Mining continues after 2140, but rewards come only from transaction fees, not new bitcoin.

Bitcoin’s fixed supply means security must be funded by real network usage and fees.

Strong adoption can keep miners profitable and the network secure long after block rewards end.

The transition to fee-based mining happens gradually over many decades, not suddenly in 2140.

Bitcoin was built with a hard supply limit of 21 million coins, making it one of the first digital systems designed to be truly scarce. Unlike traditional money, which can be printed by central banks, Bitcoin’s issuance follows a strict schedule written directly into its code.

Because of this design, many people ask important long-term questions:

And how will miners get paid if no new Bitcoins are created?

To explore these questions, CCN spoke with Frank Holmes, Co-Founder and Executive Chairman of HIVE Digital Technologies, about whether Bitcoin mining can remain sustainable in a fully fee-driven environment.

Rather than focusing on a specific date or theoretical reward model, Holmes framed the issue as one of infrastructure and energy economics, arguing that the miners best positioned for the future are those building systems designed to remain viable under any incentive structure, long before 2140 arrives.

Let’s explore what really happens, why this transition is part of Bitcoin’s plan, and what experts say about the future of mining.

Why 2140 Is Important in Bitcoin’s Design

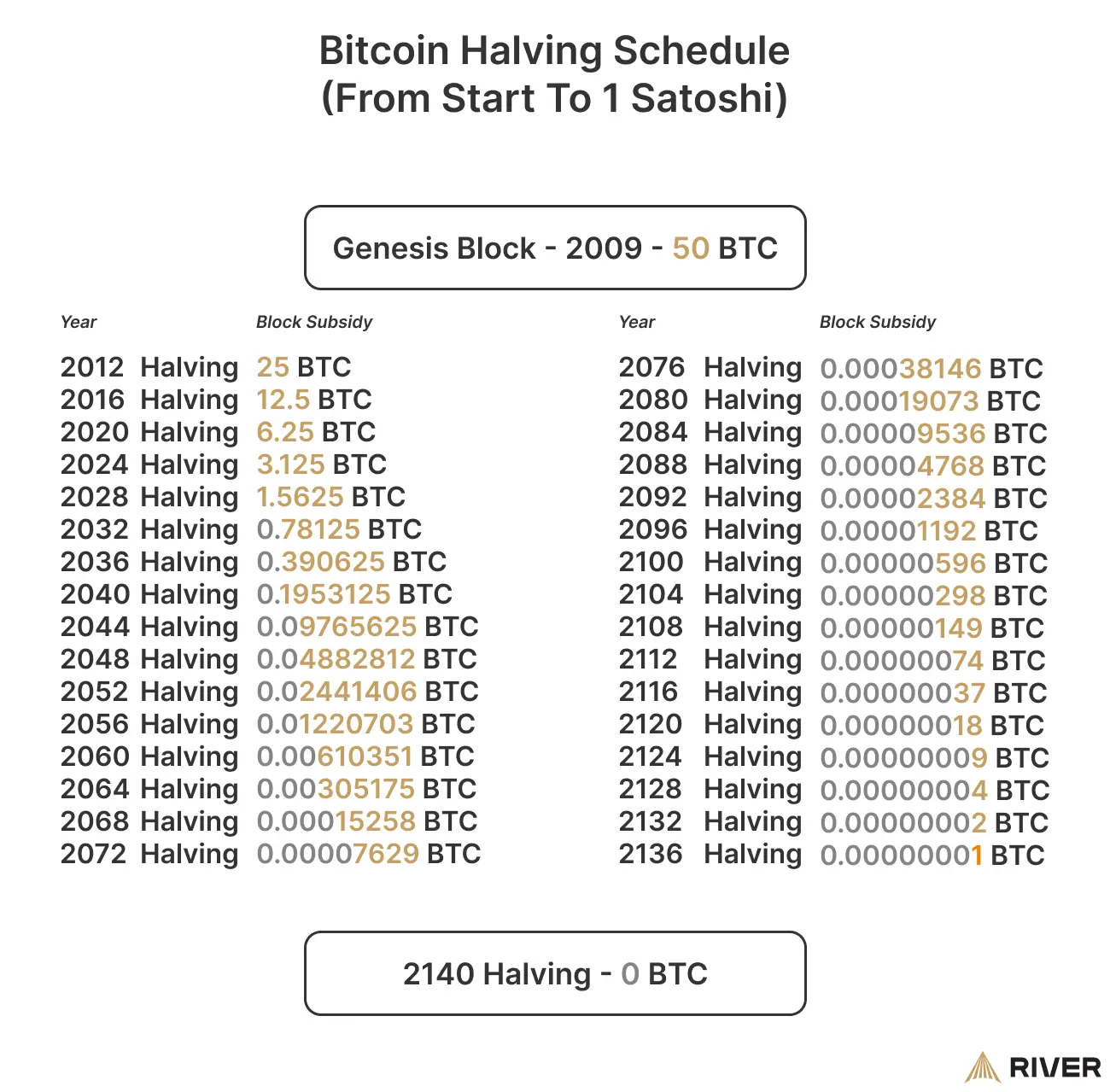

Bitcoin releases new coins through mining rewards, also known as block subsidies. Every time miners successfully add a new block to the blockchain, they receive newly created bitcoin as payment.

However, this reward is cut in half roughly every four years in an event called a halving.

Because halving continues mathematically until rewards become extremely small, the final fraction of bitcoin is expected to be mined around the year 2140. After that point, no new bitcoin will ever be issued again.

This isn’t a flaw or accident. It’s how Bitcoin was intentionally designed.

Every transaction includes a small fee that goes to the miner who confirms it. Today, block rewards make up the majority of miner income, while fees are usually a smaller portion, except during times of heavy network use, when fees can increase significantly.

Over time, however, block rewards shrink while fees become more important.

About every four years, the amount of new bitcoin miners get is cut in half. | Credit: River Financial

Mining After 2140 Is an Infrastructure Question, Not a Deadline

According to Frank Holmes, the long-term future of Bitcoin mining is often misunderstood because it focuses too narrowly on the year 2140 itself.

“The long-term question is not about predicting a specific reward model decades from now. It is about building infrastructure that remains economically relevant under any reward structure.”

Holmes emphasizes that Bitcoin mining has always been about positioning for change, not relying on a single incentive forever. While transaction fees will eventually replace block subsidies, miners that survive will be those who adapt operationally rather than depend on fixed assumptions.

“What matters most is how miners position themselves to adapt as incentives evolve.”

After 2140: Transaction Fees Become the Only Income

Once all bitcoins are mined, miners will no longer receive new coins as block rewards. Instead, they will be paid only through transaction fees.

So mining does not stop. Blocks are still created. Transactions are still confirmed.

The only difference is how miners are compensated.

You can think of it like this: Today, miners are paid partly by the system and partly by users. After 2140, miners will be paid entirely by users.

This turns Bitcoin into a pure fee-driven network, similar in concept to how payment processors charge transaction fees today.

Why Energy and Power Infrastructure Matter More Than Block Rewards

Holmes explains that miners are not just hash producers, they are energy infrastructure builders. Over time, large-scale miners have secured assets that are difficult to replicate quickly.

These elements form the foundation of digital infrastructure, regardless of how Bitcoin’s reward system evolves.

“These assets represent the hardest and most durable part of any modern digital infrastructure.”

Will Miners Still Have Incentive to Secure the Network?

This is one of the biggest debates in Bitcoin economics.

Transaction Fees Alone Are Viable If Costs Are Engineered Correctly

Bitcoin blocks have limited capacity. If millions of people want their transactions confirmed quickly, they compete by offering higher fees. Miners then prioritize transactions with the best fees, increasing their income.

In this scenario:

Bitcoin becomes a high-value settlement network

Large financial transactions move on-chain

Smaller everyday payments happen on secondary layers

Miners would function more like global settlement providers, similar to how banks and clearinghouses operate today.

Rather than treating fee-only mining as a risk, Holmes frames it as a test of operational discipline.

“Ultra-low-cost energy has always been central to HIVE’s strategy. This is not a future adjustment. It is how the company was built.”

He notes that renewable, hydro-backed power in regions like Paraguay provides long-term stability, which becomes even more important as subsidies decline.

“In any environment, energy efficiency, price discipline, and execution separate sustainable operators from short-term participants.”

This suggests that post-2140 mining favors efficiency over scale, and infrastructure over speculation.

The cautious view: fees may not always be enough

Some analysts warn that transaction fees might not always provide sufficient revenue, especially if:

If miner profits fall too low, some miners could shut down their operations. That would reduce the total computing power securing the network, which could increase risks such as centralization or certain types of attacks.

However, Bitcoin’s difficulty adjustment system automatically lowers mining difficulty if miners leave, allowing remaining miners to stay profitable. This built-in mechanism helps keep the network running even as conditions change.

Mining as a Bridge to Long-Duration Digital Infrastructure

Holmes also challenges the idea that mining is the final destination.

“Bitcoin mining is the initial workload that monetizes this foundation early and efficiently. But our Tier I sites are designed from day one to support Tier III AI and high-performance compute.”

In this view, mining revenue, whether from block rewards or fees, helps finance infrastructure that can support:

AI training and inference

High-performance computing

Cloud GPU services

Grid-balancing workloads

“Tier I power is the foundation. Tier III compute is the destination.”

This reframes Bitcoin mining not as a sunset industry after 2140, but as an entry point into long-duration energy and compute infrastructure.

What About Bitcoin’s Security Without Block Rewards?

Bitcoin’s security is tied to how much computing power protects the network. This computing power is provided by miners, and miners participate because they expect to earn money.

After 2140, that incentive depends fully on fees.

But several factors help support long-term security:

Difficulty adjustment: the system automatically balances mining difficulty based on how many miners are active.

Market competition: miners who operate more efficiently survive even when profits shrink.

Layered infrastructure: as Bitcoin adoption grows, the base layer may handle fewer but more valuable transactions.

Holmes stresses that Bitcoin’s long-term security is not just about hashrate concentration, but about geographic and operational diversity.

“Bitcoin’s security depends on economically rational, globally distributed participation. Scale alone is not enough.”

HIVE contributes to this decentralization by operating across multiple jurisdictions, grids, and regulatory environments, with a renewable-first energy strategy. This reduces concentration risk and supports network resilience.

“In the long term, Bitcoin security is strongest when supported by operators that combine scale with transparency, sustainable energy, and disciplined execution. That is the model HIVE represents.”

This means Bitcoin does not need billions of small transactions on-chain to remain secure. It needs enough high-value settlement activity to support mining incentives.

Will Mining Technology Still Matter in 2140?

Very likely, yes, but it may look very different.

Over the next century, improvements in:

chip efficiency

cooling systems

renewable energy

grid integration

could significantly reduce the cost of mining. If mining becomes more energy-efficient, miners could remain profitable even with lower absolute fee income.

Additionally, mining may increasingly use surplus or wasted energy, such as:

excess hydroelectric power

stranded natural gas

off-peak renewable production

Lower operational costs mean miners need less revenue to stay in business.

What This Means for Bitcoin Investors and Users Today

For most people, 2140 feels unimaginably far away. But understanding this future helps explain why Bitcoin behaves the way it does today.

Bitcoin’s supply is predictable. Its monetary policy cannot be changed easily. Its security model evolves gradually, not suddenly.

As block rewards continue to shrink over each halving cycle, miners already rely more on transaction fees than they did in Bitcoin’s early years. The transition is slow and continuous, not a sudden event in 2140.

This long timeline gives the network decades to adapt, upgrade, and optimize before fees become the sole incentive.

Could Bitcoin Ever Change This Rule?

Technically, Bitcoin’s rules can only change if a majority of the network agrees. But increasing the supply cap would require broad consensus from:

Historically, the Bitcoin community strongly resists changes that affect scarcity. The 21-million limit is seen as one of Bitcoin’s core value propositions. Changing it would likely face overwhelming opposition.

Because of that, most experts consider the supply cap extremely unlikely to change.

Mining After 2140 Is Part of the Plan, Not a Problem

Bitcoin was never designed to rely forever on new coin creation. Block rewards were always meant to fade, shifting responsibility to real market demand.

After 2140:

miners will still validate transactions

blocks will still be created

the network will still function

The only difference is that users, not new issuance, will fully fund security through transaction fees.

Whether this system thrives depends on Bitcoin’s global role in the future financial system. If Bitcoin remains valuable and widely used, miners will likely remain profitable. If adoption declines, mining could consolidate but the network would continue adjusting.

In many ways, Bitcoin after 2140 becomes closer to a traditional infrastructure network, one supported directly by the people who use it.

And that future was built into the code from the very beginning.

No, mining will not stop after 2140. Miners will continue to validate transactions and add new blocks to the blockchain. The only change is that they will no longer receive new bitcoin as block rewards and will instead earn income solely from transaction fees.

Could Bitcoin become less secure when block rewards end?

Bitcoin’s security will depend on how strong the transaction-fee market is. If enough users are paying fees to move high-value transactions, miners will still be incentivized to protect the network. Bitcoin’s automatic difficulty adjustment also helps keep mining economically balanced even if the number of miners changes.

Why doesn’t Bitcoin just remove the 21 million supply limit to pay miners?

Changing the supply cap would require broad agreement across the entire Bitcoin network, including developers, node operators, and users. Most of the community strongly supports the fixed supply because scarcity is central to Bitcoin’s value. For this reason, increasing the supply is considered extremely unlikely.

Will transaction fees become very expensive after 2140?

Fees could rise if demand for block space is high, but second-layer technologies like the Lightning Network may handle smaller payments off-chain. This could allow the main blockchain to focus on larger settlement transactions while keeping everyday payments affordable.

Disclaimer:

The information provided in this article is for informational purposes only. It is not intended to be, nor should it be construed as, financial advice. We do not make any warranties regarding the completeness, reliability, or accuracy of this information. All investments involve risk, and past performance does not guarantee future results. We recommend consulting a financial advisor before making any investment decisions.

Onkar Singh has three years of experience as a digital finance content creator. Throughout his career, he has collaborated with various DeFi projects and crypto media outlets. In his leisure time, he enjoys fitness activities at the gym and watching movies across different genres. Balancing his professional and personal interests, Onkar continues to contribute to the digital finance landscape while pursuing his hobbies.

Easy

Easy