations that rent compute rent their future.

“What makes HIVE’s position distinct is that our Tier I Bitcoin mining facilities carry a second life.” The buildings can convert – robotics, manufacturing, higher-density compute. And as the payback data shows, Bitcoin mining generates the capital that funds the AI build. They are not competing, he reiterated.

‘The model is designed so we never have to choose,’ he said.

AI Replacing Bitcoin Mining Narrative Driven by Market Fear

In March 2026, analyst Michaël van de Poppe also pushed back against claims that AI will replace Bitcoin mining, arguing that such narratives are driven more by market sentiment than actual data.

He described the idea that ‘AI will kill Bitcoin because data centers will stop mining’ as unfounded, saying it reflects fear that tends to surface during weaker market periods. According to him, similar claims often gain traction when prices pull back, even if underlying network fundamentals remain strong.

'AI will kill #Bitcoin, because data centers will stop mining Bitcoin'.

Absolutely bullshit.

It's one of those statements during the peak of a bear market that gets momentum, as it resonates with the fear.

Van de Poppe pointed out that Bitcoin is only modestly below its recent peak and noted that such declines are typical during broader market cycles. He emphasized that the network’s hashrate has continued to rise even as prices softened, highlighting a disconnect between price action and underlying strength.

From his perspective, this divergence could signal that Bitcoin is undervalued relative to its fundamentals, presenting a potential opportunity for investors. He added that the continued growth in hashrate suggests ongoing confidence in the network, rather than a structural shift away from mining.

That said, as demand for both decentralized finance and artificial intelligence continues to expand, operators are positioning themselves to serve both markets, adjusting output based on economic conditions.

Infrastructure Control Defines Long-Term Outcomes

The profitability comparison ultimately reflects a broader shift in the digital economy, where compute capacity and energy access are becoming strategic assets.

Holmes framed this in historical terms.

‘Every economic era has been defined by a scarce commodity. Oil. Steel. Semiconductors. In this era, the scarce resource is compute,’ he said.

The implication is that profitability in 2026 is less about choosing between Bitcoin mining and AI computing, and more about controlling the infrastructure that enables both.

‘We do not predict where demand goes. We build the infrastructure it has no choice but to use,’ Holmes said.

What is the main difference between Bitcoin mining and AI training?

Bitcoin mining uses specialized machines to validate transactions on the Bitcoin network and earn newly issued bitcoin as rewards. AI training uses high-performance GPUs, such as the NVIDIA H100, to process large datasets and train models, generating revenue by providing computing services to customers.

Why is AI computing often more profitable than Bitcoin mining in 2026?

AI computing generates significantly higher revenue per unit of energy and operates on contract-based pricing, which can lead to higher and more stable margins. Bitcoin mining revenue depends on market variables like price and network difficulty, which can compress margins, especially after the Bitcoin halving April 2024.

What are the biggest risks in each business model?

Bitcoin mining faces volatility from changes in Bitcoin price, network hashrate and electricity costs. AI computing carries different risks, including the need to secure and retain enterprise clients, high upfront capital costs and reliance on consistent utilization of GPU infrastructure.

Can the same infrastructure be used for both Bitcoin mining and AI computing?

Yes. Companies like HIVE Digital Technologies operate flexible data centers where power, cooling and connectivity can support both workloads. This allows operators to shift capacity between mining and AI depending on market conditions and profitability.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Dr. Guneet Kaur is a senior editor at CCN.com and a Science Fellow at Exponential Science. She is a fintech and blockchain expert with extensive experience in digital finance education, blockchain ecosystems, and cryptocurrency markets. She has worked with global media such as Cointelegraph, as well as education and blockchain platforms, to design and lead strategic content and learning initiatives. As an educator and assessor for top-tier executive programs, she bridges real-world fintech trends with academic insight.

Dr. Kaur is also a published researcher and peer reviewer across fintech and data science journals, including Financial Innovation Journal and International Journal of Big Data Intelligence and Applications. Her work spans data-driven analysis, Web3 innovation, and technical content development. With a strong foundation in both industry and academia, she translates complex financial technologies into practical applications, empowering learners, professionals, and institutions across the rapidly evolving digital finance landscape.

Easy

Easy